You might also like

- Economic and Market Watch Report: 1st Quarter, 2009Document14 pagesEconomic and Market Watch Report: 1st Quarter, 2009NevadaHomesNo ratings yet

- Economic and Market Watch ReportDocument15 pagesEconomic and Market Watch ReportNevadaHomesNo ratings yet

- Economic and Market Watch Report: 2nd Quarter, 2008Document14 pagesEconomic and Market Watch Report: 2nd Quarter, 2008NevadaHomesNo ratings yet

- Northern Nevada Third Quarter 2008 Economic and Market Watch ReportDocument15 pagesNorthern Nevada Third Quarter 2008 Economic and Market Watch ReportNevadaHomesNo ratings yet

- MarketWatchQ42007 Washoe CountyDocument15 pagesMarketWatchQ42007 Washoe CountyNevadaHomes100% (1)

- Economic and Market Watch Report: 1st Quarter, 2008Document15 pagesEconomic and Market Watch Report: 1st Quarter, 2008NevadaHomesNo ratings yet

- Economic and Market Watch ReportDocument14 pagesEconomic and Market Watch ReportNevadaHomesNo ratings yet

- Northern Nevada Economic and Market Watch Report 3rd Quarter 2010Document14 pagesNorthern Nevada Economic and Market Watch Report 3rd Quarter 2010NevadaHomesNo ratings yet

- NARGSBOR31Q10Document17 pagesNARGSBOR31Q10phatty34No ratings yet

- Local ReportDocument1 pageLocal ReportAndi RobinsonNo ratings yet

- Residential Review:: A Publication of RMLS, The Source For Real Estate Statistics in Your CommunityDocument20 pagesResidential Review:: A Publication of RMLS, The Source For Real Estate Statistics in Your Communitywrite4uNo ratings yet

- St. Louis Area Real Estate Market UpdateDocument6 pagesSt. Louis Area Real Estate Market Updateapi-27591084No ratings yet

- Market Conditions AddendumDocument1 pageMarket Conditions AddendumJim WhatleyNo ratings yet

- Kyle Frazier Market Update (SF) - CA - TIBURON - 2009!07!24Document10 pagesKyle Frazier Market Update (SF) - CA - TIBURON - 2009!07!24kfraz100% (2)

- April Experiences Record Number of Buyers and Sellers: InsideDocument1 pageApril Experiences Record Number of Buyers and Sellers: Insideapi-27043054No ratings yet

- Alkimos May 2023Document9 pagesAlkimos May 2023Sri RajNo ratings yet

- Market Update: David Wright'sDocument6 pagesMarket Update: David Wright'sapi-20697951No ratings yet

- Real Estate Statistics For Clayton, MO Including Real Estate & Housing StatisticsDocument11 pagesReal Estate Statistics For Clayton, MO Including Real Estate & Housing StatisticskevincottrellNo ratings yet

- Jim Duncan's Market ReportDocument6 pagesJim Duncan's Market Reportapi-25884944No ratings yet

- Jim Duncan's Market ReportDocument10 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Local Market Trends: The Real Estate ReportDocument4 pagesLocal Market Trends: The Real Estate ReportSusan StrouseNo ratings yet

- Nest Realty's Charlottesville Real Estate Q4 2010 Market ReportDocument9 pagesNest Realty's Charlottesville Real Estate Q4 2010 Market ReportJonathan KauffmannNo ratings yet

- Market Action: Residential ReviewDocument12 pagesMarket Action: Residential Reviewwrite4uNo ratings yet

- Adam Brett Market Update (SF) - CA - BREA - 2010!04!30Document14 pagesAdam Brett Market Update (SF) - CA - BREA - 2010!04!30Adam BrettNo ratings yet

- Real Estate Statistics For Kirkwood, MO Including Real Estate & Housing StatisticsDocument6 pagesReal Estate Statistics For Kirkwood, MO Including Real Estate & Housing StatisticskevincottrellNo ratings yet

- Local Market Trends: The Real Estate ReportDocument4 pagesLocal Market Trends: The Real Estate Reportsusan6276No ratings yet

