You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Reading Comprehension Animals Copyright English Created Resources PDFDocument10 pagesReading Comprehension Animals Copyright English Created Resources PDFCasillas ElNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- ThiruppavaiDocument157 pagesThiruppavaiajiva_rts100% (49)

- Understanding Death Through the Life SpanDocument52 pagesUnderstanding Death Through the Life SpanKaren HernandezNo ratings yet

- 2023 Civil LawDocument7 pages2023 Civil LawJude OnrubiaNo ratings yet

- Exam 2 Study GuideDocument11 pagesExam 2 Study GuideAnonymous ewJy7jyvNNo ratings yet

- CES Wrong Answer SummaryDocument4 pagesCES Wrong Answer SummaryZorg UANo ratings yet

- Fernández Kelly - Death in Mexican Folk CultureDocument21 pagesFernández Kelly - Death in Mexican Folk CultureantoniadelateNo ratings yet

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

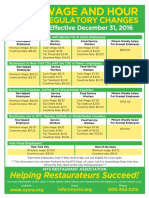

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- Myanmar Thilawa SEZ ProspectusDocument92 pagesMyanmar Thilawa SEZ ProspectusfrancistsyNo ratings yet

- ĐỀ MINH HỌA 15-19Document25 pagesĐỀ MINH HỌA 15-19Trung Vũ ThànhNo ratings yet

- Focus2 2E Review Test 4 Units1 8 Vocabulary Grammar UoE Reading GroupBDocument4 pagesFocus2 2E Review Test 4 Units1 8 Vocabulary Grammar UoE Reading GroupBaides1sonNo ratings yet

- Specification For Corrugated Bitumen Roofing Sheets: Indian StandardDocument10 pagesSpecification For Corrugated Bitumen Roofing Sheets: Indian StandardAmanulla KhanNo ratings yet

- Doubles and Doppelgangers: Religious Meaning For The Young and OldDocument12 pagesDoubles and Doppelgangers: Religious Meaning For The Young and Old0 1No ratings yet

- MA KP3-V2H-2 enDocument155 pagesMA KP3-V2H-2 enJavier MiramontesNo ratings yet

- Product Data: Real-Time Frequency Analyzer - Type 2143 Dual Channel Real-Time Frequency Analyzers - Types 2144, 2148/7667Document12 pagesProduct Data: Real-Time Frequency Analyzer - Type 2143 Dual Channel Real-Time Frequency Analyzers - Types 2144, 2148/7667jhon vargasNo ratings yet

- FINAL Conflicts 2019 Official Guidelines PDFDocument48 pagesFINAL Conflicts 2019 Official Guidelines PDFxsar_xNo ratings yet

- Talha Farooqi - Assignment 01 - Overview of Bond Sectors and Instruments - Fixed Income Analysis PDFDocument4 pagesTalha Farooqi - Assignment 01 - Overview of Bond Sectors and Instruments - Fixed Income Analysis PDFMohammad TalhaNo ratings yet

- Tarea 1Document36 pagesTarea 1LUIS RVNo ratings yet

- Ganuelas v. CawedDocument4 pagesGanuelas v. CawedHanna AlfantaNo ratings yet

- The Cult of Demeter On Andros and The HDocument14 pagesThe Cult of Demeter On Andros and The HSanNo ratings yet

- Introduction To Intelligent BuildingsDocument3 pagesIntroduction To Intelligent Buildingsmamta jainNo ratings yet

- The Son of Man Rides The Clouds Pt. 2b - Answering Islam BlogDocument5 pagesThe Son of Man Rides The Clouds Pt. 2b - Answering Islam BlogbenciusilviuNo ratings yet

- Innovations in Teaching-Learning ProcessDocument21 pagesInnovations in Teaching-Learning ProcessNova Rhea GarciaNo ratings yet

- Chemistry The Molecular Science 5th Edition Moore Solutions Manual 1Document36 pagesChemistry The Molecular Science 5th Edition Moore Solutions Manual 1josephandersonxqwbynfjzk100% (27)

- Yoga For The Primary Prevention of Cardiovascular Disease (Hartley 2014)Document52 pagesYoga For The Primary Prevention of Cardiovascular Disease (Hartley 2014)Marcelo NorisNo ratings yet

- Plants Promoting Happiness: The Effect of Indoor Plants on MoodDocument11 pagesPlants Promoting Happiness: The Effect of Indoor Plants on MoodWil UfanaNo ratings yet

- Miles and Snow's Organizational StrategiesDocument15 pagesMiles and Snow's Organizational StrategiesVirat SahNo ratings yet

- PERTANYAAN INTERVIEW WinaDocument2 pagesPERTANYAAN INTERVIEW WinaDidi SetiadiNo ratings yet

- SMS Romantis Bhs Inggris Buat Pacar TercintaDocument5 pagesSMS Romantis Bhs Inggris Buat Pacar TercintaAdnan MaruliNo ratings yet

- Java Thread Priority in MultithreadingDocument3 pagesJava Thread Priority in MultithreadingMITALI SHARMANo ratings yet

- The Names & Atributes of Allah - Abdulillah LahmamiDocument65 pagesThe Names & Atributes of Allah - Abdulillah LahmamiPanthera_No ratings yet