You might also like

- Financial Tools For Product ManagersDocument33 pagesFinancial Tools For Product ManagersSohaeb1100% (1)

- Case Study 16-3 Bill FrenchDocument28 pagesCase Study 16-3 Bill FrenchShah 6020% (2)

- The Food Service Professional Guide to Controlling Liquor, Wine & Beverage CostsFrom EverandThe Food Service Professional Guide to Controlling Liquor, Wine & Beverage CostsNo ratings yet

- Management Accounting: Breakeven AnalysisDocument27 pagesManagement Accounting: Breakeven Analysislakshmi aparna yelganamoniNo ratings yet

- 2010 05 08 - 053020 - Case5 18Document4 pages2010 05 08 - 053020 - Case5 18ambermuNo ratings yet

- 5 Decision Making & Relevant InformationDocument42 pages5 Decision Making & Relevant Informationmedrek100% (1)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Calculate Cost of Production: Background Information For LearnersDocument3 pagesCalculate Cost of Production: Background Information For LearnersMarc Joseph LumbaNo ratings yet

- MEMO FAX CVP Analysis SampleDocument26 pagesMEMO FAX CVP Analysis SampleLita LinvilleNo ratings yet

- 12 CVP Analysis SampleDocument12 pages12 CVP Analysis SampleMaziah Muhamad100% (1)

- Learner'S Packet No. 5 Quarter 1Document6 pagesLearner'S Packet No. 5 Quarter 1Salgie Masculino100% (1)

- Business Tools For Career ReadinessDocument11 pagesBusiness Tools For Career ReadinessMauricio Huacho ChecaNo ratings yet

- Chapter II Lecture NoteDocument8 pagesChapter II Lecture NotegereNo ratings yet

- Marginal CostingDocument30 pagesMarginal Costinganon_3722476140% (1)

- Cost-Volume-Profit Analysis and Relevant CostingDocument39 pagesCost-Volume-Profit Analysis and Relevant CostingJai AceNo ratings yet

- Break Even AnalysisDocument22 pagesBreak Even Analysiskhirad afNo ratings yet

- Session 8 - Support Cost Allocation - Class Slides PDFDocument39 pagesSession 8 - Support Cost Allocation - Class Slides PDFRajat RanjanNo ratings yet

- Financial and Cost Volume Profit Models ShareDocument4 pagesFinancial and Cost Volume Profit Models ShareCahyo PriyatnoNo ratings yet

- Day 3Document33 pagesDay 3Leo ApilanNo ratings yet

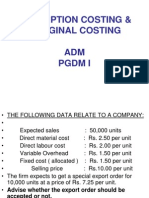

- Absorption Costing & Marginal Costing ADM PGDM IDocument9 pagesAbsorption Costing & Marginal Costing ADM PGDM ISanjay SharmaNo ratings yet

- Chapter 5 Marketing & Pricing DecisionsDocument41 pagesChapter 5 Marketing & Pricing Decisionsredwan bcNo ratings yet

- Target Costing, Life-Cycle Costing: Mgr. Andrea Gažová, PHDDocument17 pagesTarget Costing, Life-Cycle Costing: Mgr. Andrea Gažová, PHDRoberto SanchezNo ratings yet

- Topic 2: Pricing Decisions in HotelsDocument28 pagesTopic 2: Pricing Decisions in Hotelssv03No ratings yet

- Task 2: Cost-Volume-Profit Question 1: Vin Diesel Owns The Fredonia Barber Shop. He Employs Four Barbers and Pays EachDocument2 pagesTask 2: Cost-Volume-Profit Question 1: Vin Diesel Owns The Fredonia Barber Shop. He Employs Four Barbers and Pays EachNgọc Trâm TrầnNo ratings yet

- Relevant Costs (Part 2) : F. M. KapepisoDocument21 pagesRelevant Costs (Part 2) : F. M. KapepisosimsonNo ratings yet

- Chapter 1Document9 pagesChapter 1Ifye Abdulrashiid MohammedNo ratings yet

- A. Williams Module 2Document16 pagesA. Williams Module 2awilliams2641No ratings yet

- Agenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingDocument33 pagesAgenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingApoorvNo ratings yet

- Group 2 CVP RelationDocument40 pagesGroup 2 CVP RelationJeejohn Sodusta0% (1)

- Stuart DawDocument3 pagesStuart DawCaoshengjie123No ratings yet

- Bill FrenchDocument27 pagesBill FrenchRusidi Omar100% (1)

- Cost Behavior and Cost-Volume RelationshipsDocument97 pagesCost Behavior and Cost-Volume RelationshipsUtsav DubeyNo ratings yet

- Breakeven Analysis 0Document35 pagesBreakeven Analysis 0Nistha Bisht100% (1)

- Passion Funding Plan (Beta Version)Document42 pagesPassion Funding Plan (Beta Version)Myla RodrigoNo ratings yet

