You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Andover Continuum Cyberstation: Installation Guide For Version 1.92Document98 pagesAndover Continuum Cyberstation: Installation Guide For Version 1.92Eden SilveiraNo ratings yet

- 1975 Fairchild TTL MacrologicDocument298 pages1975 Fairchild TTL MacrologickgrhoadsNo ratings yet

- 10 Historical Speeches Nobody Ever HeardDocument20 pages10 Historical Speeches Nobody Ever HeardSumit Roy100% (1)

- Network Routing Basics Understanding IP Routing in Cisco SystemsDocument436 pagesNetwork Routing Basics Understanding IP Routing in Cisco Systemsellybeauty100% (1)

- Cisco - Pre .350-501.by .VCEplus.102q-DEMODocument48 pagesCisco - Pre .350-501.by .VCEplus.102q-DEMOAran PalayanNo ratings yet

- Wereldleiders Op TwitterDocument24 pagesWereldleiders Op TwitterHerman CouwenberghNo ratings yet

- World Health Days 2014: JanuaryDocument2 pagesWorld Health Days 2014: JanuaryIvy Jorene Roman RodriguezNo ratings yet

- TRAI Data Till 31st March, 2014Document19 pagesTRAI Data Till 31st March, 2014Tamanna Bavishi ShahNo ratings yet

- Hepatitis A eDocument1 pageHepatitis A eSumit RoyNo ratings yet

- Hepatitis A eDocument1 pageHepatitis A eSumit RoyNo ratings yet

- Nightingales - Philips Healthcare Tie UpDocument3 pagesNightingales - Philips Healthcare Tie UpSumit RoyNo ratings yet

- Risk Factors From Hepatitis BCDDocument1 pageRisk Factors From Hepatitis BCDSumit RoyNo ratings yet

- Calendário de Jogos Do Mundial de Futebol-Brasil 2014Document0 pagesCalendário de Jogos Do Mundial de Futebol-Brasil 2014Miguel RodriguesNo ratings yet

- World Health Statisitics FullDocument180 pagesWorld Health Statisitics FullClarice SalidoNo ratings yet

- The State of Mobile Advertising in Emerging Countries TLS EmergingMarketsDocument8 pagesThe State of Mobile Advertising in Emerging Countries TLS EmergingMarketsSumit RoyNo ratings yet

- NokiaDocument1 pageNokiaSumit RoyNo ratings yet

- Mediamind Comscore Research Dwelling On EntertainmentDocument20 pagesMediamind Comscore Research Dwelling On EntertainmentSumit RoyNo ratings yet

- Global Top 100 Most Valueable Brands Brandz2014 - Infographic PDFDocument1 pageGlobal Top 100 Most Valueable Brands Brandz2014 - Infographic PDFSumit RoyNo ratings yet

- The State of Airline Marketing Airlinetrends Simpliflying April2013Document21 pagesThe State of Airline Marketing Airlinetrends Simpliflying April2013Sumit RoyNo ratings yet

- Mobile Advertising Research Trends and InsightsDocument15 pagesMobile Advertising Research Trends and InsightsSumit RoyNo ratings yet

- FINAL - Mobile Advertising DeckDocument73 pagesFINAL - Mobile Advertising DecksumitkroyNo ratings yet

- The State of Maternal Health, D Nutrition in Asia " World Vision DataDocument4 pagesThe State of Maternal Health, D Nutrition in Asia " World Vision DataSumit RoyNo ratings yet

- Gender and Social Networking Activity :facebook Vs OthersDocument18 pagesGender and Social Networking Activity :facebook Vs OthersSumit RoyNo ratings yet

- Calendar 14Document57 pagesCalendar 14Hanan AhmedNo ratings yet

- MGI China E-Tailing Executive Summary March 2013Document18 pagesMGI China E-Tailing Executive Summary March 2013Sumit RoyNo ratings yet

- CVD Atlas 16 Death From Stroke PDFDocument1 pageCVD Atlas 16 Death From Stroke PDFRisti KhafidahNo ratings yet

- CEO Survey On Hiring, Profitability and PeopleDocument36 pagesCEO Survey On Hiring, Profitability and PeopleSumit RoyNo ratings yet

- The 5 Free Alternatives To Microsoft WordDocument60 pagesThe 5 Free Alternatives To Microsoft WordSumit RoyNo ratings yet

- The 5 Free Alternatives To Microsoft WordDocument60 pagesThe 5 Free Alternatives To Microsoft WordSumit RoyNo ratings yet

