You might also like

- NEFT Message FormatsDocument16 pagesNEFT Message Formatsmukeshkpatidar100% (1)

- SFMS - GuidelinesDocument116 pagesSFMS - GuidelinesRajnish ShastriNo ratings yet

- Terminal Operators LiabilityDocument30 pagesTerminal Operators LiabilityMurat YilmazNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- CBS Navigation MenuDocument34 pagesCBS Navigation MenuShailaja Thakur67% (6)

- Finnacle & Bancs Commands Bank Audit PDFDocument22 pagesFinnacle & Bancs Commands Bank Audit PDFAang Shaw50% (2)

- 01.19 Safe CustodyDocument9 pages01.19 Safe Custodymevrick_guyNo ratings yet

- Sfms-Neft 2011Document56 pagesSfms-Neft 2011VivekNo ratings yet

- All Finacle CommandsDocument39 pagesAll Finacle Commandssindhukotaru100% (2)

- Study On Implementation of KCC Scheme - WBDocument92 pagesStudy On Implementation of KCC Scheme - WBR K ThanviNo ratings yet

- Accounting Concept of Currency Chest TransactionDocument1 pageAccounting Concept of Currency Chest TransactionAjoydeep DasNo ratings yet

- Niraj-LSB CatalogueDocument8 pagesNiraj-LSB CataloguenirajNo ratings yet

- Chapter 2 Management Accounting Hansen Mowen PDFDocument28 pagesChapter 2 Management Accounting Hansen Mowen PDFidka100% (1)

- Chapter - 11: Npa DateDocument9 pagesChapter - 11: Npa DateBaideheeNo ratings yet

- Npa Status Through Short Enquiry: Menu Navigation For Npa inDocument11 pagesNpa Status Through Short Enquiry: Menu Navigation For Npa inBaidehee0% (3)

- 8 To 8 Functionality: Section Section DescriptionDocument7 pages8 To 8 Functionality: Section Section Descriptionmevrick_guyNo ratings yet

- 01.09-User System ManagementDocument12 pages01.09-User System Managementmevrick_guyNo ratings yet

- Core Banking Solutions: Andhra Pradesh Grameena Vikas Bank Head Office, WarangalDocument8 pagesCore Banking Solutions: Andhra Pradesh Grameena Vikas Bank Head Office, WarangalleenardniNo ratings yet

- 01 07-VpisDocument19 pages01 07-Vpishell_hello11No ratings yet

- GLIFDocument38 pagesGLIFTigmarashmi MahantaNo ratings yet

- 01.01 IntroductionDocument16 pages01.01 Introductionmevrick_guyNo ratings yet

- 01.04-DepositAccounts Other FunctionalitiesDocument30 pages01.04-DepositAccounts Other Functionalitiesmevrick_guyNo ratings yet

- 01.03-Deposit Accounts OpeningDocument38 pages01.03-Deposit Accounts Openingmevrick_guy0% (1)

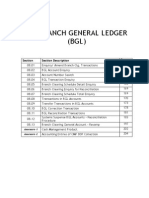

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- 01.05 Transaction ProcessingDocument23 pages01.05 Transaction Processingmevrick_guyNo ratings yet

- 01.13 ClearingDocument38 pages01.13 Clearingmevrick_guy0% (1)

- Branch InterfaceDocument81 pagesBranch Interfacemevrick_guy100% (1)

- 00.02-List of ChaptersDocument2 pages00.02-List of Chaptersashi9812No ratings yet

- Procedural Guidelines1Document69 pagesProcedural Guidelines1sburugulaNo ratings yet

- BANCS@24Document27 pagesBANCS@24Arihant Pawariya80% (5)

- What Is An Account Aggregator?Document7 pagesWhat Is An Account Aggregator?Francis NeyyanNo ratings yet

- B@Ncs24 Software Solution: ArihantDocument27 pagesB@Ncs24 Software Solution: Arihantsanchit_hNo ratings yet

- 01 06-CashDocument21 pages01 06-Cashmevrick_guyNo ratings yet

- 01.12 Posting RestrictionsDocument14 pages01.12 Posting Restrictionsmevrick_guyNo ratings yet

- Sbi Core BankingDocument28 pagesSbi Core Bankingsarthak_ganguly100% (1)

- 01.20 Government BusinessDocument48 pages01.20 Government Businessmevrick_guyNo ratings yet

- LogicDocument712 pagesLogicsuresh vedpathiNo ratings yet

- 01.17 Currency ChestDocument10 pages01.17 Currency Chestmevrick_guyNo ratings yet

- Cif CircularDocument196 pagesCif CircularLalit Yadav67% (3)

- CBS FaqDocument138 pagesCBS FaqKallol DasNo ratings yet

- Cbi BankDocument81 pagesCbi BankVaibhavKamble100% (1)

- e-KYC and New Investor Process FlowDocument32 pagese-KYC and New Investor Process FlowSneha Abhash SinghNo ratings yet

- Cash System and Procedure Part 1Document8 pagesCash System and Procedure Part 1Rohit BhaduNo ratings yet

- 01 02-CifDocument25 pages01 02-Cifmevrick_guyNo ratings yet

- NachDocument8 pagesNachS GanesanNo ratings yet

- IMPS FAQsBankers PDFDocument5 pagesIMPS FAQsBankers PDFAccounting & TaxationNo ratings yet

- UPI GuidelinesDocument31 pagesUPI Guidelinespradyumna sisodiaNo ratings yet

- Bank Management System in VB 6Document30 pagesBank Management System in VB 6yusuf habibNo ratings yet

- IRAC Norms & NPA ManagementDocument29 pagesIRAC Norms & NPA ManagementSarvar PathanNo ratings yet

