You might also like

- Dimensions of Working Capital ManagementDocument22 pagesDimensions of Working Capital ManagementRamana Rao V GuthikondaNo ratings yet

- Project Report on Working Capital ManagementDocument35 pagesProject Report on Working Capital Managementomprakash shindeNo ratings yet

- Auditing Standards in IndiaDocument8 pagesAuditing Standards in IndiaInderdeep SharmaNo ratings yet

- SHRM-2marks NEWDocument15 pagesSHRM-2marks NEWjohnpratheesh100% (2)

- Procedures To Obtain Export FinanceDocument3 pagesProcedures To Obtain Export FinanceVajju ThoutiNo ratings yet

- A Study On Credit Management at District CoDocument86 pagesA Study On Credit Management at District CoIMAM JAVOOR100% (2)

- PCA & RD Bank PDFDocument86 pagesPCA & RD Bank PDFmohan ks100% (2)

- Recruitment and Selection in Reliance Retail-1Document69 pagesRecruitment and Selection in Reliance Retail-1Pallavi MeghnaNo ratings yet

- Features of SecuritizationDocument37 pagesFeatures of Securitizationhakec100% (2)

- Problems in Receivables ManagementDocument2 pagesProblems in Receivables ManagementSushant GuptaNo ratings yet

- Optimize Working Capital ManagementDocument8 pagesOptimize Working Capital ManagementAnnapurna VinjamuriNo ratings yet

- Unit-II ADocument26 pagesUnit-II APaytm KaroNo ratings yet

- Account for Special Types of Individual CustomersDocument14 pagesAccount for Special Types of Individual CustomersSubodh Kumar Sharma0% (1)

- Funds Flow and Cash Flow NotesDocument12 pagesFunds Flow and Cash Flow NotesSoumendra RoyNo ratings yet

- Case Study All PDFDocument172 pagesCase Study All PDFDr-Shefali GargNo ratings yet

- Recruitment, SelectionDocument63 pagesRecruitment, SelectionAkshay Shah100% (1)

- Factors Affect Factors Affecting Working Capitaling Working CapitalDocument24 pagesFactors Affect Factors Affecting Working Capitaling Working Capitalranjita kelageriNo ratings yet

- Presentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDDocument12 pagesPresentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDEra ChaudharyNo ratings yet

- Funds Flow StatementDocument11 pagesFunds Flow Statementkulife50% (4)

- Pre Issue ManagementDocument19 pagesPre Issue Managementbs_sharathNo ratings yet

- Vuoap01 0406 - Mba 201Document17 pagesVuoap01 0406 - Mba 201prayas sarkarNo ratings yet

- Research Project On Financial LeverageDocument42 pagesResearch Project On Financial LeverageMarryam Majeed63% (8)

- Increased Concern of HRMDocument30 pagesIncreased Concern of HRMAishwarya Chachad33% (3)

- Financial Management (I-Mba V) Important Questions (Module 1&3) (I.e. Asked in GTU Question Papers)Document2 pagesFinancial Management (I-Mba V) Important Questions (Module 1&3) (I.e. Asked in GTU Question Papers)Sabhaya Chirag100% (2)

- Working Capital Requirement QuestionsDocument2 pagesWorking Capital Requirement QuestionsVIRAL DOSHI100% (1)

- NBHI - JD - Next Gen Agency ManagerDocument3 pagesNBHI - JD - Next Gen Agency ManagerHemanth SNo ratings yet

- Fund Flow StatementDocument7 pagesFund Flow StatementvipulNo ratings yet

- Unit III Amalgamation With Respect To A.S - 14 Purchase ConsiderationDocument17 pagesUnit III Amalgamation With Respect To A.S - 14 Purchase ConsiderationPaulomi LahaNo ratings yet

- MBFS Question Bank & AnswersDocument17 pagesMBFS Question Bank & AnswersArunkumar JwNo ratings yet

- SBI & BMB MergerDocument12 pagesSBI & BMB MergerShubham naharwal (PGDM 17-19)No ratings yet

- Tandon Committee PresentationDocument13 pagesTandon Committee PresentationNitharshini Kannan0% (1)

