You might also like

- AmeriGas invoice details customer's propane purchaseDocument2 pagesAmeriGas invoice details customer's propane purchaseVictor Sosa0% (1)

- AGWA Guide FixingDocument49 pagesAGWA Guide FixingdavoefirthNo ratings yet

- Activate Your BPI Credit CardDocument3 pagesActivate Your BPI Credit CardAl Patrick Dela CalzadaNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Frequently Asked Questions in International Standards on AuditingFrom EverandFrequently Asked Questions in International Standards on AuditingRating: 1 out of 5 stars1/5 (1)

- Chapter 10 Lessons From Market History: Corporate Finance, 12e (Ross)Document35 pagesChapter 10 Lessons From Market History: Corporate Finance, 12e (Ross)EnciciNo ratings yet

- Quiz Cash FlowDocument3 pagesQuiz Cash FlowMumbo Jumbo100% (1)

- Cost Accounting Past PapersDocument66 pagesCost Accounting Past Paperssalamankhana100% (2)

- Quiz Semester - 5 (Professional Etiquettes and Group Discussion) Name: Enrollment No.Document3 pagesQuiz Semester - 5 (Professional Etiquettes and Group Discussion) Name: Enrollment No.paridhiNo ratings yet

- Agreement Between Author and PublisherDocument4 pagesAgreement Between Author and PublisherMUNEEB AKBARNo ratings yet

- 2015 11 SP Accountancy Solved 04 PDFDocument4 pages2015 11 SP Accountancy Solved 04 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Unsolved 05 PDFDocument4 pages2015 11 SP Accountancy Unsolved 05 PDFcerlaNo ratings yet

- Sample Paper on Accountancy Class XIDocument20 pagesSample Paper on Accountancy Class XIGurjit BrarNo ratings yet

- Ryan International School Unit Test - I Class-Xi Sub.: Accounts (Paper-2) Time: 1 Hrs. MM: 32Document2 pagesRyan International School Unit Test - I Class-Xi Sub.: Accounts (Paper-2) Time: 1 Hrs. MM: 32RGN 11E 20 KHUSHI NAGARNo ratings yet

- Part - A (: Time Allowed: 3 Hours Maximum Marks: 90Document4 pagesPart - A (: Time Allowed: 3 Hours Maximum Marks: 90NameNo ratings yet

- SAMPLE PAPER - (Solved) : For Examination March 2018 Accountancy Class - XIDocument14 pagesSAMPLE PAPER - (Solved) : For Examination March 2018 Accountancy Class - XISaksham AroraNo ratings yet

- ACCOUNTANCY XI SAMPLE PAPERDocument13 pagesACCOUNTANCY XI SAMPLE PAPERpriyaNo ratings yet

- SAMPLE PAPER - (Solved) : For Examination March 2017Document13 pagesSAMPLE PAPER - (Solved) : For Examination March 2017ankush yadavNo ratings yet

- Sample PaperDocument28 pagesSample PaperSantanu KararNo ratings yet

- NCERT Solutions for Class 11 AccountancyDocument4 pagesNCERT Solutions for Class 11 AccountancyAnonymous VaYaLmoX4No ratings yet

- Must DoDocument27 pagesMust DoKuldeep SharmaNo ratings yet

- Questions Bank Accounts ClassDocument5 pagesQuestions Bank Accounts ClassRidhesh SharmaNo ratings yet

- 438Document6 pages438Rehan AshrafNo ratings yet

- Class 11 Accountancy Worksheet - 2023-24Document17 pagesClass 11 Accountancy Worksheet - 2023-24Yashi BhawsarNo ratings yet

- Institute of Actuaries of India: ExaminationsDocument8 pagesInstitute of Actuaries of India: ExaminationsRushikesh AravkarNo ratings yet

- 22ODBBT103Document5 pages22ODBBT103Pallavi JaggiNo ratings yet

- Part - A (: Time Allowed: 3 Hours Maximum Marks: 90Document4 pagesPart - A (: Time Allowed: 3 Hours Maximum Marks: 90NameNo ratings yet

- 11 Accountancy SP 2Document17 pages11 Accountancy SP 2Vikas Chandra BalodhiNo ratings yet

- Accounting Final Sendup 2013Document3 pagesAccounting Final Sendup 2013Mozam MushtaqNo ratings yet