- Summary Report - Cost Volume Profit AnalysisDocument3 pagesSummary Report - Cost Volume Profit AnalysisruiwonshiNo ratings yet

- Topic 2: Pricing Decisions in HotelsDocument28 pagesTopic 2: Pricing Decisions in Hotelssv03No ratings yet

- Financial AnalysisDocument24 pagesFinancial AnalysisMahsheed AfshanNo ratings yet

- LO 2 Unit 4 Part 2 PriceDocument39 pagesLO 2 Unit 4 Part 2 PricePawel KulonNo ratings yet

- Lesson 6 Calculate Cost of ProductionsDocument18 pagesLesson 6 Calculate Cost of ProductionsesperancillababyNo ratings yet

- Cost Measurement: Joint & Byproduct CostingDocument51 pagesCost Measurement: Joint & Byproduct CostingstarlightNo ratings yet

- Abm PM Lesson 8 4TH QTRDocument25 pagesAbm PM Lesson 8 4TH QTRk4te.celesNo ratings yet

- Cadm Pre Mid Term 2016 - SolnDocument5 pagesCadm Pre Mid Term 2016 - SolnngrckrNo ratings yet

- CVP Analysis IibsDocument32 pagesCVP Analysis IibsSoumendra RoyNo ratings yet

- Topic 3 - CVPDocument31 pagesTopic 3 - CVPnguyennauy25042003No ratings yet

- Session 5Document17 pagesSession 5sana khanNo ratings yet

- Accounting Notes: Contribution Margin, Break-Even Analysis, Product Costing MethodsDocument4 pagesAccounting Notes: Contribution Margin, Break-Even Analysis, Product Costing Methodstome44No ratings yet

- Running Head: BMGT1101 - PRINCIPLES OF BUSINESS 1Document8 pagesRunning Head: BMGT1101 - PRINCIPLES OF BUSINESS 1Tayyab Hanif GillNo ratings yet

- Praktikum Akuntansi-BiayaDocument27 pagesPraktikum Akuntansi-BiayaK-AnggunYulianaNo ratings yet

- Marketing Study Marketing Analysis: MangaldaniansDocument5 pagesMarketing Study Marketing Analysis: MangaldaniansBARBO, KIMBERLY T.No ratings yet

- Standard Costing by Acca PDFDocument39 pagesStandard Costing by Acca PDFFahmi AbdullaNo ratings yet

- Chapter 3 Cost II Relevant Cost and DMDocument54 pagesChapter 3 Cost II Relevant Cost and DMarefayne wodajoNo ratings yet

- Ac 202 KishaniDocument16 pagesAc 202 KishaniTonie NascentNo ratings yet

- Entrep Forecasting RevenueDocument29 pagesEntrep Forecasting RevenueKevin GatanNo ratings yet

- TLECookery Grade7 8 QTR1 Module2Part2Document10 pagesTLECookery Grade7 8 QTR1 Module2Part2sanoymarkjhavez1No ratings yet

- BizCafe Team1 A3 DeliverableC CSBA1010 S1Document10 pagesBizCafe Team1 A3 DeliverableC CSBA1010 S1Nivedha ManiNo ratings yet

- G3 Break Even Pricing Written ReportDocument5 pagesG3 Break Even Pricing Written ReportADAY, KRISDYLYN A.No ratings yet

- SMCH 02Document35 pagesSMCH 02Lara Lewis AchillesNo ratings yet

- Lesson 8: Calculate Profitability of A RecipeDocument24 pagesLesson 8: Calculate Profitability of A RecipeJohn Michael SuguilonNo ratings yet

- Make $300 Every Day With CPA Activities: The CPA Activities that Works First Time, Every TimeFrom EverandMake $300 Every Day With CPA Activities: The CPA Activities that Works First Time, Every TimeNo ratings yet

- Launching Krispy Natural: Cracking The Product Management CoDocument2 pagesLaunching Krispy Natural: Cracking The Product Management CoShamik DebnathNo ratings yet

- Mutual Funds in India - Wikipedia, The Free EncyclopediaDocument4 pagesMutual Funds in India - Wikipedia, The Free EncyclopediaShamik DebnathNo ratings yet

- Archdiocese of New York Hbs Case Solution - Google SearchDocument1 pageArchdiocese of New York Hbs Case Solution - Google SearchShamik DebnathNo ratings yet

- Activation Site AfaqsDocument2 pagesActivation Site AfaqsShamik DebnathNo ratings yet

- Gooo - Google SearchDocument2 pagesGooo - Google SearchShamik DebnathNo ratings yet

- Oo - Google SearchDocument2 pagesOo - Google SearchShamik DebnathNo ratings yet

- 89 - Google SearchDocument1 page89 - Google SearchShamik DebnathNo ratings yet

- Changes in Business ModelsDocument6 pagesChanges in Business ModelsShamik DebnathNo ratings yet

- Formal Email FormatDocument1 pageFormal Email FormatShamik Debnath100% (1)