You might also like

- Closing EntriesDocument4 pagesClosing Entriesapi-299265916No ratings yet

- Periodic inventory method accounting entriesDocument9 pagesPeriodic inventory method accounting entriesnicole bancoroNo ratings yet

- PT .1 in AccountingDocument8 pagesPT .1 in AccountingMerdwindelle Allagones100% (1)

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDocument12 pagesThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- Merchandising BusinessDocument11 pagesMerchandising BusinessABM-AKRISTINE DELA CRUZNo ratings yet

- 2016 14 PPT Acctg1 Adjusting EntriesDocument20 pages2016 14 PPT Acctg1 Adjusting Entriesash wu100% (3)

- Davao Commercial Center Chart of AccountsDocument2 pagesDavao Commercial Center Chart of AccountsFrancis Raagas67% (3)

- Test Bank 4Document5 pagesTest Bank 4Jinx Cyrus RodilloNo ratings yet

- Mira's School Supplies Store Financial AnalysisDocument1 pageMira's School Supplies Store Financial AnalysisMiguel Lulab100% (1)

- Accounting Books - Journal, Ledger and Trial BalanceDocument35 pagesAccounting Books - Journal, Ledger and Trial BalanceGhie Ragat100% (3)

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet

- Nature of A Merchandising Business: Lesson 1. Intro To MerchandisingDocument14 pagesNature of A Merchandising Business: Lesson 1. Intro To Merchandisingsophia100% (1)

- Santa Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesDocument19 pagesSanta Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesareumNo ratings yet

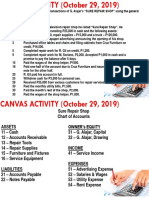

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- Acctg Closing Entries, Post Closing Trial Balance and Reversing EntriesDocument21 pagesAcctg Closing Entries, Post Closing Trial Balance and Reversing EntriesDaisy Marie A. Rosel100% (1)

- Accounting For Merchandising CompaniesDocument11 pagesAccounting For Merchandising CompaniesJesseca JosafatNo ratings yet

- Income Statement MerchandisingDocument1 pageIncome Statement MerchandisingPatrick RomeroNo ratings yet

- Group Activity 1Document10 pagesGroup Activity 1Winshei Cagulada0% (1)

- Accounting TransactionsDocument6 pagesAccounting TransactionsCelyn DeañoNo ratings yet

- Financial Acctg AdjustmentsDocument28 pagesFinancial Acctg AdjustmentsLj BesaNo ratings yet

- Chapter 2 and 3 Lopez BookDocument4 pagesChapter 2 and 3 Lopez BookSam CorsigaNo ratings yet

- Statement of Changes in EquityDocument3 pagesStatement of Changes in EquityAnonymousNo ratings yet

- Merchandising Periodic SampleDocument14 pagesMerchandising Periodic SampleYam Pinoy100% (2)

- It FinalsDocument11 pagesIt FinalsHea Jennifer AyopNo ratings yet

- General Ledger - Adrianne, Mendoza-BSBA-1 BLK BDocument6 pagesGeneral Ledger - Adrianne, Mendoza-BSBA-1 BLK BJaks ExplorerNo ratings yet

- Act3 StatDocument33 pagesAct3 StatAllecks Juel Luchana0% (1)

- Answer (Question) Module 4 Quiz 1 Adjusting Entries, Worksheet, FS PreparationDocument1 pageAnswer (Question) Module 4 Quiz 1 Adjusting Entries, Worksheet, FS Preparationkakao100% (1)

- BA991 Activity Guide Chapter 3Document12 pagesBA991 Activity Guide Chapter 3vanessaNo ratings yet

- Adjusting Entries for Cesar Cifra Accounting FirmDocument3 pagesAdjusting Entries for Cesar Cifra Accounting FirmJohn CalvinNo ratings yet

- Chapter 5 Financial Statement Analysis 1Document3 pagesChapter 5 Financial Statement Analysis 1Syrill CayetanoNo ratings yet

