You might also like

- Notice To The MarketDocument1 pageNotice To The MarketJBS RINo ratings yet

- Notice To The MarketDocument1 pageNotice To The MarketJBS RINo ratings yet

- Notice To The MarketDocument1 pageNotice To The MarketJBS RINo ratings yet

- JBS S.A. Releases Its 2016 Annual and Sustainability ReportDocument1 pageJBS S.A. Releases Its 2016 Annual and Sustainability ReportJBS RINo ratings yet

- 1Q17 Earnings PresentationDocument15 pages1Q17 Earnings PresentationJBS RINo ratings yet

- JBS S.A. Announces The Conclusion of Plumrose AcquisitionDocument1 pageJBS S.A. Announces The Conclusion of Plumrose AcquisitionJBS RINo ratings yet

- 1Q17 Financial StatementsDocument31 pages1Q17 Financial StatementsJBS RINo ratings yet

- 1Q17 Conference Call TranscriptDocument13 pages1Q17 Conference Call TranscriptJBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On May 08, 2017Document2 pagesMinutes of The Board of Directors' Meeting Held On May 08, 2017JBS RINo ratings yet

- Release and FS 1Q17Document53 pagesRelease and FS 1Q17JBS RINo ratings yet

- Minutes of The Fiscal Council's Meeting Held On May 04, 2017Document2 pagesMinutes of The Fiscal Council's Meeting Held On May 04, 2017JBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On May 05, 2017Document2 pagesMinutes of The Board of Directors' Meeting Held On May 05, 2017JBS RINo ratings yet

- Minutes of The Fiscal Council's Meeting Held On April 05, 2017Document5 pagesMinutes of The Fiscal Council's Meeting Held On April 05, 2017JBS RINo ratings yet

- JBS - Annual and Sustainability Report 2016Document144 pagesJBS - Annual and Sustainability Report 2016JBS RINo ratings yet

- MGMT Report FS 2015 (Reap 2017)Document95 pagesMGMT Report FS 2015 (Reap 2017)JBS RINo ratings yet

- MGMT Report FS 2016 (Reap 2017)Document97 pagesMGMT Report FS 2016 (Reap 2017)JBS RINo ratings yet

- REMOTE VOTING FORM OF OESM To Be Held On April 28, 2017Document5 pagesREMOTE VOTING FORM OF OESM To Be Held On April 28, 2017JBS RINo ratings yet

- JBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngDocument5 pagesJBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngJBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On March 13, 2017Document4 pagesMinutes of The Board of Directors' Meeting Held On March 13, 2017JBS RINo ratings yet

- JBS Institutional Presentation Including 4Q16 and 2016 ResultsDocument24 pagesJBS Institutional Presentation Including 4Q16 and 2016 ResultsJBS RINo ratings yet

- 4Q16 and 2016 Earnings PresentationDocument21 pages4Q16 and 2016 Earnings PresentationJBS RINo ratings yet

- 4Q16 Conference Call TranscriptDocument16 pages4Q16 Conference Call TranscriptJBS RINo ratings yet

- MgmtReport FSDocument96 pagesMgmtReport FSJBS RINo ratings yet

- JBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngDocument4 pagesJBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngJBS RINo ratings yet

- MgmtReport FSDocument96 pagesMgmtReport FSJBS RINo ratings yet

- UntitledDocument4 pagesUntitledJBS RINo ratings yet

- Notice To The Market - Federal Police OperationDocument1 pageNotice To The Market - Federal Police OperationJBS RINo ratings yet

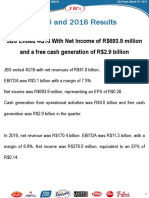

- 4Q16 and 2016 Earnings ReleaseDocument31 pages4Q16 and 2016 Earnings ReleaseJBS RI100% (1)

- MATERIAL FACT - JBS Announces The Acquisition of Plumrose USADocument2 pagesMATERIAL FACT - JBS Announces The Acquisition of Plumrose USAJBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On February 23, 2017Document20 pagesMinutes of The Board of Directors' Meeting Held On February 23, 2017JBS RINo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- AIA Doc Synopses by SeriesDocument43 pagesAIA Doc Synopses by Seriesdupree100% (1)