- CBSE Class 12 Accountancy Sample Paper With Marking Scheme 2013Document5 pagesCBSE Class 12 Accountancy Sample Paper With Marking Scheme 2013Manish SahuNo ratings yet

- Module-2 Sample Question PaperDocument18 pagesModule-2 Sample Question PaperRay Ch100% (1)

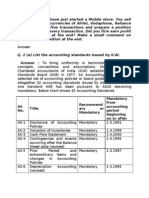

- Recommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterDocument7 pagesRecommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterdnbiswasNo ratings yet

- 11 Accountancy SP 1 PDFDocument17 pages11 Accountancy SP 1 PDFSumit MazumderNo ratings yet

- Accountancy Extra PointsDocument14 pagesAccountancy Extra PointsRishav KuriNo ratings yet

- Segment Sales Net Profit: Sample Questions For Written Test in ProjectsDocument3 pagesSegment Sales Net Profit: Sample Questions For Written Test in ProjectsvasantNo ratings yet

- If, Cost of Machine Rs.400, 000 Useful Life 5 Years Rate of Depreciation 40%Document13 pagesIf, Cost of Machine Rs.400, 000 Useful Life 5 Years Rate of Depreciation 40%Narang NewsNo ratings yet

- Class Xi SP 1Document17 pagesClass Xi SP 1Priya NasaNo ratings yet

- 11th Accounts Mock Paper-1Document2 pages11th Accounts Mock Paper-1Aliasgar ZaverNo ratings yet

- Intermediate Exam Question Compilation for ICWAI Syllabus 2002Document30 pagesIntermediate Exam Question Compilation for ICWAI Syllabus 2002Reshma RajNo ratings yet

- CBSE Class 11 Accountancy Worksheet - Question Bank (1)Document17 pagesCBSE Class 11 Accountancy Worksheet - Question Bank (1)Umesh JaiswalNo ratings yet

- Concepts and Accounting Equations Test - 02Document2 pagesConcepts and Accounting Equations Test - 02Khushi GuptaNo ratings yet

- CA IPCC Accounts Mock Test Series 1 - Sept 2015Document8 pagesCA IPCC Accounts Mock Test Series 1 - Sept 2015Ramesh Gupta100% (1)

- शिक्षा निदेिालय राष्ट्रीय राजधािी क्षेत्र ददल्ली Directorate of Education, GNCT of DelhiDocument4 pagesशिक्षा निदेिालय राष्ट्रीय राजधािी क्षेत्र ददल्ली Directorate of Education, GNCT of DelhiAshish ChNo ratings yet

- XII AccountancyDocument4 pagesXII AccountancyAahna AcharyaNo ratings yet

- Test (Single Entry System)Document3 pagesTest (Single Entry System)SarthakNo ratings yet

- 4 MarksDocument4 pages4 MarksEswari GkNo ratings yet

- NCERT solutions, CBSE sample papers, notes for classes 6 to 12Document4 pagesNCERT solutions, CBSE sample papers, notes for classes 6 to 12NameNo ratings yet

- 2015 Accountancy Question PaperDocument4 pages2015 Accountancy Question PaperJoginder SinghNo ratings yet

- KTTC1Document22 pagesKTTC1Trần Khánh VyNo ratings yet

- Accounting For Managers MB003 QuestionDocument34 pagesAccounting For Managers MB003 QuestionAiDLo0% (1)

- 123doc Questions and Answers For Financial Accounting 1 3Document16 pages123doc Questions and Answers For Financial Accounting 1 3Mỹ AnhNo ratings yet

- CBSE Class 11 Accountancy Sample Paper 1 QuestionsDocument6 pagesCBSE Class 11 Accountancy Sample Paper 1 Questionsrenu bhattNo ratings yet

- Acconts Preliminary Paper 2Document13 pagesAcconts Preliminary Paper 2AMIN BUHARI ABDUL KHADERNo ratings yet

- Mock TestDocument8 pagesMock TestDiksha DudejaNo ratings yet

- F AccountDocument39 pagesF AccountChandra Prakash SoniNo ratings yet

- Q.1 Assure You Have Just Started A Mobile Store. You Sell MobileDocument16 pagesQ.1 Assure You Have Just Started A Mobile Store. You Sell MobileUttam SinghNo ratings yet

