You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Letter of ComplaintDocument1 pageLetter of Complaintapi-317237792No ratings yet

- Letter of ApplicationDocument2 pagesLetter of Applicationapi-317237792No ratings yet

- Eric James JR ResumeDocument2 pagesEric James JR Resumeapi-317237792No ratings yet

- Sales Assistant ResolvedDocument1 pageSales Assistant Resolvedapi-317237792No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Bank of Valletta P.L.C.: Annual Report & Financial StatementsDocument164 pagesBank of Valletta P.L.C.: Annual Report & Financial StatementsrizaNo ratings yet

- Stained Glass CatalogDocument48 pagesStained Glass Catalogtwat neckNo ratings yet

- ERwinAPI TutorialSpreadsheetDocument42 pagesERwinAPI TutorialSpreadsheetRyan RiggsNo ratings yet

- Reading: Directions: Questions 101-140 Are Incomplete Sentences. Four Words or Phrase, Marked (A), (B), (C), (D)Document20 pagesReading: Directions: Questions 101-140 Are Incomplete Sentences. Four Words or Phrase, Marked (A), (B), (C), (D)นิกร ขจรมณีNo ratings yet

- New Rekening Koran Online 216801010479506 2023-03-01 2023-03-31 00313019Document11 pagesNew Rekening Koran Online 216801010479506 2023-03-01 2023-03-31 00313019dodimaryono22No ratings yet

- Interior Design Contract: ClientDocument4 pagesInterior Design Contract: ClientTiberiu Lupescu100% (1)

- Credit CardDocument23 pagesCredit Carddeepak kumarNo ratings yet

- Unit I.4 - Levy and Collection of GSTDocument38 pagesUnit I.4 - Levy and Collection of GSTFake MailNo ratings yet

- Annual 4 FlashbackDocument32 pagesAnnual 4 FlashbackGilvan AragãoNo ratings yet

- Project DescriptionDocument4 pagesProject DescriptionVenu GopalNo ratings yet

- Uhht BG 0 P Il 6 MP 6 GMDocument8 pagesUhht BG 0 P Il 6 MP 6 GMpaappaapNo ratings yet

- Business Credit Building Checklist 2020Document6 pagesBusiness Credit Building Checklist 2020Patrick Py100% (10)

- National Compressor Parts Catalog GuideDocument45 pagesNational Compressor Parts Catalog GuideJhonatan Villafuerte HuamancondorNo ratings yet

- Judgment by CICDocument8 pagesJudgment by CICAshish GillNo ratings yet

- Trade and Commerce Using The Computer Networks.: ASC Independent PU College Chapter:5 Emerging Modes of BusinessDocument15 pagesTrade and Commerce Using The Computer Networks.: ASC Independent PU College Chapter:5 Emerging Modes of Business20PC4007 DEEKSHITH VNo ratings yet

- Penrock Seeds Catalogue Closing Down SaleDocument26 pagesPenrock Seeds Catalogue Closing Down SalePaoloNo ratings yet

- Permanent Credit Limit Increase Application Form - Higher Limit with Income DocsDocument2 pagesPermanent Credit Limit Increase Application Form - Higher Limit with Income DocsleenobleNo ratings yet

- Terms and ConditionsDocument18 pagesTerms and ConditionsferhatimeyouNo ratings yet

- Oneplus Carding Trick of 2022 LuciDocument6 pagesOneplus Carding Trick of 2022 LuciDougNo ratings yet

- Credit Card Functionality Within OracleDocument5 pagesCredit Card Functionality Within OracleAmith Kumar IndurthiNo ratings yet

- Credit-Card Whizzes Outsmart Banks at Their Own GameDocument24 pagesCredit-Card Whizzes Outsmart Banks at Their Own GamejaspreetsaroraNo ratings yet

- Bank Reconciliation Statement TemplateDocument3 pagesBank Reconciliation Statement TemplateGarima GarimaNo ratings yet

- Ielts Writing Task 2 Band 7++Document142 pagesIelts Writing Task 2 Band 7++Muhammad SobranNo ratings yet

- 4-CONSUMER CREDIT (PART 2) (Choosing A Source of Credit, The Cost of Credit Alternatives)Document19 pages4-CONSUMER CREDIT (PART 2) (Choosing A Source of Credit, The Cost of Credit Alternatives)Nur DinieNo ratings yet

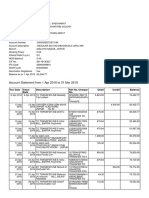

- StatementDocument4 pagesStatementlorielys0909No ratings yet

- Igem Standards ListDocument8 pagesIgem Standards ListKarthick RamasubramanianNo ratings yet

- Four Seasons Hotel Vancouver Reservation - Booking PDFDocument1 pageFour Seasons Hotel Vancouver Reservation - Booking PDFHakan DemirciNo ratings yet

- Booking Confirmation On IRCTC, Train: 12797, 23-Feb-2023, 3A, KCG - TPTYDocument1 pageBooking Confirmation On IRCTC, Train: 12797, 23-Feb-2023, 3A, KCG - TPTYBhagath SharabNo ratings yet

- IUKL Malaysian Undergraduate Enrolment GuideDocument22 pagesIUKL Malaysian Undergraduate Enrolment GuideFatimaNo ratings yet