You might also like

- Lecture 6 - Profitability AnalysisDocument21 pagesLecture 6 - Profitability AnalysisTrang Bùi HàNo ratings yet

- Lecture 8 - Credit Analysis & Distress PredictionDocument22 pagesLecture 8 - Credit Analysis & Distress PredictionTrang Bùi Hà100% (1)

- Lecture 10 - Prospective Analysis - ForecastingDocument15 pagesLecture 10 - Prospective Analysis - ForecastingTrang Bùi Hà100% (1)

- Lecture 1: Overview of Financial Statement AnalysisDocument17 pagesLecture 1: Overview of Financial Statement AnalysisTrang Bùi HàNo ratings yet

- Risk Analysis Liquidity and SolvencyDocument23 pagesRisk Analysis Liquidity and SolvencyTrang Bùi HàNo ratings yet

- Chapter 01Document17 pagesChapter 01Trang Bùi HàNo ratings yet

- Annex 4Document4 pagesAnnex 4Trang Bùi HàNo ratings yet

- Abcs ContractsDocument9 pagesAbcs ContractsTrang Bùi HàNo ratings yet

- Fdi Related Dispute Settlement and The Role of Icsid Striking Balance Between de 22Document15 pagesFdi Related Dispute Settlement and The Role of Icsid Striking Balance Between de 22Trang Bùi HàNo ratings yet

- 3 International Commercial Sale of GoodsDocument31 pages3 International Commercial Sale of GoodsPranav GhabrooNo ratings yet

- Relationship Between Inflation and Interest Rates in PakistanDocument5 pagesRelationship Between Inflation and Interest Rates in PakistanTrang Bùi HàNo ratings yet

- Practicetest Macro16Document9 pagesPracticetest Macro16Trang Bùi HàNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Citigroup - Hot Corporate Finance Topics in 2006Document36 pagesCitigroup - Hot Corporate Finance Topics in 2006darkstar314No ratings yet

- Cash Flow and Ratio AnalysisDocument7 pagesCash Flow and Ratio AnalysisShalal Bin YousufNo ratings yet

- This Is A Complete, Comprehensive and Single Document Promulgated by IASB Establishing The Concepts That Underlie Financial ReportingDocument9 pagesThis Is A Complete, Comprehensive and Single Document Promulgated by IASB Establishing The Concepts That Underlie Financial ReportingFelsie Jane PenasoNo ratings yet

- Ozark S01e03Document59 pagesOzark S01e03SpeedyGonsalesNo ratings yet

- Secretos Indicador TDI MMMDocument22 pagesSecretos Indicador TDI MMMLuiz Vinhas100% (2)

- Summer Internship 2013-14: Amity Business School, Amity University, Lucknow Campus 1Document10 pagesSummer Internship 2013-14: Amity Business School, Amity University, Lucknow Campus 1Deepak Singh NegiNo ratings yet

- Financial Management Part 3 UpdatedDocument65 pagesFinancial Management Part 3 UpdatedMarielle Ace Gole CruzNo ratings yet

- Civil Law Uribe Notes Civ Rev 2Document74 pagesCivil Law Uribe Notes Civ Rev 2Chilzia RojasNo ratings yet

- Financial Markets Seminar 2 ExercisesDocument2 pagesFinancial Markets Seminar 2 Exercises小廷No ratings yet

- Mishkin Econ13e PPT 11Document39 pagesMishkin Econ13e PPT 11hangbg2k3No ratings yet

- Telekom Bill: Page 1 of 6Document6 pagesTelekom Bill: Page 1 of 6Zulkhibri ZulNo ratings yet

- A Study in Mutual Funds in IndiaDocument91 pagesA Study in Mutual Funds in IndiaNazir Ahmad AmirNo ratings yet

- Covid-19 and Its Impact On Indian EconomyDocument8 pagesCovid-19 and Its Impact On Indian EconomyDr Shubhi AgarwalNo ratings yet

- Chapal Uptown Payment Schedules PDFDocument13 pagesChapal Uptown Payment Schedules PDFHakeem Farhan TariqiNo ratings yet

- OP 4.09 Pest ManagementDocument2 pagesOP 4.09 Pest ManagementRina YulianiNo ratings yet

- Glossary BAHARDocument372 pagesGlossary BAHARJasmine AishaNo ratings yet

- ParametresDocument2 pagesParametresgabyy7985No ratings yet

- CRYPTO TRADING GUIDEDocument46 pagesCRYPTO TRADING GUIDELudwig VictoryNo ratings yet

- Equity Analysis of A Project: Capital Budgeting WorksheetDocument6 pagesEquity Analysis of A Project: Capital Budgeting WorksheetasaefwNo ratings yet

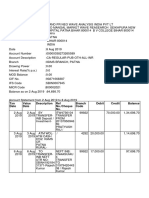

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- JPM Asia Pacific Equity 2011-07-07 624664Document22 pagesJPM Asia Pacific Equity 2011-07-07 624664tommyphyuNo ratings yet

- Tata Docomo bill details for account 910080161Document5 pagesTata Docomo bill details for account 910080161Vatsal PurohitNo ratings yet

- Induction Training Report - Planning Division: AcknowledgementDocument44 pagesInduction Training Report - Planning Division: AcknowledgementasamselaseNo ratings yet

- DematclosureDocument1 pageDematclosureVishal YadavNo ratings yet

- Natural Gas Market of EuropeDocument124 pagesNatural Gas Market of EuropeSuvam PatelNo ratings yet

- Raunak Kumar ResumeDocument2 pagesRaunak Kumar Resumeraunak29No ratings yet

- Trend Analysis Balance SheetDocument4 pagesTrend Analysis Balance Sheetrohit_indiaNo ratings yet

- MCQ NpoDocument6 pagesMCQ NpoSurya ShekharNo ratings yet

- Muslim Women Entrepreneurs: A Study On Success FactorsDocument14 pagesMuslim Women Entrepreneurs: A Study On Success FactorsBadiu'zzaman FahamiNo ratings yet