You might also like

- Trade in Audiovisuals Between Physical Trade and E-CommerceDocument5 pagesTrade in Audiovisuals Between Physical Trade and E-CommerceRenato AntoniniNo ratings yet

- Abnormal Values in The EU 1Document16 pagesAbnormal Values in The EU 1Renato AntoniniNo ratings yet

- EU Rules of Origin of Anti-Dumping ProceedingsDocument4 pagesEU Rules of Origin of Anti-Dumping ProceedingsRenato AntoniniNo ratings yet

- Standards of The WTO Agreement On Technical BarriersDocument5 pagesStandards of The WTO Agreement On Technical BarriersRenato AntoniniNo ratings yet

- Transatlantic Trade and Investment PartnershipDocument5 pagesTransatlantic Trade and Investment PartnershipRenato AntoniniNo ratings yet

- Russia in The WTO Challenges and Opportunities For BusinessesDocument5 pagesRussia in The WTO Challenges and Opportunities For BusinessesRenato AntoniniNo ratings yet

- Importers in Good Faith and The Rectification of The Customs DutyDocument5 pagesImporters in Good Faith and The Rectification of The Customs DutyRenato AntoniniNo ratings yet

- EU Restrictive Measures Use of Import RestrictionsDocument2 pagesEU Restrictive Measures Use of Import RestrictionsRenato AntoniniNo ratings yet

- EU Restrictive Measures Use of Import RestrictionsDocument2 pagesEU Restrictive Measures Use of Import RestrictionsRenato AntoniniNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CHAP 11. Fraud AuditingDocument14 pagesCHAP 11. Fraud AuditingNoroNo ratings yet

- LEED Evolution in 40 CharactersDocument2 pagesLEED Evolution in 40 CharactersJoel Jude TadeoNo ratings yet

- The Anti CEO PlaybookDocument8 pagesThe Anti CEO Playbookcherry africaNo ratings yet

- Leather Industry in Tamil NaduDocument6 pagesLeather Industry in Tamil Nadukbk dmNo ratings yet

- Court suit for unpaid Rs. amountDocument3 pagesCourt suit for unpaid Rs. amountIndranil Roy Choudhuri100% (1)

- Withholding Tax (Eng)Document10 pagesWithholding Tax (Eng)WN TV programsNo ratings yet

- Filipinos' Biggest Concern is InflationDocument2 pagesFilipinos' Biggest Concern is InflationPrences Jhewen Albis100% (3)

- Koraput CoffeeDocument23 pagesKoraput CoffeeRupam PratikshyaNo ratings yet

- P3 Fusion Accounting HubDocument21 pagesP3 Fusion Accounting HubAnis Bre100% (1)

- Service Network - 20211007Document14 pagesService Network - 20211007Antonis IsidorouNo ratings yet

- Global Finance OCT20 PDFDocument134 pagesGlobal Finance OCT20 PDFSuchi Roll-erNo ratings yet

- Say Good Bye To Physical Cash and Welcome To Central Bank Digital CurrencyDocument44 pagesSay Good Bye To Physical Cash and Welcome To Central Bank Digital CurrencyJohn TaskinsoyNo ratings yet

- Avoiding Theoretical Stagnation - A Systematic Review and Framework For Measuring Public ValueDocument19 pagesAvoiding Theoretical Stagnation - A Systematic Review and Framework For Measuring Public ValuezooopsNo ratings yet

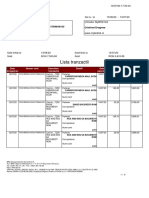

- Lista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaDocument6 pagesLista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaSebastian PSNo ratings yet

- CEO Duality and Firm Performance: The Moderating Roles of CEO Informal Power and Board InvolvementsDocument22 pagesCEO Duality and Firm Performance: The Moderating Roles of CEO Informal Power and Board InvolvementsWihelmina DeaNo ratings yet

- Imposto D Renda em Inglês Tax Return - BrancoDocument5 pagesImposto D Renda em Inglês Tax Return - BrancoAbimaelNo ratings yet

- Land Purchase and Sale Agreement Templates - LegalDocument4 pagesLand Purchase and Sale Agreement Templates - LegalAlekz PicarNo ratings yet

- Erwin DI Business Glossary Management GuideDocument149 pagesErwin DI Business Glossary Management GuideleoluiNo ratings yet

- Letter of Engagement Draft Vlad's Emporium LimitedDocument33 pagesLetter of Engagement Draft Vlad's Emporium LimitedNatali DavydenkoNo ratings yet

- Formal Letters Piddubna Anastasia 302 AnfDocument12 pagesFormal Letters Piddubna Anastasia 302 AnfАнастасия ПоддубнаяNo ratings yet

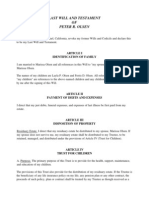

- Will For Parents of Minor ChildrenDocument10 pagesWill For Parents of Minor ChildrenRocketLawyerNo ratings yet

- 5th All India Urban Cooperative Banking Virtual Summit 2021Document3 pages5th All India Urban Cooperative Banking Virtual Summit 2021Rohit SharmaNo ratings yet

- Econyl PresentationDocument33 pagesEconyl PresentationAlexandra PopescuNo ratings yet

- Managing Theatre Resources Post-COVIDDocument17 pagesManaging Theatre Resources Post-COVIDIbironke ShalomNo ratings yet

- Intro To MEASURE PhaseDocument9 pagesIntro To MEASURE PhaseAira_DirectonerNo ratings yet

- NIKE Inc Q117 Press Release PDFDocument8 pagesNIKE Inc Q117 Press Release PDFPitroda BhavinNo ratings yet

- 1185028747.2 en-US - Mining and Rock Excavation Torque SpecificationsDocument24 pages1185028747.2 en-US - Mining and Rock Excavation Torque SpecificationsJuan Yanayaco Ramos100% (1)

- Annexure A - Ritesh Tandon - Morgan Stanley (31VLK)Document1 pageAnnexure A - Ritesh Tandon - Morgan Stanley (31VLK)Ritesh TandonNo ratings yet

- Process Costing Systems: Job vs Process CostingDocument10 pagesProcess Costing Systems: Job vs Process CostingMegan CruzNo ratings yet

- Bosch Common Rail Injector Valve CatalogDocument52 pagesBosch Common Rail Injector Valve CatalogSergioNo ratings yet