- Funds Flow AnalysisDocument20 pagesFunds Flow AnalysisRajeevAgrawalNo ratings yet

- Mkt-Lab Assignment Book ReviewDocument11 pagesMkt-Lab Assignment Book ReviewRishabh Khichi100% (2)

- Presentation on Amalgamation and Merger of BanksDocument14 pagesPresentation on Amalgamation and Merger of BanksKrishnakant Mishra100% (1)

- A Study On EBIT-EPS Analysis and Its Impact On Profitability of Reliance IndustriesDocument31 pagesA Study On EBIT-EPS Analysis and Its Impact On Profitability of Reliance IndustriesKalyani Rao67% (3)

- Kotak Mahindra BankDocument13 pagesKotak Mahindra BankKunal Singh100% (1)

- A study on Productivity and Analysis for Retail Liabilities Business at Suryoday Small Finance BankDocument36 pagesA study on Productivity and Analysis for Retail Liabilities Business at Suryoday Small Finance BankRameshwari Pillai0% (1)

- Summer Project Report ON: " Working Capital in Icici Bank of India"Document70 pagesSummer Project Report ON: " Working Capital in Icici Bank of India"JaiHanumankiNo ratings yet

- Human Resource Project Report: Recruitment & SelectionDocument14 pagesHuman Resource Project Report: Recruitment & SelectionharshitvaNo ratings yet

- Synergy and Dysergy: Understanding Positive and Negative EffectsDocument2 pagesSynergy and Dysergy: Understanding Positive and Negative EffectsTitus ClementNo ratings yet

- Legal and Procedural Aspects of MergerDocument8 pagesLegal and Procedural Aspects of MergerAnkit Kumar (B.A. LLB 16)No ratings yet

- Final PHD Commerce Thesis PDFDocument450 pagesFinal PHD Commerce Thesis PDFMegha Jain BhandariNo ratings yet

- Calculating financial metrics and terminal value from corporate dataDocument5 pagesCalculating financial metrics and terminal value from corporate datapachpind jayeshNo ratings yet

- Mba 4th Sem Syllabus....Document5 pagesMba 4th Sem Syllabus....MOHAMMED SHEBEER A50% (2)

- 12th BK Question Paper 2023Document11 pages12th BK Question Paper 2023yashashreebhurke333100% (1)

- Training Development Report Index Table Contents Acme TelepowersDocument40 pagesTraining Development Report Index Table Contents Acme TelepowersFaizan Billoo KhanNo ratings yet

- Income From Salary Final SEM 3Document49 pagesIncome From Salary Final SEM 3Baleshwar ChauhanNo ratings yet

- Consumer FinanceDocument17 pagesConsumer FinanceVaishali Trivedi OjhaNo ratings yet

- Final Summer Training Report Mohit PalDocument110 pagesFinal Summer Training Report Mohit Palbharat sachdevaNo ratings yet

- SBI's HR development focuses on staffDocument8 pagesSBI's HR development focuses on staffShraddha KshirsagarNo ratings yet

- Chapter (4) : Fund Flow Statements: Saoud Chayed MashkourDocument18 pagesChapter (4) : Fund Flow Statements: Saoud Chayed MashkourParamesh Miracle100% (1)

- Synopsis Ratio AnalysisDocument2 pagesSynopsis Ratio Analysismoshiurrah0% (2)

- External MobilityDocument12 pagesExternal MobilityRishabh MishraNo ratings yet

- Capital Budgeting and Working Capital DecisionsDocument24 pagesCapital Budgeting and Working Capital DecisionsVeeramani YellapuNo ratings yet

- Capital Budgeting and Working Capital AnalysisDocument36 pagesCapital Budgeting and Working Capital Analysis19-R-0503 ManogjnaNo ratings yet

- MALINAB AIRA BSBA FM 2-2 ACTIVITY 6 Overview of WCMDocument5 pagesMALINAB AIRA BSBA FM 2-2 ACTIVITY 6 Overview of WCMAira MalinabNo ratings yet