- Jim Duncan's Market ReportDocument6 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Rancho Santa Margarita - CondoDocument7 pagesRancho Santa Margarita - CondoDeborah Lynn ThomasNo ratings yet

- Real Estate Market Update For BreaDocument14 pagesReal Estate Market Update For BreaAdam BrettNo ratings yet

- St. Louis Area Real Estate Market UpdateDocument6 pagesSt. Louis Area Real Estate Market Updateapi-27591084No ratings yet

- Your Local Executive SummaryDocument1 pageYour Local Executive Summaryapi-22871972No ratings yet

- November Market ReportDocument1 pageNovember Market ReportmiguelnunezNo ratings yet

- The Nest Report: 3rd Quarter, 2009Document10 pagesThe Nest Report: 3rd Quarter, 2009api-26005222No ratings yet

- Jim Duncan's Market ReportDocument6 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Carmel Ca Homes Market Action Report Real Estate Sales For Feb 2011Document3 pagesCarmel Ca Homes Market Action Report Real Estate Sales For Feb 2011Nicole TruszkowskiNo ratings yet

- Carmel-by-the-Sea Homes Market Action Report Real Estate Sales For October 2014Document4 pagesCarmel-by-the-Sea Homes Market Action Report Real Estate Sales For October 2014Nicole TruszkowskiNo ratings yet

- Real Estate Market Update For Brea CaliforniaDocument14 pagesReal Estate Market Update For Brea CaliforniaAdam BrettNo ratings yet

- Jim Duncan's Market ReportDocument6 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Your Local Executive SummaryDocument1 pageYour Local Executive Summaryapi-22871972No ratings yet

- Altos 92130Document11 pagesAltos 92130conleyteamNo ratings yet

- Jim Duncan's Market ReportDocument6 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Jim Duncan's Market ReportDocument6 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- San Diego Market UpdateDocument5 pagesSan Diego Market UpdatemiguelnunezNo ratings yet

- Market Update: Jennifer PritchettDocument36 pagesMarket Update: Jennifer PritchettJennifer PritchettNo ratings yet

- Real Estate Market Update For BreaDocument14 pagesReal Estate Market Update For BreaAdam BrettNo ratings yet

- The Luxury Home Market A Quick Look September 2009 Single Family Detached Sales by Fletcher Wilcox V.P. Grand Canyon Title Agency, Inc. 602-648-1230Document9 pagesThe Luxury Home Market A Quick Look September 2009 Single Family Detached Sales by Fletcher Wilcox V.P. Grand Canyon Title Agency, Inc. 602-648-1230api-26125802No ratings yet

- Jim Duncan's Market ReportDocument10 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Jim Duncan's Market ReportDocument10 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Carmel Valley Homes Market Action Report Real Estate Sales For February 2015Document4 pagesCarmel Valley Homes Market Action Report Real Estate Sales For February 2015Nicole TruszkowskiNo ratings yet

- Jim Duncan's Market ReportDocument10 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Carmel-by-the-Sea Homes Market Action Report Real Estate Sales For November 2014Document4 pagesCarmel-by-the-Sea Homes Market Action Report Real Estate Sales For November 2014Nicole TruszkowskiNo ratings yet

- Real Estate Statistics For Town and Country, MO Including Real Estate & Housing StatisticsDocument16 pagesReal Estate Statistics For Town and Country, MO Including Real Estate & Housing StatisticskevincottrellNo ratings yet

- Jim Duncan's Market ReportDocument10 pagesJim Duncan's Market ReportJim DuncanNo ratings yet

- Market Update: David Wright'sDocument6 pagesMarket Update: David Wright'sapi-20697951No ratings yet

- Real Estate Market Update - BreaDocument14 pagesReal Estate Market Update - BreaAdam BrettNo ratings yet

- Market Stats For Bethel December 2011Document4 pagesMarket Stats For Bethel December 2011Donna KuehnNo ratings yet

