You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Best Guide For NewbieDocument3 pagesBest Guide For Newbiebs_activeNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Lucky GuideDocument1 pageLucky Guidebs_activeNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Banker Blueprint PDFDocument37 pagesBanker Blueprint PDFSangwoo Kim100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Piano StuffDocument1 pagePiano Stuffbs_activeNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Banker Blueprint PDFDocument37 pagesBanker Blueprint PDFSangwoo Kim100% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Excel Sample Prac ExamDocument4 pagesExcel Sample Prac Exambs_activeNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Mini Case 5 - FinishedDocument9 pagesMini Case 5 - Finishedbs_activeNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- (Piano Sheet) Sonata Arctica - TallulahDocument7 pages(Piano Sheet) Sonata Arctica - TallulahAlee__50% (2)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Eka NoodlesDocument122 pagesEka NoodlesDivesha Ravi0% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Perception of Investors Towards Derivative Market With Special Reference To Indore District 837935667Document10 pagesPerception of Investors Towards Derivative Market With Special Reference To Indore District 837935667RAhuljain793_rjNo ratings yet

- Fin541 651 630-1 PDFDocument4 pagesFin541 651 630-1 PDFKiMi MooeNaNo ratings yet

- Financial Accounting 3 Chapter 1 Financial StatementsDocument3 pagesFinancial Accounting 3 Chapter 1 Financial StatementsKristine Florence TolentinoNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Insurance CompaniesDocument11 pagesInsurance CompaniesPricia AbellaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- International Capital market-OMDocument16 pagesInternational Capital market-OMOmprakash KajipetNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- S&P Shariah IndicesDocument27 pagesS&P Shariah IndicesroytanladiasanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- 09-29-2010 Term Sheet - Wednesday, Sept. 2919Document5 pages09-29-2010 Term Sheet - Wednesday, Sept. 2919Sri ReddyNo ratings yet

- Mutual Funds Sahi HaiDocument24 pagesMutual Funds Sahi Haishiva1602No ratings yet

- Dlom 2018 Q2Document76 pagesDlom 2018 Q2Catalina DumitrascuNo ratings yet

- Way2wealth Deri 31jan18Document2 pagesWay2wealth Deri 31jan18Binod Kumar PadhiNo ratings yet

- Company Law - Salomon V Salomon & Co. LTD CaseDocument9 pagesCompany Law - Salomon V Salomon & Co. LTD CaseKandarp Jha100% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Rec Center News Sun City West Dec 07Document24 pagesRec Center News Sun City West Dec 07Del Webb Sun Cities MuseumNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Capital Structure, Cost of Capital and Value-Question BankDocument8 pagesCapital Structure, Cost of Capital and Value-Question Bankkaran30No ratings yet

- Glencore 31 5 11Document6 pagesGlencore 31 5 11Chandra ChadalawadaNo ratings yet

- BPI: Balance SheetDocument1 pageBPI: Balance SheetBusinessWorld100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- You Can Be A Stock Market Genius Pdfsdocumentscom - 59c56f9b1723dde092c9f568 PDFDocument2 pagesYou Can Be A Stock Market Genius Pdfsdocumentscom - 59c56f9b1723dde092c9f568 PDFSriram RameshNo ratings yet

- Basic Finance 19.11Document35 pagesBasic Finance 19.11Cristian VillanuevaNo ratings yet

- Bowne Nyse Ipo-GuideDocument108 pagesBowne Nyse Ipo-GuideorfelynnNo ratings yet

- Liquidity, Risk and Profitability AnalysisDocument13 pagesLiquidity, Risk and Profitability AnalysisMichael Neal100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Venture Capital Advantages and DisadvantagesDocument24 pagesVenture Capital Advantages and DisadvantagesRLC VenturesNo ratings yet

- Pami Equity Index Fund: Value of P5,000 Invested Since InceptionDocument1 pagePami Equity Index Fund: Value of P5,000 Invested Since InceptionNoah BrionesNo ratings yet

- Actg 100Document4 pagesActg 100Klaverine ClarenceNo ratings yet

- 6-ch 18Document38 pages6-ch 18herueuxNo ratings yet

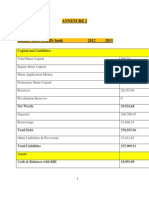

- Annexure 2Document13 pagesAnnexure 2Shalini SrivastavNo ratings yet

- Isgpore PDFDocument16 pagesIsgpore PDFGabriel La MottaNo ratings yet

- OldMutualInterims2009Announcement PDFDocument121 pagesOldMutualInterims2009Announcement PDFKristi DuranNo ratings yet

- M&a Case 1 - Radio One Group2Document13 pagesM&a Case 1 - Radio One Group2mdikme389% (9)

- Adr, GDR, Idr PDFDocument27 pagesAdr, GDR, Idr PDFmohit0% (1)

- Ratio Analysis of EXIM Banl LTDDocument11 pagesRatio Analysis of EXIM Banl LTDtoufiq999100% (4)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)