You might also like

- For Analysis Basis of Carmen Diaz CaseDocument9 pagesFor Analysis Basis of Carmen Diaz CaseShielarien DonguilaNo ratings yet

- Case1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9Document20 pagesCase1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9amyth_dude_9090100% (2)

- Case Music MartDocument23 pagesCase Music MartDarwin Dionisio Clemente75% (4)

- Lone Pine Cafe Case SolutionDocument5 pagesLone Pine Cafe Case SolutionShammika Krishna75% (4)

- Dispensers of CaliforniaDocument4 pagesDispensers of CaliforniaShweta GautamNo ratings yet

- Cash Accounts Receivable Inventories Equipment Income Statement Balance SheetDocument3 pagesCash Accounts Receivable Inventories Equipment Income Statement Balance Sheetrajo_onglao50% (2)

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariNo ratings yet

- Case 2-2 Music Mart Balance Sheet 1 OctDocument5 pagesCase 2-2 Music Mart Balance Sheet 1 OctAnubhav Jha100% (3)

- Cash Flow StatementDocument4 pagesCash Flow StatementRavina Singh100% (1)

- The Garden Spot 1Document25 pagesThe Garden Spot 1Saad Arain0% (1)

- Lone Pine Cafe-CaseDocument28 pagesLone Pine Cafe-CaseNadya Rizkita100% (2)

- Maynard Company financial analysisDocument1 pageMaynard Company financial analysisTarry Berry75% (4)

- Revenue Recognition at HBPDocument2 pagesRevenue Recognition at HBPtechna8No ratings yet

- ACCOUNTING STERN CORPORATION (A) AnswerDocument4 pagesACCOUNTING STERN CORPORATION (A) AnswerPradina RachmadiniNo ratings yet

- Hamilton - Case BDocument8 pagesHamilton - Case BJayash KaushalNo ratings yet

- Multi Tech Case AnalysisDocument1 pageMulti Tech Case AnalysisRit8No ratings yet

- Forest City Tennis Club General Ledger and Financial StatementsDocument9 pagesForest City Tennis Club General Ledger and Financial StatementsAhmedNiaz100% (1)

- Waltham Oil Lube Centre Inc - FinalDocument10 pagesWaltham Oil Lube Centre Inc - Finalerarun2267% (3)

- CPL Case Analysis SolutionDocument5 pagesCPL Case Analysis SolutionInder Singh100% (2)

- QED Electronics - Problem 3.7Document1 pageQED Electronics - Problem 3.7ivanyongforexNo ratings yet

- Lone Pine Café FinancialsDocument5 pagesLone Pine Café FinancialsRitu ChhipaNo ratings yet

- Gemini PPT 1Document21 pagesGemini PPT 1Bhanu NirwanNo ratings yet

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdeNo ratings yet

- Waltham Oil and Lube CentreDocument5 pagesWaltham Oil and Lube CentreAnirudh Singh0% (2)

- Lori Crump Accounting Case StudyDocument1 pageLori Crump Accounting Case StudyHarsh Anchalia100% (1)

- Case Report - Grenell FarmDocument5 pagesCase Report - Grenell Farmajsibal100% (1)

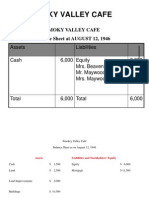

- Smokey Valley Cafe Balance Sheets 1946Document3 pagesSmokey Valley Cafe Balance Sheets 1946mohit_namanNo ratings yet

- Solution of Rachna BoutiqueDocument5 pagesSolution of Rachna BoutiqueShashank Patel100% (1)

- JW SPORT SuppliesDocument5 pagesJW SPORT SuppliesVishvesh Soni100% (4)

- Stafford Press SolvedDocument2 pagesStafford Press SolvedMurali DharanNo ratings yet

- Hamilton - Case A - 5 PDFDocument2 pagesHamilton - Case A - 5 PDFJayash Kaushal0% (1)

- Decision Sheet P&GDocument2 pagesDecision Sheet P&GApurv Toppo100% (2)

- Case 3.1Document2 pagesCase 3.1Sandeep Agrawal100% (6)

- Merton Truck CompanyDocument8 pagesMerton Truck CompanyRucha83% (6)

- Sombrero - Proposed Fruit Juice Outlet PDFDocument19 pagesSombrero - Proposed Fruit Juice Outlet PDFAngeli Aurelia100% (1)

