You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- How To Trade Options - 12 Tenets of Daily Trade DisciplineDocument2 pagesHow To Trade Options - 12 Tenets of Daily Trade DisciplineHome Options TradingNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Chart of AccountsDocument8 pagesChart of AccountsMariaCarlaMañagoNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Robles v. YapcincoDocument2 pagesRobles v. YapcincoRem SerranoNo ratings yet

- Money Flow IndexDocument8 pagesMoney Flow IndexShahzad DalalNo ratings yet

- MBA Finance Thesis Topics: Stock Analysis, Mutual Funds, Banks, InsuranceDocument2 pagesMBA Finance Thesis Topics: Stock Analysis, Mutual Funds, Banks, InsuranceSalman Rahi100% (2)

- B.Ethics (Part 2)Document110 pagesB.Ethics (Part 2)Hamza KianiNo ratings yet

- Stock Market Scams in India: A Historical Overview (1991-PresentDocument16 pagesStock Market Scams in India: A Historical Overview (1991-Presentsachincool0100% (2)

- BYD Company's Growth in Automotive and Battery BusinessesDocument7 pagesBYD Company's Growth in Automotive and Battery BusinessesYograj Singh ChauhanNo ratings yet

- How to Invest in Gold: Spot Markets, Futures, ETFs, Bars and CoinsDocument5 pagesHow to Invest in Gold: Spot Markets, Futures, ETFs, Bars and CoinsLeonard NgNo ratings yet

- APCF Research Grant Starch Final Report 2017 October 2017Document177 pagesAPCF Research Grant Starch Final Report 2017 October 2017kyaq001No ratings yet

- Basic Question and Answer On ComputerDocument16 pagesBasic Question and Answer On ComputerSalman RahiNo ratings yet

- Financial Detective Case AnalysisDocument11 pagesFinancial Detective Case AnalysisBrian AlmeidaNo ratings yet

- Question Bank For The Final ExamDocument2 pagesQuestion Bank For The Final ExamRaktim100% (1)

- Mis of DellDocument17 pagesMis of DellMohammad Al Amin71% (7)

- Fin. Analysis MBA Fall. 2015Document4 pagesFin. Analysis MBA Fall. 2015Salman RahiNo ratings yet

- OIL Development Limited: & GAS CompanyDocument1 pageOIL Development Limited: & GAS CompanySalman RahiNo ratings yet

- Research Proposal of Hunain, Majid and SalmanDocument13 pagesResearch Proposal of Hunain, Majid and SalmanSalman RahiNo ratings yet

- Subject: Application For The Post of Junior AssistantDocument1 pageSubject: Application For The Post of Junior AssistantSalman RahiNo ratings yet

- Is There A Future For International BanksDocument20 pagesIs There A Future For International BanksSalman RahiNo ratings yet

- Kraus & Litzenberger, 1976 Homaifar & Graddy, 1988 Fang & Lai, 1997Document2 pagesKraus & Litzenberger, 1976 Homaifar & Graddy, 1988 Fang & Lai, 1997Salman RahiNo ratings yet

- Risk and Return QuestionsDocument1 pageRisk and Return QuestionsSalman RahiNo ratings yet

- Time Table For Spring 2015: Masters of Business AdministrationDocument1 pageTime Table For Spring 2015: Masters of Business AdministrationSalman RahiNo ratings yet

- How To Give References and CitationsDocument5 pagesHow To Give References and CitationsSalman RahiNo ratings yet

- NHA1 - Stress in Simple and Complex WordsDocument18 pagesNHA1 - Stress in Simple and Complex Words08AV2D78% (18)

- BEJ-10 Vol2010Document9 pagesBEJ-10 Vol2010Agung WicaksonoNo ratings yet

- Title Page of The Assignment ARM Litrature ReviewDocument1 pageTitle Page of The Assignment ARM Litrature ReviewSalman RahiNo ratings yet

- Case of WaccDocument2 pagesCase of WaccSalman RahiNo ratings yet

- 15 Answers To All ProblemsDocument25 pages15 Answers To All ProblemsPushpa BaruaNo ratings yet