- Father Agnel School, New Delhi PERIODIC TEST-I (2021-22) SUBJECT: Accountancy Class: Xii TIME: 1hr. 30min Max Marks: 40Document4 pagesFather Agnel School, New Delhi PERIODIC TEST-I (2021-22) SUBJECT: Accountancy Class: Xii TIME: 1hr. 30min Max Marks: 40fffffNo ratings yet

- Accountancy March 2008 EngDocument8 pagesAccountancy March 2008 EngPrasad C M100% (2)

- IPCC MTP2 AccountingDocument7 pagesIPCC MTP2 AccountingBalaji SiddhuNo ratings yet

- CBSE Sample Paper Class Xi Accountancy 2006 03Document6 pagesCBSE Sample Paper Class Xi Accountancy 2006 03Amrita Mary JacobNo ratings yet

- Questions Accounting For Departments: Revision Test Paper Cap-Ii: Advanced AccountingDocument27 pagesQuestions Accounting For Departments: Revision Test Paper Cap-Ii: Advanced AccountingcasarokarNo ratings yet

- 2016 12 SP Accountancy Solved 01Document8 pages2016 12 SP Accountancy Solved 01Sto BreakerNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- 2015 11 SP Accountancy Unsolved 01 PDFDocument4 pages2015 11 SP Accountancy Unsolved 01 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Unsolved 02 PDFDocument4 pages2015 11 SP Accountancy Unsolved 02 PDFcerlaNo ratings yet

- Solution: SAMPLE PAPER-5 (Solved) Accountancy Class - XIDocument6 pagesSolution: SAMPLE PAPER-5 (Solved) Accountancy Class - XIcerlaNo ratings yet

- Latest o Is D StandardsDocument1 pageLatest o Is D StandardsSushil MeshramNo ratings yet

- 2015 11 SP Accountancy Solved 02Document4 pages2015 11 SP Accountancy Solved 02Siddharth Jain0% (1)

- 2015 11 SP Accountancy Solved 03 Sol 9hg3 PDFDocument6 pages2015 11 SP Accountancy Solved 03 Sol 9hg3 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 01 Sol IcewDocument6 pages2015 11 SP Accountancy Solved 01 Sol IcewcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 05 PDFDocument4 pages2015 11 SP Accountancy Solved 05 PDFcerla0% (1)

- 2015 11 SP Accountancy Solved 02 Sol 89nd PDFDocument7 pages2015 11 SP Accountancy Solved 02 Sol 89nd PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 03 PDFDocument4 pages2015 11 SP Accountancy Solved 03 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 01Document4 pages2015 11 SP Accountancy Solved 01Siddharth JainNo ratings yet

- Cbse Class 11 Mathematics Sample Paper Sa1 2014 2 PDFDocument2 pagesCbse Class 11 Mathematics Sample Paper Sa1 2014 2 PDFcerlaNo ratings yet

- Cbse Class 11 Mathematics Sample Paper Sa1 2014 3 PDFDocument3 pagesCbse Class 11 Mathematics Sample Paper Sa1 2014 3 PDFcerlaNo ratings yet

- Cbse Class 11 Mathematics Sample Paper Sa1 2014 1 PDFDocument3 pagesCbse Class 11 Mathematics Sample Paper Sa1 2014 1 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 03 Sol 9hg3 PDFDocument6 pages2015 11 SP Accountancy Solved 03 Sol 9hg3 PDFcerlaNo ratings yet

- Blue Print: Accounting: Class XI Weightage Difficulty Level of QuestionsDocument12 pagesBlue Print: Accounting: Class XI Weightage Difficulty Level of Questionssirsa11No ratings yet

- 2015 11 SP Accountancy Unsolved 02 PDFDocument4 pages2015 11 SP Accountancy Unsolved 02 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Unsolved 04 PDFDocument4 pages2015 11 SP Accountancy Unsolved 04 PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 03 PDFDocument4 pages2015 11 SP Accountancy Solved 03 PDFcerlaNo ratings yet

- Sample Paper XI Accountancy ClassDocument4 pagesSample Paper XI Accountancy ClasscerlaNo ratings yet

- Solution: SAMPLE PAPER-5 (Solved) Accountancy Class - XIDocument6 pagesSolution: SAMPLE PAPER-5 (Solved) Accountancy Class - XIcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 05 PDFDocument4 pages2015 11 SP Accountancy Solved 05 PDFcerla0% (1)