- Music Mart SolutionDocument6 pagesMusic Mart SolutionStranger Sinha50% (2)

- Dispensers of California Case AnalysisDocument10 pagesDispensers of California Case AnalysisAvinash Singh100% (1)

- Asian ToysDocument2 pagesAsian ToysHbbekn jjdbhh100% (1)

- OPTIMIZING HEALTHCARE STAFFINGDocument53 pagesOPTIMIZING HEALTHCARE STAFFINGPriyesh Wankhede50% (2)

- Chemallte FinancialsDocument7 pagesChemallte FinancialsTara AkinteweNo ratings yet

- Financial Accounting and Reporting: The Game of Financial RatiosDocument8 pagesFinancial Accounting and Reporting: The Game of Financial RatiosANANTHA BHAIRAVI MNo ratings yet

- Appex CorporationDocument5 pagesAppex CorporationNandanaNo ratings yet

- Odyssey - The Life and Career of A Senior Consultant: Gyan Prakash Pgp/22/132Document3 pagesOdyssey - The Life and Career of A Senior Consultant: Gyan Prakash Pgp/22/132gyan prakashNo ratings yet

- Statement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Document4 pagesStatement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Jayash KaushalNo ratings yet

- Banyan HouseDocument8 pagesBanyan HouseNimit ShahNo ratings yet

- Stafford Press Move Case StudyDocument5 pagesStafford Press Move Case StudyArjun Khosla0% (2)

- Solman 12 Second EdDocument23 pagesSolman 12 Second Edferozesheriff50% (2)

- Case 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalDocument5 pagesCase 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalCyd Marie VictorianoNo ratings yet

- Campus PizzeriaDocument12 pagesCampus PizzeriaSHIVAM SRIVASTAVANo ratings yet

- Boardroom GameDocument12 pagesBoardroom GameShivam SomaniNo ratings yet

- Case Study 4 - 3 Copies ExpressDocument8 pagesCase Study 4 - 3 Copies ExpressJZ0% (1)

- Stafford Press CaseDocument4 pagesStafford Press CaseAmit Kumar AroraNo ratings yet

- Waltham Oil and Lube WorkingsDocument5 pagesWaltham Oil and Lube WorkingsGaurav Sahu100% (1)

- Octane Service StationDocument8 pagesOctane Service StationKalyan Kumar83% (6)

- Key Learnings From MR - Mehta DilemmaDocument1 pageKey Learnings From MR - Mehta Dilemmaraghav94g0% (1)

- Dewdrop Soap - BRMDocument1 pageDewdrop Soap - BRMAlexCooksNo ratings yet

- Ribons and Bows Case Study AccountingDocument6 pagesRibons and Bows Case Study Accountingsalva89830% (1)

- Chap 3 Accounting For ManagersDocument19 pagesChap 3 Accounting For ManagersBitan BanerjeeNo ratings yet

- Chapter 11 Balance SheetDocument12 pagesChapter 11 Balance SheetSha HussainNo ratings yet

- Acounts Case Study Wid SolutionsDocument20 pagesAcounts Case Study Wid SolutionsRoopali SinghNo ratings yet

- #Trulyhuman: What Does Being Truly Human Mean ?Document9 pages#Trulyhuman: What Does Being Truly Human Mean ?Shivam KanojiaNo ratings yet

- MRS - Concept Writing WebDocument94 pagesMRS - Concept Writing WebShivam KanojiaNo ratings yet

- Sub PrimeDocument5 pagesSub PrimeShivam KanojiaNo ratings yet

- Land Rover CaseDocument7 pagesLand Rover CaseadityaanandNo ratings yet

- Effectiveness of Marketing Strategies of PVR CinemaDocument59 pagesEffectiveness of Marketing Strategies of PVR CinemaDeepali Thakur100% (9)

- EX2 A1 Anshul JainDocument8 pagesEX2 A1 Anshul JainShivam KanojiaNo ratings yet

- The Elearning Guild's Handbook of E-Learning StrategyDocument87 pagesThe Elearning Guild's Handbook of E-Learning StrategySetyo Nugroho92% (24)

- Tire City AssignmentDocument7 pagesTire City AssignmentShivam Kanojia100% (1)

- Review of Policies andDocument12 pagesReview of Policies andShivam KanojiaNo ratings yet