- Unit V MefaDocument24 pagesUnit V Mefashaikkhaderbasha2002No ratings yet

- Mefa Unit5Document47 pagesMefa Unit5SurajNo ratings yet

- Mefa R19 - Unit-5Document26 pagesMefa R19 - Unit-5KaarletNo ratings yet

- Dimensions of Working Capital ManagementDocument22 pagesDimensions of Working Capital ManagementRamana Rao V GuthikondaNo ratings yet

- Fibre To BTSDocument7 pagesFibre To BTSPravesh Kumar Thakur100% (2)

- A Key Issue in Public Policy MakingDocument2 pagesA Key Issue in Public Policy MakingRamana Rao V GuthikondaNo ratings yet

- A Key Issue in Public Policy MakingDocument2 pagesA Key Issue in Public Policy MakingRamana Rao V GuthikondaNo ratings yet

- Pocket ViewDocument7 pagesPocket ViewWaqar AhmedNo ratings yet

- Cellular Concepts A WriteupDocument9 pagesCellular Concepts A WriteupRamana Rao V GuthikondaNo ratings yet

- Longitudinal Standing Waves in An Air ColumnDocument3 pagesLongitudinal Standing Waves in An Air ColumnRamana Rao V GuthikondaNo ratings yet

- New Licenses in Banking SectorDocument13 pagesNew Licenses in Banking SectorRamana Rao V GuthikondaNo ratings yet

- Names of foodstuffs in Indian languagesDocument19 pagesNames of foodstuffs in Indian languagesSubramanyam GundaNo ratings yet

- Term Paper On USO Scheme by G V R Rao, V Surendran, PGPPMDocument33 pagesTerm Paper On USO Scheme by G V R Rao, V Surendran, PGPPMRamana Rao V GuthikondaNo ratings yet

- Archimedis PrincipleDocument2 pagesArchimedis PrincipleRamana Rao V Guthikonda100% (1)

- 02 Fundamentals of OFDMDocument33 pages02 Fundamentals of OFDMDiego CamargoNo ratings yet

- Longitudinal Standing Waves in An Air ColumnDocument3 pagesLongitudinal Standing Waves in An Air ColumnRamana Rao V GuthikondaNo ratings yet

- Comments On Ratio AnalysisDocument1 pageComments On Ratio AnalysisRamana Rao V GuthikondaNo ratings yet

- Social Marketing Case StudyDocument5 pagesSocial Marketing Case StudyRamana Rao V GuthikondaNo ratings yet

- An Approach To Planned Social ChangeDocument10 pagesAn Approach To Planned Social ChangeAkochayé Israël KouteyNo ratings yet

- Ofdm PaperDocument58 pagesOfdm Paperdarkprince117No ratings yet

- Ofdm Mimo4mm EditionDocument48 pagesOfdm Mimo4mm EditionRamana Rao V GuthikondaNo ratings yet

- Rohde-Schwarz DTF981027 05Document57 pagesRohde-Schwarz DTF981027 05xjackiechanNo ratings yet

- BICNDocument12 pagesBICNRamana Rao V GuthikondaNo ratings yet

- GSMDocument36 pagesGSMkanav07No ratings yet

- NGN OverviewDocument30 pagesNGN OverviewRamana Rao V GuthikondaNo ratings yet

- How OFDM WorksDocument22 pagesHow OFDM Workssaske969No ratings yet

- Understanding OFDM by IITGDocument7 pagesUnderstanding OFDM by IITGRamana Rao V GuthikondaNo ratings yet

- M 2 M Communication: Worldwide Future Prospects and Potential Impact Analysis in IndiaDocument15 pagesM 2 M Communication: Worldwide Future Prospects and Potential Impact Analysis in IndiaRamana Rao V GuthikondaNo ratings yet

- Faint Transmissions PDFDocument8 pagesFaint Transmissions PDFMi24_HindNo ratings yet

- The foundations of chemistry: classifying matter by state and compositionDocument121 pagesThe foundations of chemistry: classifying matter by state and compositionRamana Rao V GuthikondaNo ratings yet