- Appendix 22 C: Format of Certificate of Payments Issued by The Project AuthorityDocument5 pagesAppendix 22 C: Format of Certificate of Payments Issued by The Project Authorityavijit kundu senco onlineNo ratings yet

- Economic CyclesDocument203 pagesEconomic CyclesMauriNo ratings yet

- Price Theory 2018-2021Document20 pagesPrice Theory 2018-2021Gabriel RoblesNo ratings yet

- ) Presenting The Contribution As A Group of Assets 2: Does Not Equal Pay Receive Is Not DeterminedDocument20 pages) Presenting The Contribution As A Group of Assets 2: Does Not Equal Pay Receive Is Not Determinedايهاب غزالةNo ratings yet

- External Analysis Draft 1Document6 pagesExternal Analysis Draft 1Benjiemar QuirogaNo ratings yet

- International Oil Trader Academy Winter School - Virtual DeliveryDocument6 pagesInternational Oil Trader Academy Winter School - Virtual DeliveryMuslim NasirNo ratings yet

- Material Costing and ControlDocument54 pagesMaterial Costing and ControlFADIASATTNo ratings yet

- Soal BaruDocument14 pagesSoal BaruDella Lina100% (1)

- Segmenting The Business Market and Estimating Segment DemandDocument24 pagesSegmenting The Business Market and Estimating Segment Demandlilian04No ratings yet

- CM2ADocument10 pagesCM2AMike KanyataNo ratings yet

- Tata India 10 ValuationDocument117 pagesTata India 10 ValuationPankaj GuptaNo ratings yet

- 4th Assignment Postponement Strategy in Paint IndustryDocument8 pages4th Assignment Postponement Strategy in Paint IndustryAnjaliNo ratings yet

- CHAPTER 6 - Capital Asset Pricing ModelDocument23 pagesCHAPTER 6 - Capital Asset Pricing Modelemmiliana kasamaNo ratings yet

- Economy Current Affairs by Teju, Nextgen Ias - November 2020Document50 pagesEconomy Current Affairs by Teju, Nextgen Ias - November 2020akshaygmailNo ratings yet

- Principle 6 of EconomicsDocument2 pagesPrinciple 6 of EconomicsAdrian Joseph AlvarezNo ratings yet

- Geisst Monopolies in America PDFDocument368 pagesGeisst Monopolies in America PDFmhtsospap100% (1)

- Partnership FormationDocument3 pagesPartnership FormationRyou ShinodaNo ratings yet

- B.S Studies Pack BookDocument225 pagesB.S Studies Pack Bookjungleman marandaNo ratings yet

- AMAZON.COM - Inc. 2004 overview and analysisDocument45 pagesAMAZON.COM - Inc. 2004 overview and analysisAjay KumarNo ratings yet

- 18 Ubm 306 Financial Management Multiple Choice Questions. Unit-IDocument78 pages18 Ubm 306 Financial Management Multiple Choice Questions. Unit-IrohitthalalNo ratings yet

- BankingDocument3 pagesBankingTamanna MulchandaniNo ratings yet

- Netflix: Submitted By:-Avinash Kumar 19022 Core 1Document11 pagesNetflix: Submitted By:-Avinash Kumar 19022 Core 1Aastha GiriNo ratings yet

- MERALCODocument10 pagesMERALCOKatRobesDeCastroNo ratings yet

- Sales PromotionDocument22 pagesSales PromotionHina QureshiNo ratings yet

- Maths for Business Lecture NotesDocument176 pagesMaths for Business Lecture NotesBảo GiangNo ratings yet

- Fly Ash Brick ProjectDocument4 pagesFly Ash Brick ProjectJeremy Ruiz100% (4)

- Csat Feb 2011Document31 pagesCsat Feb 2011meherbaba_prasadNo ratings yet

- Mba 3 Sem Corporate Financial Management Group B Financial Management Paper 1 Summer 2018Document3 pagesMba 3 Sem Corporate Financial Management Group B Financial Management Paper 1 Summer 2018pranali nagleNo ratings yet

- Manacc Online QuizDocument3 pagesManacc Online QuizJoshuaTagayunaNo ratings yet