- Book 1Document7 pagesBook 1Shivam KanojiaNo ratings yet

- Dharwar Drilling SocietyDocument3 pagesDharwar Drilling SocietyShivam KanojiaNo ratings yet

- Planview Project Portfolio Management System OverviewDocument3 pagesPlanview Project Portfolio Management System OverviewRettoNo ratings yet

- Vicente Ponce v. Alsons Cement Corporation and GironDocument1 pageVicente Ponce v. Alsons Cement Corporation and GironCheCheNo ratings yet

- Ratio Analysis of Sainsbury PLCDocument4 pagesRatio Analysis of Sainsbury PLCshuvossNo ratings yet

- US Masters Property Fund OverviewDocument4 pagesUS Masters Property Fund OverviewleithvanonselenNo ratings yet

- IRDA Workbook PDFDocument662 pagesIRDA Workbook PDFNancy Singh100% (1)

- eNPSForm PDFDocument5 pageseNPSForm PDFPradnyaNo ratings yet

- Comparative Analysis of Systematic Investment Plan and Lump Sum InvestmentDocument10 pagesComparative Analysis of Systematic Investment Plan and Lump Sum InvestmentAdit Sharma100% (1)

- Banking 01Document32 pagesBanking 01Prathamesh BhatNo ratings yet

- Structuring Venture Capital, Private Equity, and Entrepreneurial TransactionsDocument35 pagesStructuring Venture Capital, Private Equity, and Entrepreneurial TransactionsShailja BhandariNo ratings yet

- Imperatives For Market Driven StrategyDocument13 pagesImperatives For Market Driven StrategyRaju Sporsher Baire100% (1)

- Sharia Family: The Nasdaq 100 (NDX)Document2 pagesSharia Family: The Nasdaq 100 (NDX)Amir Syazwan Bin MohamadNo ratings yet

- Eldridge Industries, LLCDocument3 pagesEldridge Industries, LLCBryce MorenoNo ratings yet

- 6 Principles of FinanceDocument2 pages6 Principles of FinancePalash Bairagi100% (1)

- CH 02Document12 pagesCH 02courtney_cthNo ratings yet

- Working Capital Management and Profitability of National Fertilizers LimitedDocument3 pagesWorking Capital Management and Profitability of National Fertilizers LimitedRaman KapoorNo ratings yet

- Market Feasibility of Movie House BusinessDocument10 pagesMarket Feasibility of Movie House BusinessJonarissa BeltranNo ratings yet

- International MarketingDocument6 pagesInternational MarketingNafisa AurnaNo ratings yet

- Mpob Techniques of ControlDocument2 pagesMpob Techniques of ControlPrachi TanejaNo ratings yet

- How Government Corruptions Can Affect The Program of DevelopmentDocument5 pagesHow Government Corruptions Can Affect The Program of DevelopmentJeremiah NayosanNo ratings yet

- Analysis of Arcelor Mittal M&ADocument32 pagesAnalysis of Arcelor Mittal M&Aroli singhNo ratings yet

- Amy's dilemma between loyalty to friend and firmDocument2 pagesAmy's dilemma between loyalty to friend and firmpalros100% (1)

- Analysis of Financial Performance of State Bank of India Using Camels ApproachDocument4 pagesAnalysis of Financial Performance of State Bank of India Using Camels ApproachpriyankaNo ratings yet

- Financial Reporting and Statements ExplainedDocument26 pagesFinancial Reporting and Statements ExplainedVictor VandekerckhoveNo ratings yet

- Review Session 6 TEXTDocument6 pagesReview Session 6 TEXTAliBerradaNo ratings yet

- HEC Coach LBO CaseDocument12 pagesHEC Coach LBO CasePrashant KhoranaNo ratings yet

- Proposal Presentation: Trisakti School of ManagementDocument23 pagesProposal Presentation: Trisakti School of ManagementFiona IsabelaNo ratings yet

- Tysers P&I Report 2015Document36 pagesTysers P&I Report 2015sam ignarskiNo ratings yet

- Doheny Contributions 2011-2012Document8 pagesDoheny Contributions 2011-2012David LombardoNo ratings yet

- RailwayDocument47 pagesRailwaybazingaa aNo ratings yet

- EHub MARIM Conference Details 19082019Document13 pagesEHub MARIM Conference Details 19082019PrabhuNo ratings yet