- 2015 11 SP Accountancy Solved 02 Sol 89nd PDFDocument7 pages2015 11 SP Accountancy Solved 02 Sol 89nd PDFcerlaNo ratings yet

- 2015 11 SP Accountancy Solved 02Document4 pages2015 11 SP Accountancy Solved 02Siddharth Jain0% (1)

- Chapter Ii: Management and OrganizationDocument6 pagesChapter Ii: Management and OrganizationBrenNan ChannelNo ratings yet

- The Champion Legal Ads: 07-15-21Document36 pagesThe Champion Legal Ads: 07-15-21Donna S. SeayNo ratings yet

- PDN Trail Branding GuidelinesDocument11 pagesPDN Trail Branding GuidelinesALEC MondelloNo ratings yet

- Exceptional Service Grading Company: A Case Study On Employing Financial Ratio Analysis As A Basis For Business ExpansionDocument5 pagesExceptional Service Grading Company: A Case Study On Employing Financial Ratio Analysis As A Basis For Business ExpansionRyan S. AngelesNo ratings yet

- Public Finance & Taxation - Chapter 4, PT IVDocument24 pagesPublic Finance & Taxation - Chapter 4, PT IVbekelesolomon828No ratings yet

- Wellesley CollegeDocument11 pagesWellesley CollegeAyam KontloNo ratings yet

- The Exxon-Mobil Merger: An Archetype: J. Fred WestonDocument20 pagesThe Exxon-Mobil Merger: An Archetype: J. Fred WestonTRANNo ratings yet

- 3901 LN1Document3 pages3901 LN1Ayushmaan BhattacharjiNo ratings yet

- CEAT Limited Integrated Annual Report FY23 PG 85 85Document177 pagesCEAT Limited Integrated Annual Report FY23 PG 85 85sumitminocha00No ratings yet

- Test Plan For Online Test GeneratorDocument9 pagesTest Plan For Online Test GeneratorLucasNo ratings yet

- Fact Finding - UT TakafulDocument1 pageFact Finding - UT TakafulcaptkhairulnizamNo ratings yet

- Gateway Case Study Write UpDocument2 pagesGateway Case Study Write UpSamantha VasquezNo ratings yet

- Intercultural Communication PowerpointDocument34 pagesIntercultural Communication PowerpointRenee.KitsonNo ratings yet

- Chapter 6 - Introduction To The Value Added TaxDocument8 pagesChapter 6 - Introduction To The Value Added TaxJamaica DavidNo ratings yet

- Entrepreneurship Chapter 4 QuizDocument2 pagesEntrepreneurship Chapter 4 QuizBrian DuelaNo ratings yet

- Org Chart Updated 2021Document1 pageOrg Chart Updated 2021Shan Dela VegaNo ratings yet

- Credit Risk Management and Best PracticesDocument23 pagesCredit Risk Management and Best Practicessagar7No ratings yet

- Corporate & Business LawDocument8 pagesCorporate & Business LawRuchika ChonaNo ratings yet

- Mathematics: Quarter 2 - Modyul 2: Pagpanan-Aw Ag Paghambae It Basic Multiplication FactsDocument16 pagesMathematics: Quarter 2 - Modyul 2: Pagpanan-Aw Ag Paghambae It Basic Multiplication FactsEdlyn Aranas RegnoNo ratings yet

- An Application of Building Blocks of Competitive Advantage' Approach To The U.S. Cereal Market LeadersDocument17 pagesAn Application of Building Blocks of Competitive Advantage' Approach To The U.S. Cereal Market LeadersGemNo ratings yet

- CFP Young Scholar Conference 2019Document2 pagesCFP Young Scholar Conference 2019Tanmoy dasNo ratings yet

- Round Tripping - Indian Dilemma and International PerspectiveDocument8 pagesRound Tripping - Indian Dilemma and International PerspectiveINSTITUTE OF LEGAL EDUCATIONNo ratings yet

- Bajaj Finserv Limited's focus on lending, asset management, and insuranceDocument23 pagesBajaj Finserv Limited's focus on lending, asset management, and insuranceAthira K. ANo ratings yet

- 43-Interview-Tips-Asset ManagementDocument2 pages43-Interview-Tips-Asset ManagementAdnan NaboulsyNo ratings yet