- Q3 10 Alameda 1.1Document1 pageQ3 10 Alameda 1.1pamoettelNo ratings yet

- The Wright Report:: Sacramento's Residential Investment AnalysisDocument26 pagesThe Wright Report:: Sacramento's Residential Investment AnalysisWright Real EstateNo ratings yet

- Real Estate Statistics For Chesterfield, MO 63146 Including Real Estate & Housing StatisticsDocument11 pagesReal Estate Statistics For Chesterfield, MO 63146 Including Real Estate & Housing StatisticskevincottrellNo ratings yet

- Educated REIT Investing: The Ultimate Guide to Understanding and Investing in Real Estate Investment TrustsFrom EverandEducated REIT Investing: The Ultimate Guide to Understanding and Investing in Real Estate Investment TrustsNo ratings yet

- Northern Nevada Economic and Market Watch Report 1st Quarter 2011Document15 pagesNorthern Nevada Economic and Market Watch Report 1st Quarter 2011NevadaHomesNo ratings yet

- April 2011 Special EventsDocument1 pageApril 2011 Special EventsNevadaHomesNo ratings yet

- March 2011 Special EventsDocument1 pageMarch 2011 Special EventsNevadaHomesNo ratings yet

- Northern Nevada Economic and Market Watch Report 1st Quarter 2010Document15 pagesNorthern Nevada Economic and Market Watch Report 1st Quarter 2010NevadaHomesNo ratings yet

- Washoe County 4th Quarter 2010 Market ReportDocument1 pageWashoe County 4th Quarter 2010 Market ReportNevadaHomesNo ratings yet

- Feb 2011 Special EventsDocument1 pageFeb 2011 Special EventsNevadaHomesNo ratings yet

- Economic and Market Watch Report: 2nd Quarter, 2010Document15 pagesEconomic and Market Watch Report: 2nd Quarter, 2010NevadaHomesNo ratings yet

- Northern Nevada Economic and Market Watch Report 3rd Quarter 2010Document14 pagesNorthern Nevada Economic and Market Watch Report 3rd Quarter 2010NevadaHomesNo ratings yet

- Economic and Market Watch ReportDocument14 pagesEconomic and Market Watch ReportNevadaHomesNo ratings yet

- Economic and Market Watch Report: 2nd Quarter, 2009Document14 pagesEconomic and Market Watch Report: 2nd Quarter, 2009NevadaHomesNo ratings yet

- FTHB CreditDocument2 pagesFTHB CreditNevadaHomesNo ratings yet

- 2007 4th Quarter Washoe County ReportDocument1 page2007 4th Quarter Washoe County ReportNevadaHomesNo ratings yet

- Economic and Market Watch Report: 1st Quarter, 2008Document15 pagesEconomic and Market Watch Report: 1st Quarter, 2008NevadaHomesNo ratings yet

- Reno, NV Special Events May 08Document1 pageReno, NV Special Events May 08NevadaHomesNo ratings yet

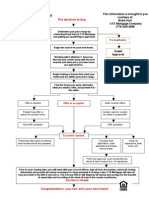

- Home Buying Process Flow ChartDocument1 pageHome Buying Process Flow ChartNevadaHomes100% (5)

- Special Events March 08Document1 pageSpecial Events March 08NevadaHomesNo ratings yet

- Daily Timecard Entry in HoursDocument20 pagesDaily Timecard Entry in HoursadnanykhanNo ratings yet

- Why The Bollard Pull Calculation Method For A Barge Won't Work For A Ship - TheNavalArchDocument17 pagesWhy The Bollard Pull Calculation Method For A Barge Won't Work For A Ship - TheNavalArchFederico BabichNo ratings yet

- This Study Resource Was: Artur Vartanyan Supply Chain and Operations Management MGMT25000D Tesla Motors, IncDocument9 pagesThis Study Resource Was: Artur Vartanyan Supply Chain and Operations Management MGMT25000D Tesla Motors, IncNguyễn Như QuỳnhNo ratings yet