- Journalize the above transactions in the general journal of Bert PhotographyDocument24 pagesJournalize the above transactions in the general journal of Bert PhotographyManuel Panotes Reantazo50% (2)

- General Journal: Date Account Titles and Explanation Ref Debit CreditDocument17 pagesGeneral Journal: Date Account Titles and Explanation Ref Debit CreditPrecious NosaNo ratings yet

- Record purchases and returns under perpetual inventoryDocument6 pagesRecord purchases and returns under perpetual inventoryJalieca Lumbria Gadong0% (1)

- Negros Occidental (ACCOUNTING1)Document7 pagesNegros Occidental (ACCOUNTING1)Maxine Ceballos Glodove100% (1)

- 8 ACCT 1A&B MerchandisingDocument13 pages8 ACCT 1A&B MerchandisingShannon MojicaNo ratings yet

- Topic: Accounting Cycle of A Service BusinessDocument5 pagesTopic: Accounting Cycle of A Service BusinessJohn Rey BusimeNo ratings yet

- Thor General Merchandise ProblemDocument3 pagesThor General Merchandise ProblemEdmundo Otañes GasatanNo ratings yet

- Basic Accounting ReviewerDocument4 pagesBasic Accounting ReviewerRyan Dizon100% (1)

- Or, Deposit Slip and Withdrawl SlipDocument4 pagesOr, Deposit Slip and Withdrawl SlipJessica Rose AlbaracinNo ratings yet

- Moises Dondoyano Information Systems Company Trial Balance: Accounts Dr. CRDocument5 pagesMoises Dondoyano Information Systems Company Trial Balance: Accounts Dr. CR버니 모지코No ratings yet

- Special Journals - Quiz 38Document7 pagesSpecial Journals - Quiz 38Joana TrinidadNo ratings yet

- Current and Noncurrent AssetsDocument19 pagesCurrent and Noncurrent AssetsMylene SalvadorNo ratings yet

- Page 75Document3 pagesPage 75Aya AlayonNo ratings yet

- Handouts Acctg 1 - MerchandisingDocument13 pagesHandouts Acctg 1 - MerchandisingJoannah Marie OliverosNo ratings yet

- Agatha Trading Financial Statement 2019Document1 pageAgatha Trading Financial Statement 2019Jasmine Acta0% (1)

- Perpetual Inventory SystemDocument5 pagesPerpetual Inventory SystemRey ArudNo ratings yet

- Financial Accounting and Reporting Lesson 1 2 3Document12 pagesFinancial Accounting and Reporting Lesson 1 2 3kim fernandoNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document19 pagesFundamentals of Accountancy, Business and Management 1Shiellai Mae Polintang0% (1)

- Adjusting Entries: Fundamentals of Accountancy, Business and Management-1Document22 pagesAdjusting Entries: Fundamentals of Accountancy, Business and Management-1Arminda VillaminNo ratings yet

- Quiz Bee ReviewerDocument6 pagesQuiz Bee ReviewerFeliz Victoria CañezalNo ratings yet

- Statement of Financial PositionDocument7 pagesStatement of Financial PositionJay KwonNo ratings yet

- 600 Assembly Work: 2x + 6y 480Document5 pages600 Assembly Work: 2x + 6y 480John Louie DungcaNo ratings yet

- FABM 2 Week 4Document3 pagesFABM 2 Week 4JayMoralesNo ratings yet

- Completing The Acctg CycleDocument14 pagesCompleting The Acctg CycleHearty Hitutua100% (1)

- Practice Problem Jenny Light AccountantDocument17 pagesPractice Problem Jenny Light AccountantFranco James SanpedroNo ratings yet

- Dental Clinic AnswerDocument16 pagesDental Clinic AnswerMaria Licuanan100% (1)

- 8 Adjusted Trial BalanceDocument3 pages8 Adjusted Trial Balanceapi-299265916100% (1)