- 2014 Bill and Melinda Gates Foundation Report On Global PovertyDocument28 pages2014 Bill and Melinda Gates Foundation Report On Global PovertySumit RoyNo ratings yet

- India InfographicsDocument3 pagesIndia InfographicsSumit RoyNo ratings yet

- The Evolution of Digital Advertising 3.0: Adobe Research InsightsDocument1 pageThe Evolution of Digital Advertising 3.0: Adobe Research InsightsSumit RoyNo ratings yet

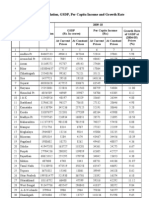

- Statewise GSDP PCI and G.RDocument3 pagesStatewise GSDP PCI and G.RArchit SingalNo ratings yet

- SAP GTT MM App PDFDocument144 pagesSAP GTT MM App PDFJorge FunezNo ratings yet

- Xda-Developers - SECRET CODES - Omnia 2 GT-i8000 PDFDocument3 pagesXda-Developers - SECRET CODES - Omnia 2 GT-i8000 PDFM Arshad Iqbal HarralNo ratings yet

- Hacking LG 32lf2500 and FamilyDocument40 pagesHacking LG 32lf2500 and FamilyAurelia100% (1)

- LABSIM For CompTIA Linux+ (LX0-101, LX0-102 & LPIC-1)Document3 pagesLABSIM For CompTIA Linux+ (LX0-101, LX0-102 & LPIC-1)irshaad010% (3)

- Revathy CVVDocument2 pagesRevathy CVVrevathykaNo ratings yet

- 125K HI RW USB D5 User GuideDocument5 pages125K HI RW USB D5 User GuidejujonetNo ratings yet

- ANX1122 Product Brief 0Document2 pagesANX1122 Product Brief 0Win Ko KoNo ratings yet

- Accident Detection and Alert System For Medical AssistanceDocument2 pagesAccident Detection and Alert System For Medical AssistanceInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Dzamindar MyFAX Brochure Pg5Document1 pageDzamindar MyFAX Brochure Pg5Johnson LukoseNo ratings yet

- Veeam Agent Linux 2 0 User GuideDocument256 pagesVeeam Agent Linux 2 0 User GuideJose X LuisNo ratings yet

- How To Deploy EPGDocument6 pagesHow To Deploy EPGcavendisuNo ratings yet

- Git - First Time Git Setup: WindowsDocument3 pagesGit - First Time Git Setup: WindowsJesica TandonNo ratings yet

- PME Licensing GuideDocument19 pagesPME Licensing GuideYosmir Dario Torres MarchenaNo ratings yet

- UsbeeDocument300 pagesUsbee吳冠儀No ratings yet

- Ccie Clone MasterDocument4 pagesCcie Clone MasterAnonymous qNY1Xcw7RNo ratings yet

- ETSI TS 122 186: 5G Service Requirements For Enhanced V2X Scenarios (3GPP TS 22.186 Version 15.4.0 Release 15)Document18 pagesETSI TS 122 186: 5G Service Requirements For Enhanced V2X Scenarios (3GPP TS 22.186 Version 15.4.0 Release 15)Bruno PintoNo ratings yet

- It Ends With Us - Ebook: Book DetailDocument1 pageIt Ends With Us - Ebook: Book DetailJomaii Cajandoc0% (2)

- SecurePenDrive User Manual Setup GuideDocument11 pagesSecurePenDrive User Manual Setup GuideDipstick072No ratings yet

- Akash Agarwal: Front End DeveloperDocument2 pagesAkash Agarwal: Front End DeveloperakashNo ratings yet

- Speed Control of Single Phase Induction Motor by Android Application Using Wi FiDocument3 pagesSpeed Control of Single Phase Induction Motor by Android Application Using Wi FiInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- WinPanel HelpDocument64 pagesWinPanel HelpisidriskyNo ratings yet

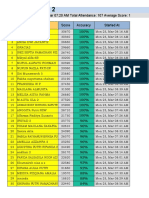

- Matematika 2 Score and Accuracy ReportDocument14 pagesMatematika 2 Score and Accuracy ReportmalindaNo ratings yet

- Eviews PDFDocument2 pagesEviews PDFAshleyNo ratings yet

- JES2Document24 pagesJES2api-3828592No ratings yet

- Writing Games with PygameDocument25 pagesWriting Games with PygameAline OliveiraNo ratings yet

- AMS-RF PDK FlowDocument30 pagesAMS-RF PDK FlowNava KrishnanNo ratings yet