You might also like

- Technical Proposal Template SampleDocument12 pagesTechnical Proposal Template SampleWrite Bagga100% (1)

- India's Economic Crisis and Reforms 1991-2008Document15 pagesIndia's Economic Crisis and Reforms 1991-2008Insha RahmanNo ratings yet

- How Guide SapcreditmanageDocument4 pagesHow Guide SapcreditmanagepoornaraoNo ratings yet

- Economic Liberalization in India: Past Achievements and Future ChallengesDocument55 pagesEconomic Liberalization in India: Past Achievements and Future ChallengesEr Arvind NagdaNo ratings yet

- LPG and the Indian Economy: An Analysis of Liberalization, Privatization and GlobalizationDocument40 pagesLPG and the Indian Economy: An Analysis of Liberalization, Privatization and Globalizationsowmya sNo ratings yet

- Trade As An Engine For Growth-Developing EconomiesDocument57 pagesTrade As An Engine For Growth-Developing EconomiesAmit BehalNo ratings yet

- Economic Reforms in IndiaDocument14 pagesEconomic Reforms in IndiaRajat Suri100% (2)

- Can India Make It To The League of Economics' Superpower in The Next 25 Yrs?Document35 pagesCan India Make It To The League of Economics' Superpower in The Next 25 Yrs?zydeco.14100% (3)

- Impact of Globalization On Indian EconomyDocument33 pagesImpact of Globalization On Indian EconomySrikanth ReddyNo ratings yet

- IM Proj Done...Document31 pagesIM Proj Done...Sohham ParingeNo ratings yet

- Lecture 3 MGN 101Document32 pagesLecture 3 MGN 101Taukir SiddiqueNo ratings yet

- Globalization and India: Iipm SMDocument24 pagesGlobalization and India: Iipm SMRAJIV SINGHNo ratings yet

- Fesf PDFDocument32 pagesFesf PDFameeNo ratings yet

- Unit11 LPGDocument15 pagesUnit11 LPGVivek AdateNo ratings yet

- Paradigm Shift in Indian Economy: Presentation ByDocument21 pagesParadigm Shift in Indian Economy: Presentation Bysharukh1No ratings yet

- New Economic Policy of 1991Document20 pagesNew Economic Policy of 1991Chetan PanaraNo ratings yet

- Fastest Growing Free Market Democracy in A Global Economy IndiaDocument101 pagesFastest Growing Free Market Democracy in A Global Economy IndiaPrakashNo ratings yet

- Indian EconomyDocument20 pagesIndian Economysyedzakiali333No ratings yet

- India's Fastest Growing Free Market Democracy in a Global EconomyDocument101 pagesIndia's Fastest Growing Free Market Democracy in a Global EconomymanowjjNo ratings yet

- Economic Development in IndiaDocument14 pagesEconomic Development in IndiaKaran ShahNo ratings yet

- India's growth story from 1991-2019: Top performing sectorsDocument5 pagesIndia's growth story from 1991-2019: Top performing sectorsdacchuNo ratings yet

- Indian Economy: An OverviewDocument44 pagesIndian Economy: An OverviewkundankarnNo ratings yet

- Emerging Sectors in Indian EconomyDocument4 pagesEmerging Sectors in Indian EconomyManoj TiwariNo ratings yet

- Effects of India's Growth On The Global Economy and EnvironmentDocument25 pagesEffects of India's Growth On The Global Economy and EnvironmentPankaj YadavNo ratings yet

- Analysis WallstreetDocument11 pagesAnalysis WallstreetNinadTambeNo ratings yet

- GLOBALIZATION AND INTERNATIONAL BUSINESS: INDIA'S PERSPECTIVEDocument24 pagesGLOBALIZATION AND INTERNATIONAL BUSINESS: INDIA'S PERSPECTIVEgeetika1629No ratings yet

- Main Article:: India FollowedDocument44 pagesMain Article:: India Followedmohit_tandel8No ratings yet

- Assessing Overall Business Environment in Indian EconomyDocument22 pagesAssessing Overall Business Environment in Indian Economyshivamkarir03No ratings yet

- Commercial Policy Drives Economic GrowthDocument16 pagesCommercial Policy Drives Economic GrowthGautam SahaNo ratings yet

- History: Management Joint-Venture Transfer of Technology Expertise InvestmentDocument12 pagesHistory: Management Joint-Venture Transfer of Technology Expertise InvestmentMonika SharmaNo ratings yet

- Economic Reforms Since 1991 or New Economic PolicyDocument41 pagesEconomic Reforms Since 1991 or New Economic PolicyGeeta GhaiNo ratings yet

- India's Rise as a Top Global Investment HubDocument38 pagesIndia's Rise as a Top Global Investment HubNagmani SrivastavaNo ratings yet

- IEPDocument50 pagesIEPK.muniNo ratings yet

- Indian Economy Broad Features: AvraoDocument37 pagesIndian Economy Broad Features: AvraoAakash Singh SuryvanshiNo ratings yet