- 3 How To Prepare A Balance SheetDocument4 pages3 How To Prepare A Balance Sheetapi-299265916No ratings yet

- Basics of Accounting Cycle, Adjusting Enteries, Closing Process, Net Profit Margin Ratio.Document28 pagesBasics of Accounting Cycle, Adjusting Enteries, Closing Process, Net Profit Margin Ratio.AccountjinNo ratings yet

- 2 Income Statement FormatDocument3 pages2 Income Statement Formatapi-299265916No ratings yet

- 3 Income Statement ExamplesDocument3 pages3 Income Statement Examplesapi-299265916100% (1)

- Financial TableDocument9 pagesFinancial Tableapi-299265916No ratings yet

- 2 Liability AccountsDocument2 pages2 Liability Accountsapi-299265916No ratings yet

- 4 Revenue AccountsDocument1 page4 Revenue Accountsapi-299265916No ratings yet

- 5 Expense AccountsDocument2 pages5 Expense Accountsapi-299265916No ratings yet

- 1 Income Statement AccountsDocument2 pages1 Income Statement Accountsapi-299265916No ratings yet

- 3 Stockholders Equity AccountsDocument2 pages3 Stockholders Equity Accountsapi-299265916No ratings yet

- 3 Standards of Ethical Conduct For Management AccountantsDocument2 pages3 Standards of Ethical Conduct For Management Accountantsapi-299265916No ratings yet

- 2 Qualitative Characteristics of Financial InformationDocument2 pages2 Qualitative Characteristics of Financial Informationapi-299265916No ratings yet

- 4 Accounting PrinciplesDocument3 pages4 Accounting Principlesapi-299265916No ratings yet

- Financial Ratio AnalysisDocument4 pagesFinancial Ratio Analysisapi-299265916No ratings yet

- 2 Managerial Vs Financial AccountingDocument2 pages2 Managerial Vs Financial Accountingapi-299265916No ratings yet

- 1 Asset AccountsDocument3 pages1 Asset Accountsapi-299265916No ratings yet

- 3 Accounting StandardsDocument2 pages3 Accounting Standardsapi-299265916No ratings yet

- 1 What Is Managerial AccountingDocument2 pages1 What Is Managerial Accountingapi-299265916No ratings yet

- 7 Adjusting Entry For Bad Debts ExpenseDocument2 pages7 Adjusting Entry For Bad Debts Expenseapi-299265916No ratings yet

- 5 Adjusting Entries For Prepaid ExpenseDocument4 pages5 Adjusting Entries For Prepaid Expenseapi-299265916No ratings yet

- Reversing Entries Part 1Document3 pagesReversing Entries Part 1api-299265916No ratings yet

- 2 Adjusting Entry For Accrued RevenueDocument2 pages2 Adjusting Entry For Accrued Revenueapi-299265916No ratings yet

- 2 How To Prepare A Statement of OwnerDocument4 pages2 How To Prepare A Statement of Ownerapi-299265916No ratings yet

- 1 How To Prepare An Income StatementDocument4 pages1 How To Prepare An Income Statementapi-299265916No ratings yet

- Reversing Entries Part 2Document2 pagesReversing Entries Part 2api-299265916No ratings yet

- 3 How To Prepare A Balance SheetDocument4 pages3 How To Prepare A Balance Sheetapi-299265916No ratings yet

- 8 Adjusted Trial BalanceDocument3 pages8 Adjusted Trial Balanceapi-299265916100% (1)

- 3 Adjusting Entry For Accrued ExpensesDocument2 pages3 Adjusting Entry For Accrued Expensesapi-299265916No ratings yet

- 4 Adjusting Entry For Unearned RevenueDocument4 pages4 Adjusting Entry For Unearned Revenueapi-299265916No ratings yet

- 6 Adjusting Entry For Depreciation ExpenseDocument3 pages6 Adjusting Entry For Depreciation Expenseapi-299265916No ratings yet