- GEDocument6 pagesGESalman RahiNo ratings yet

- 7Cs Effective Business CommunicationDocument23 pages7Cs Effective Business CommunicationSalman Rahi100% (1)

- MGT Assignment Basic Elements of Control in RganizationDocument31 pagesMGT Assignment Basic Elements of Control in RganizationSalman RahiNo ratings yet

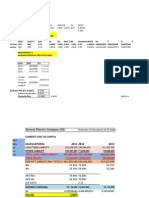

- Income Statement: Dec 31, 2009 Dec 31, 2008 Dec 31, 2007 Total Revenue 796,800 1,042,800 1,112,900Document2 pagesIncome Statement: Dec 31, 2009 Dec 31, 2008 Dec 31, 2007 Total Revenue 796,800 1,042,800 1,112,900Salman RahiNo ratings yet

- B RecorderDocument5 pagesB RecorderMuhammad HishamNo ratings yet

- Merce and SecurityDocument48 pagesMerce and SecuritySalman RahiNo ratings yet

- Introduction to MCB Islamic Banking Deposit and Financing SchemesDocument24 pagesIntroduction to MCB Islamic Banking Deposit and Financing SchemesSalman RahiNo ratings yet

- Tenses MADE EASY BY SALMAN RAHIDocument1 pageTenses MADE EASY BY SALMAN RAHISalman RahiNo ratings yet

- Ratio AnalysisDocument10 pagesRatio AnalysisSalman RahiNo ratings yet

- P 6 KK 6 UDocument33 pagesP 6 KK 6 URichard OonNo ratings yet

- International Business & Trade Research Paper ReviewDocument3 pagesInternational Business & Trade Research Paper ReviewKiyan YunNo ratings yet

- Fixed Income Analyst Jan 2023Document2 pagesFixed Income Analyst Jan 2023FransNo ratings yet

- ALFI and ABBL Guidelines and Recommendations For Depositaries Safekeeping of Other AssetsDocument62 pagesALFI and ABBL Guidelines and Recommendations For Depositaries Safekeeping of Other AssetsludivineNo ratings yet

- Chapter9 - FinalDocument17 pagesChapter9 - FinalbraveusmanNo ratings yet

- A Study On Market Analysis On Life Insurance CompanyDocument52 pagesA Study On Market Analysis On Life Insurance CompanyNitin DubeyNo ratings yet

- Báo Cáo Thực TậpDocument35 pagesBáo Cáo Thực TậpTuấn HuỳnhNo ratings yet

- Periasamy Resume 08.11.19Document13 pagesPeriasamy Resume 08.11.19Pandy PeriasamyNo ratings yet

- AFA QuizDocument15 pagesAFA QuizNoelia Mc DonaldNo ratings yet

- Comparative Financial Analysis of Tata Steel and SAILDocument53 pagesComparative Financial Analysis of Tata Steel and SAILManu GCNo ratings yet

- Ch10 TB RankinDocument6 pagesCh10 TB RankinAnton Vitali100% (1)

- Business Incubators SystemDocument31 pagesBusiness Incubators SystemPrashanth KumarNo ratings yet

- Test Bank For Investments Analysis and Management 12th Edition JonesDocument38 pagesTest Bank For Investments Analysis and Management 12th Edition Jonessidneynash9mc5100% (14)

- MarriottDocument10 pagesMarriottimwkyaNo ratings yet

- CFO Tax Partner CPA in Houston TX Resume Darryl SiefkasDocument3 pagesCFO Tax Partner CPA in Houston TX Resume Darryl SiefkasDarrylSiefkasNo ratings yet

- Chapter 2Document3 pagesChapter 2AyylmaoNo ratings yet

- Airport BackgroundDocument27 pagesAirport Backgroundseanne07No ratings yet

- Sales Quota - All Types of QuotaDocument17 pagesSales Quota - All Types of QuotaSunny Bharatbhai Gandhi100% (2)

- Three questions to grow your investment returnsDocument21 pagesThree questions to grow your investment returnsMOVIES SHOPNo ratings yet