- Globalisation and Its Impact On Financial ServicesDocument30 pagesGlobalisation and Its Impact On Financial ServicesLairenlakpam Mangal100% (3)

- The Impact of Globalization On Indian EconomyDocument15 pagesThe Impact of Globalization On Indian Economyronik25No ratings yet

- Tiger V/S DragonDocument25 pagesTiger V/S DragonAmol KareNo ratings yet

- India Completing Inv UniverseDocument16 pagesIndia Completing Inv UniverseKushal ManupatiNo ratings yet

- Present Status of Indian IndustryDocument20 pagesPresent Status of Indian IndustryAka AkNo ratings yet

- Globalization & LiberalizationDocument12 pagesGlobalization & Liberalizationmitul-desai-8682No ratings yet

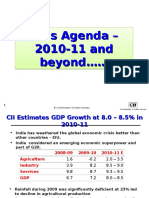

- CII's AgendaDocument31 pagesCII's AgendaPremkumarJittaNo ratings yet

- European Business Group - India and Retail Landscape 4th Feb 10v1 5Document21 pagesEuropean Business Group - India and Retail Landscape 4th Feb 10v1 59827005212No ratings yet

- Retail Evolution, Trends & Opportunities in IndiaDocument21 pagesRetail Evolution, Trends & Opportunities in IndiabhuppibhuvanNo ratings yet

- FDI A Catalyst For Growth of The Textile & Apparel IndustryDocument10 pagesFDI A Catalyst For Growth of The Textile & Apparel Industryshobu_iujNo ratings yet

- Effects of Globalization On Indian Industry Started When The Government Opened The CountryDocument5 pagesEffects of Globalization On Indian Industry Started When The Government Opened The Countryjimmynarangs100% (1)

- Executive Summary: Cement IndustryDocument81 pagesExecutive Summary: Cement IndustrySankaraharan ShanmugamNo ratings yet

- 4A. Small BusinessesDocument21 pages4A. Small Businessesditemiy411No ratings yet

- China Import Forum 2013: Presentation On Indian IndustryDocument19 pagesChina Import Forum 2013: Presentation On Indian IndustryGourav Batheja classesNo ratings yet

- BEP Presentation: Course Instructor: Prof. Sibananda SenapatiDocument93 pagesBEP Presentation: Course Instructor: Prof. Sibananda Senapatisi ranNo ratings yet

- Indian Pharma IndustryDocument60 pagesIndian Pharma Industrysushantmishra85100% (55)

- Padma Awards 2020 Announced: WWW - Careerpower.in Adda247 AppDocument1 pagePadma Awards 2020 Announced: WWW - Careerpower.in Adda247 AppnagarajuNo ratings yet

- Executive Summary: Cement IndustryDocument97 pagesExecutive Summary: Cement Industryst miraNo ratings yet

- India's cement industry outpaces China's growthDocument92 pagesIndia's cement industry outpaces China's growthAbdulgafoor NellogiNo ratings yet

- CBSE Class 11 Economics: Appraisal of Indian Economic ReformsDocument6 pagesCBSE Class 11 Economics: Appraisal of Indian Economic ReformsAyush LohiyaNo ratings yet

- Changing Economic Environment of IndiaDocument55 pagesChanging Economic Environment of Indiarajat_singlaNo ratings yet

- Industrial Report on Bharat Petroleum Corporation LimitedDocument67 pagesIndustrial Report on Bharat Petroleum Corporation LimitedSunny ThakurNo ratings yet

- Indian Economy: Presented By: Pavan P Kannav Roll No: G-45Document12 pagesIndian Economy: Presented By: Pavan P Kannav Roll No: G-45pavan_kannavNo ratings yet

- GlobalDocument30 pagesGlobalsriharshagNo ratings yet

- Final PrintDocument24 pagesFinal PrintSwapnil AmbawadeNo ratings yet

- Micro, Small and Medium Enterprises (Msme) : MBA113 (SCIM)Document29 pagesMicro, Small and Medium Enterprises (Msme) : MBA113 (SCIM)thakurjNo ratings yet

- Bye Laws PuneDocument20 pagesBye Laws PuneSaurabh BadjateNo ratings yet

- Tips Related To Vastu: Business DiagnosticsDocument21 pagesTips Related To Vastu: Business DiagnosticsSagar BhoiNo ratings yet

- Water TreatmentDocument17 pagesWater TreatmentSaurabh BadjateNo ratings yet

- Sus ConsDocument12 pagesSus ConsSaurabh BadjateNo ratings yet

- Realestate CHK ListDocument2 pagesRealestate CHK ListSaurabh BadjateNo ratings yet

- Tips Related To Vastu: Business DiagnosticsDocument21 pagesTips Related To Vastu: Business DiagnosticsSagar BhoiNo ratings yet

- Realestate CHK ListDocument2 pagesRealestate CHK ListSaurabh BadjateNo ratings yet