- Madsen PedersenDocument23 pagesMadsen PedersenWong XianyangNo ratings yet

- Candlestick Patterns Trading GuideDocument19 pagesCandlestick Patterns Trading GuideleylNo ratings yet

- Set-22 Mba I Semester Assign QuestionsDocument10 pagesSet-22 Mba I Semester Assign Questionsஇந்துமதி வெங்கடரமணன்No ratings yet

- Performance Evaluation and Ratio Analysis - Meghna Cement - R1Document11 pagesPerformance Evaluation and Ratio Analysis - Meghna Cement - R1Sayed Abu Sufyan100% (1)

- BIAN Service LandscapeV7 0 PDFDocument1 pageBIAN Service LandscapeV7 0 PDFميلاد نوروزي رهبرNo ratings yet

- Companyfinal Accounts Including A Manufacturing AccountDocument8 pagesCompanyfinal Accounts Including A Manufacturing AccountMahmozNo ratings yet

- Case Analysis Massey Ferguson 1980Document7 pagesCase Analysis Massey Ferguson 1980Muhammad Faisal Hayat100% (2)

- Chapter 2 Macro SolutionDocument16 pagesChapter 2 Macro Solutionsaurabhsaurs80% (10)

- RosewoodDocument2 pagesRosewoodEricka Ayala100% (1)

- One-year rate sensitivity test assetsDocument6 pagesOne-year rate sensitivity test assetsAnton VelkovNo ratings yet

- FinMan 12 IPO and Hybrid Financing 2015Document50 pagesFinMan 12 IPO and Hybrid Financing 2015panjiNo ratings yet

- Strategic Risk TakingDocument9 pagesStrategic Risk TakingDipock MondalNo ratings yet

- International Business - SybillusDocument5 pagesInternational Business - SybillusaminarizwanNo ratings yet

- Words of InsuranceDocument2 pagesWords of InsuranceVeronicaGelfgren100% (2)

- 06-14 GMP UpdatedDocument260 pages06-14 GMP UpdatedGyimah SamuelNo ratings yet

- Tactical asset allocation strategiesDocument16 pagesTactical asset allocation strategiesGabriel ManjonjoNo ratings yet

- Goat Farm BudgetingDocument9 pagesGoat Farm Budgetingqfarms100% (1)

- Consumption and Savings-Lesson 4 (Repaired) - NewDocument7 pagesConsumption and Savings-Lesson 4 (Repaired) - NewMerry Rosalie AdaoNo ratings yet

- Accounting 101 OverviewDocument50 pagesAccounting 101 OverviewPallavi ChawlaNo ratings yet

- Futures and OptionsDocument51 pagesFutures and OptionsRitik VermaniNo ratings yet

- Construction Equipment PlanningDocument33 pagesConstruction Equipment PlanningMohamed Moustafa ElashwahNo ratings yet

- Teach A Man To FishDocument99 pagesTeach A Man To Fishdeepak100% (1)

- Name - KEYDocument30 pagesName - KEYjhouvanNo ratings yet

- BiscuitDocument16 pagesBiscuitVishal JainNo ratings yet

- Impairment of Non-Current Assets and Financial Reporting IssuesDocument3 pagesImpairment of Non-Current Assets and Financial Reporting IssuesfurqanNo ratings yet

- Chapter 18Document16 pagesChapter 18Norman DelirioNo ratings yet

- Demo Practise Project (FICO Exercises)Document4 pagesDemo Practise Project (FICO Exercises)saavbNo ratings yet

- Assignment 2Document3 pagesAssignment 2KARLANo ratings yet

- Security Analysis 6th Edition IntroductionDocument3 pagesSecurity Analysis 6th Edition IntroductionTheodor ToncaNo ratings yet

- TAX CARD 2019Document1 pageTAX CARD 2019Kinglovefriend100% (1)