- hc12 MannualDocument440 pageshc12 Mannualcopyright.caNo ratings yet

- Iscal EARDocument311 pagesIscal EARDjalma MoreiraNo ratings yet

- Unit 3 - Foreign Exchange TradingDocument3 pagesUnit 3 - Foreign Exchange TradingPhan Thị Minh ThúyNo ratings yet

- Acctg Lab 7Document8 pagesAcctg Lab 7AngieNo ratings yet

- Vipul's Investment Management Portfolio Analysis GuideDocument10 pagesVipul's Investment Management Portfolio Analysis GuideAnjali AnanthakrishnanNo ratings yet

- Corporate Finance DecisionsDocument3 pagesCorporate Finance DecisionsPua Suan Jin RobinNo ratings yet

- Working Report 2022 30 June English Single Page Artwork Low ResDocument36 pagesWorking Report 2022 30 June English Single Page Artwork Low ResAparajita RB SinghNo ratings yet

- Practice Problems - Audit of InvestmentsDocument10 pagesPractice Problems - Audit of InvestmentsAnthoni BacaniNo ratings yet

- 10, Intengan Vs CADocument2 pages10, Intengan Vs CABOEN YATORNo ratings yet

- Bill Discounting Factoring & ForfaitingDocument34 pagesBill Discounting Factoring & Forfaitingdilpreet92No ratings yet

- Corporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFDocument35 pagesCorporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFvernon.amundson153100% (10)

- HBZ Bank business account termsDocument11 pagesHBZ Bank business account termsXolani Radebe RadebeNo ratings yet

- G 10 Acc Homework 2Document4 pagesG 10 Acc Homework 2Sayed AbbasNo ratings yet

- Cambridge Assessment International Education: Accounting 0452/22 October/November 2017Document12 pagesCambridge Assessment International Education: Accounting 0452/22 October/November 2017pyaaraasingh716No ratings yet

- What Is Account PayableDocument5 pagesWhat Is Account PayablebhityNo ratings yet

- USAA HackingDocument6 pagesUSAA Hackingayina100% (1)

- Set A Merchandising Vat QuizDocument6 pagesSet A Merchandising Vat QuizJan Allyson BiagNo ratings yet

- NidhiDocument41 pagesNidhiAjeet KumarNo ratings yet

- 02 Financial Statements Case StudyDocument3 pages02 Financial Statements Case StudyanitalauymNo ratings yet

- Update Customer Account DetailsDocument1 pageUpdate Customer Account DetailsvipinNo ratings yet

- 04 ReceivablesDocument12 pages04 ReceivablesNina100% (1)

- RBS Holdings N.V. Annual Report and Accounts 2011Document256 pagesRBS Holdings N.V. Annual Report and Accounts 2011Iskandar IsNo ratings yet

- Background of The Study:: Financial Analysis of Himalayan Bank LimitedDocument31 pagesBackground of The Study:: Financial Analysis of Himalayan Bank Limitedram binod yadavNo ratings yet

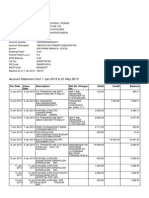

- Account StatementDocument6 pagesAccount StatementDeepaBabukumarNo ratings yet

- SCF WorksheetDocument19 pagesSCF WorksheetAngelo Gian CoNo ratings yet

- Final Report On BankingDocument70 pagesFinal Report On Bankingbharat sachdevaNo ratings yet

- Sip PPT 2018Document16 pagesSip PPT 2018Rajat GuptaNo ratings yet

- Uts Manajemen Keuangan StrategikDocument8 pagesUts Manajemen Keuangan StrategikRahman IqbalNo ratings yet

- Financial Management Core Concepts 4th Edition Brooks Test BankDocument35 pagesFinancial Management Core Concepts 4th Edition Brooks Test Banktrancuongvaxx8r100% (21)

- Central Banks: Understanding the Key Players in Financial MarketsDocument69 pagesCentral Banks: Understanding the Key Players in Financial MarketsSebastian PaglinoNo ratings yet

- Fin430 - Dec2019Document6 pagesFin430 - Dec2019nurinsabyhahNo ratings yet