- The Bedford Clanger May 2013 (The Beer Issue)Document12 pagesThe Bedford Clanger May 2013 (The Beer Issue)Erica RoffeNo ratings yet

- DamaDocument21 pagesDamaLive Law67% (3)

- m100 Stopswitch ManualDocument12 pagesm100 Stopswitch ManualPatrick TiongsonNo ratings yet

- AirROC T35 D45 D50 Tech SpecDocument4 pagesAirROC T35 D45 D50 Tech SpecmdelvallevNo ratings yet

- 71cryptocurrencies Have Become One of The Hottest Topics in The Financial WorldDocument2 pages71cryptocurrencies Have Become One of The Hottest Topics in The Financial WorldicantakeyouupNo ratings yet

- RTC Ruling on Land Ownership Upheld by CADocument12 pagesRTC Ruling on Land Ownership Upheld by CAGladys BantilanNo ratings yet

- Export Promoting InstitutesDocument21 pagesExport Promoting InstitutesVikaskundu28100% (1)

- Science Room Rules Teaching PlanDocument1 pageScience Room Rules Teaching PlanraqibsheenaNo ratings yet

- PR-Unit1-ERP EvolutionDocument13 pagesPR-Unit1-ERP EvolutionSiddhant AggarwalNo ratings yet

- Lala Lajpat Rai College: Public Relations Project Rough Draft Topic: Nike V/S AdidasDocument34 pagesLala Lajpat Rai College: Public Relations Project Rough Draft Topic: Nike V/S AdidasNikitha Dsouza75% (4)

- Create Config Files Python ConfigParserDocument8 pagesCreate Config Files Python ConfigParserJames NgugiNo ratings yet

- Specijalni Elektrici MasiniDocument22 pagesSpecijalni Elektrici MasiniIgor JovanovskiNo ratings yet

- ReleaseDocument36 pagesReleasebassamrajehNo ratings yet

- Digital Payments in IndiaDocument6 pagesDigital Payments in IndiaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Project ProposalDocument6 pagesProject Proposalapi-386094460No ratings yet

- Vissim 11 - ManualDocument1,219 pagesVissim 11 - Manualmauricionsantos60% (5)

- Group analyzes Sunsilk brand auditDocument49 pagesGroup analyzes Sunsilk brand auditinkLLL0% (1)

- MCB, MCCB, ElcbDocument3 pagesMCB, MCCB, ElcbMonirul Islam0% (1)

- Soft ListDocument21 pagesSoft Listgicox89No ratings yet

- ASTM D 529 - 00 Enclosed Carbon-Arc Exposures of Bituminous MaterialsDocument3 pagesASTM D 529 - 00 Enclosed Carbon-Arc Exposures of Bituminous Materialsalin2005No ratings yet

- January 2023: Top 10 Cited Articles in Computer Science & Information TechnologyDocument32 pagesJanuary 2023: Top 10 Cited Articles in Computer Science & Information TechnologyAnonymous Gl4IRRjzNNo ratings yet

- Gmail - MOM For Plumeria Garden Estate - MyGateDocument1 pageGmail - MOM For Plumeria Garden Estate - MyGateAjit KumarNo ratings yet

- Spouses Aggabao v. Parulan, Jr. and ParulanDocument5 pagesSpouses Aggabao v. Parulan, Jr. and ParulanGeenea VidalNo ratings yet

- 3G Ardzyka Raka R 1910631030065 Assignment 8Document3 pages3G Ardzyka Raka R 1910631030065 Assignment 8Raka RamadhanNo ratings yet

- Delivering Large-Scale IT Projects On Time, On Budget, and On ValueDocument5 pagesDelivering Large-Scale IT Projects On Time, On Budget, and On ValueMirel IonutNo ratings yet

- ELEC 121 - Philippine Popular CultureDocument10 pagesELEC 121 - Philippine Popular CultureMARITONI MEDALLANo ratings yet

- Ultrasonic Pulse Velocity or Rebound MeasurementDocument2 pagesUltrasonic Pulse Velocity or Rebound MeasurementCristina CastilloNo ratings yet