- UPI For Businesses BrochureDocument8 pagesUPI For Businesses BrochuretyagigaNo ratings yet

- Bcsbi PDFDocument284 pagesBcsbi PDFsimerjotkaur100% (3)

- Sr. No. Particulars AnnexureDocument18 pagesSr. No. Particulars AnnexureSrinivasan IyerNo ratings yet

- Rtgs-Neft 10xDocument13 pagesRtgs-Neft 10xDharmavir Singh GautamNo ratings yet

- PGC FINACLEDocument95 pagesPGC FINACLEBavya MohanNo ratings yet

- AEPS Interface Specification v2.7 PDFDocument55 pagesAEPS Interface Specification v2.7 PDFSanjeev PaulNo ratings yet

- Finacle SettingDocument2 pagesFinacle Settingersukhdevchd2836No ratings yet

- SBI Core BankingDocument47 pagesSBI Core Bankingsarthak_ganguly78% (9)

- Interbank Mobile Payment ServiceDocument10 pagesInterbank Mobile Payment ServiceRitesh KumarNo ratings yet

- Npa Management SbiDocument104 pagesNpa Management Sbiparth jani100% (1)

- NPA & Income RecognitionDocument56 pagesNPA & Income RecognitionDrashti Raichura100% (1)

- Manual 1044 31mar19 Revised PDFDocument232 pagesManual 1044 31mar19 Revised PDFRanjeet kumarNo ratings yet

- Promotion Study Material Clerk To OfficerDocument315 pagesPromotion Study Material Clerk To OfficerAbhishek KumarNo ratings yet

- A HandBook On Finacle Work Flow Process 1st EditionDocument79 pagesA HandBook On Finacle Work Flow Process 1st EditionSpos Udupi100% (2)

- Ccs (Conduct) RulesDocument3 pagesCcs (Conduct) RulesKawaljeetNo ratings yet

- VT - DUNS - Human Services 03.06.17 PDFDocument5 pagesVT - DUNS - Human Services 03.06.17 PDFann vom EigenNo ratings yet

- Section 114-118Document8 pagesSection 114-118ReiZen UelmanNo ratings yet

- 1st Quarterly Exam Questions - TLE 9Document28 pages1st Quarterly Exam Questions - TLE 9Ronald Maxilom AtibagosNo ratings yet

- Planning & Managing Inventory in Supply Chain: Cycle Inventory, Safety Inventory, ABC Inventory & Product AvailabilityDocument24 pagesPlanning & Managing Inventory in Supply Chain: Cycle Inventory, Safety Inventory, ABC Inventory & Product AvailabilityAsma ShoaibNo ratings yet

- Haryana MGMTDocument28 pagesHaryana MGMTVinay KumarNo ratings yet

- Resolution No 003 2020 LoanDocument4 pagesResolution No 003 2020 LoanDexter Bernardo Calanoga TignoNo ratings yet

- Anubrat ProjectDocument80 pagesAnubrat ProjectManpreet S BhownNo ratings yet

- Selecting ERP Consulting PartnerDocument7 pagesSelecting ERP Consulting PartnerAyushmn SikkaNo ratings yet

- Coin Sort ReportDocument40 pagesCoin Sort ReportvishnuNo ratings yet

- Company Profile of Tradexcel Graphics LTDDocument19 pagesCompany Profile of Tradexcel Graphics LTDDewan ShuvoNo ratings yet

- Idx Monthly StatsticsDocument113 pagesIdx Monthly StatsticsemmaryanaNo ratings yet

- Best Practice Guidelines For Concrete Placement Planning, Field Testing, and Sample Collection PDFDocument48 pagesBest Practice Guidelines For Concrete Placement Planning, Field Testing, and Sample Collection PDFandriessebastia9395No ratings yet

- Chandelier Exit 26 Jun 2016Document4 pagesChandelier Exit 26 Jun 2016Rajan ChaudhariNo ratings yet

- GADocument72 pagesGABang OchimNo ratings yet

- Know Your BSNLDocument96 pagesKnow Your BSNLFarhanAkramNo ratings yet

- Customer Loyalty AttributesDocument25 pagesCustomer Loyalty Attributesmr_gelda6183No ratings yet

- Cross TAB in Crystal ReportsDocument15 pagesCross TAB in Crystal ReportsMarcelo Damasceno ValeNo ratings yet

- Memphis in May Damage Repair Invoice - 080223Document54 pagesMemphis in May Damage Repair Invoice - 080223Jacob Gallant0% (1)

- Talk About ImbalancesDocument1 pageTalk About ImbalancesforbesadminNo ratings yet

- G2 Group5 FMCG Products Fair & Lovely - Ver1.1Document20 pagesG2 Group5 FMCG Products Fair & Lovely - Ver1.1intesharmemonNo ratings yet

- Break Even Point (Bep) Analysis of Tomato Farming Business in Taraitak I Village, Langowan District, Minahasa DistrictDocument8 pagesBreak Even Point (Bep) Analysis of Tomato Farming Business in Taraitak I Village, Langowan District, Minahasa Districtrenita lishandiNo ratings yet

- Group 13 Excel AssignmentDocument6 pagesGroup 13 Excel AssignmentNimmy MathewNo ratings yet

- FRANCHISEDocument2 pagesFRANCHISEadieNo ratings yet

- Hanan 07 C.V.-aucDocument6 pagesHanan 07 C.V.-aucAhmed NabilNo ratings yet

- Ecoborder Brown L Shaped Landscape Edging (6-Pack) - The Home Depot CanadaDocument4 pagesEcoborder Brown L Shaped Landscape Edging (6-Pack) - The Home Depot Canadaming_zhu10No ratings yet

- HPM 207Document7 pagesHPM 207Navnit Kumar KUSHWAHANo ratings yet