- Maharashtra Land Revenue Code 1966 PDFDocument118 pagesMaharashtra Land Revenue Code 1966 PDFAmol RautNo ratings yet

- Maharashtra Land Revenue Code 1966 PDFDocument118 pagesMaharashtra Land Revenue Code 1966 PDFAmol RautNo ratings yet

- Earthquake Effect On BuildingDocument11 pagesEarthquake Effect On BuildingSaurabh Badjate100% (1)

- Earth Quake DamagesDocument25 pagesEarth Quake DamagesSaurabh BadjateNo ratings yet

- STAIRSDocument14 pagesSTAIRSSaurabh BadjateNo ratings yet

- 11188-04 InstructivoDocument20 pages11188-04 InstructivoLuis AlonsoNo ratings yet

- Scrum PDFDocument222 pagesScrum PDFvive_vt_vivasNo ratings yet

- Hospital Design and Infrastructure 2012Document8 pagesHospital Design and Infrastructure 2012milham09No ratings yet

- Evaluation of Fire Protection Systems in Commercial HighrisesDocument9 pagesEvaluation of Fire Protection Systems in Commercial HighrisesPrithvi RajNo ratings yet

- Purchasing Audit ProgrammeDocument12 pagesPurchasing Audit ProgrammemercymabNo ratings yet

- INWARD INSPECTION - MVR - Material Verification ReportsDocument1 pageINWARD INSPECTION - MVR - Material Verification ReportsvinothNo ratings yet

- LINCOLN Lubrication Centro - MaticDocument53 pagesLINCOLN Lubrication Centro - Maticrmartinf2527No ratings yet

- KB - ETA - Printable - PDF - VNX Drive Firmware UpgradeDocument5 pagesKB - ETA - Printable - PDF - VNX Drive Firmware UpgradeAshley DouglasNo ratings yet

- Faurecia Automotive Maneser NSF Project Time Plan PS Trails (6152)Document2 pagesFaurecia Automotive Maneser NSF Project Time Plan PS Trails (6152)Tushar KohinkarNo ratings yet

- Product Overview - LeuschDocument32 pagesProduct Overview - Leuschprihartono_diasNo ratings yet

- Case Study On Ford Motor CompanyDocument5 pagesCase Study On Ford Motor CompanySteveNo ratings yet

- ZARGES K 470 Universal Box - 40678Document3 pagesZARGES K 470 Universal Box - 40678Phee Beng HweeNo ratings yet

- China Vaseline White Petroleum Jelly - Snow White Vaseline - China Vaseline White, Petroleum Jelly PDFDocument3 pagesChina Vaseline White Petroleum Jelly - Snow White Vaseline - China Vaseline White, Petroleum Jelly PDFIstianah Achy HaeruddinNo ratings yet

- 1 Drilling Engineering IIDocument235 pages1 Drilling Engineering IIKarwan Dilmany100% (7)

- ServiceManuals LG Washing WD1015FB WD-1015FB Service ManualDocument35 pagesServiceManuals LG Washing WD1015FB WD-1015FB Service ManualMicu Adrian DanutNo ratings yet

- V2 I4 Naniwa Newsletter OFFICIALDocument4 pagesV2 I4 Naniwa Newsletter OFFICIALNigelNo ratings yet

- Engineering - Reasoning - Critical ThinkingDocument25 pagesEngineering - Reasoning - Critical ThinkingLoseHeartNo ratings yet

- Professional Resume (HVAC & Utilities Manager) - 1Document3 pagesProfessional Resume (HVAC & Utilities Manager) - 1Mujtaba AliNo ratings yet

- BigData & DWH-BI Architect ProfileDocument8 pagesBigData & DWH-BI Architect ProfiledharmendardNo ratings yet

- How To Make Better Decisions: The Importance of Creative Problem Solving in Business and LifeDocument11 pagesHow To Make Better Decisions: The Importance of Creative Problem Solving in Business and LifeNagaPrasannaKumarKakarlamudi100% (1)

- Microsign PresentationDocument27 pagesMicrosign PresentationMicrosign ProductsNo ratings yet

- Volvo Cars Sustainability Report 2013Document64 pagesVolvo Cars Sustainability Report 2013JM MANOJKUMARNo ratings yet

- NCAR AIP 2010 AerodromeDocument170 pagesNCAR AIP 2010 AerodromeAbhishek Man ShresthaNo ratings yet

- Geomatics Lab ModuleDocument6 pagesGeomatics Lab ModuleCt Kamariah Md SaatNo ratings yet

- Cross Company Sales ConfigurationDocument70 pagesCross Company Sales Configurationnelsondarla1275% (4)

- Hoke Gyrolok FittingDocument6 pagesHoke Gyrolok FittingHendra CiptanegaraNo ratings yet

- Thesis - PHD - 2014 - Grid Connected Doubly Fed Induction Generator Based Wind Turbine Under LVRTDocument198 pagesThesis - PHD - 2014 - Grid Connected Doubly Fed Induction Generator Based Wind Turbine Under LVRTjose-consuelo100% (1)