Professional Documents

Culture Documents

Internship Report

Uploaded by

Bishnu DhamalaCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Internship Report

Uploaded by

Bishnu DhamalaCopyright:

Available Formats

1

Chapter One

Introduction

1.1 Background

1.1 Introduction of Insurance

Insurance is a means to get financial security against risk. It is a contract or a policy

whereby, for a premium one party promises to compensate to the other party for loss on a

specified subject by specified peril or risk. It is a service industry it provides valuable

protection to individual industry, commerce and trade against uncertain financial losses.

Insurance is a valid contract between two parties where offer and acceptance are the essential

ingredients. Until and unless the offer by offerer is not accepted by offeree it cannot be called

as contract. Basically insurance is a way of reducing uncertainties and risk.

The word Risk is a catchword pounce by the people from every nook and corner of

the world. Generally risk refers to the exposure of peril, possibility of suffering loss or injury,

chances of meeting dangerous situation. Human life and material possessions are continually

exposed to loss or damage by numerous destructive forces, which create great uncertainty in

life, in commerce, in industry etc. It is an undisputed fact that the risk is undeniable in the

modern complex life and society. More specifically risk denotes the uncertainty of loss.

Uncertainty refers to the unknown future outcome or result of an event. Risk is a blessing

because it gives rise to discussion, hope, planning accomplishment and progress. It is a curse

in so far as it gives rise to dispute, fear, defensive tactics, failure and retrogression. The

uncertainty about future is basic universal fact of human life or earth.

No human activity is free from risk. Moreover, sophisticated scientific innovations,

scalating violence and terrorism have made risk a glaring critical issue. In this context the

idea of risk management and the idea of the insurance have emerged. Insurance plays a

significant role in risk management. Insurance is devised as a financial security against risk.

The wheel of development is accelerated by industrialization and industrialization is possible

only with the support of two big institutions - banking and insurance. The one pillar, banking

provides capital and helps in the financial transaction of business in many ways. Another,

pillar insurance offers a high economic relief to different types of industrialist, businessmen

and individuals. Insurance has become the pillar of alertness, courage and eagerness to

develop the life and living standard of common people, industrialist and traders of todays

world. Insurance has been introduced to safeguard the interest of people from uncertainty by

providing certainty of payment at a given contingency. Insurance companys are integrated

part of the same business. These two are the two wheels of a cart. In the absence of one, the

other cannot function. Insurance is equally important for common people and businessmen. It

is part and parcel of the business houses.

The insurance market in global perspective has been an important ingredient for

economic development. In a every countries, Insurance companies have played a very

significant intermediaries role in mobilizing funds through the combination of investment

portfolio. However, in developing countries like Nepal, the role of insurance companies is

still to be realized as an important vehicle of mobilizing the internal saving through various

insurance schemes of life and non-life sectors in the economy. This can be done with proper

and optimal combination of risks as an organized method of dealing with pure risks to which

individual, family, firm or other organizations are exposed. Insurance is a social device,

which combines the risk of individuals into a group, using funds contributed by members of

the group to pay for losses.

Insurance has wide scope and areas nowadays. Insurance can be defined form the

viewpoint of several disciplines. The definition of insurance can be expressed from the

viewpoint of law, economic, history, sociology. Insurance is a non-profit oriented service that

shares risk of the society. According to G.H Magee, "Insurance has been defined as a plan by

which large number of people are associated themselves and transfer to shoulder of all, risk to

attach individuals. The main objective of insurance is to minimize the boarder of risk by

collecting form many people in the society and paying to few over the entire group. Insurance

works as a co-operative device to spread the loss caused by a particular risk over a number of

persons who are exposed to it and who agree to ensure themselves against that risk. Insurance

gives relief from the risk. It performs the task of paying compensation for financial loss under

the insurance, in return of little fixed amount if loss or damage has taken place. That is why

A.H Mowbary and R.H Blanchard defined insurance in this way, "Insurance is a promise by

an insurer to an insured protection or service"

Insurance companies are capable of providing industrial finance, government finance

or even personal finance. They provide different finance through their own investment policy

and pattern based upon their own corporate objective and nature of the line of insurance

business. In the context of Nepalese insurance companies they provide various insurance

policies and charge premium under insured risk and nature. Insurance companies collect fund

through various client (people and organization) as premium. Therefore, all the insurance

companies are responsible for their clients interest. This study looks and analyses insurance

companys premium collection and investment situation. Everyone pays a premium those

who suffer a loss are paid a sum of equivalent to loss (loss according to the term of contract)

and those who dont suffer loss by the premium paid. The protection against unforeseen

events is purchased through a contract of insurance.

From the above mentioned definitions it is clear that the insurance reduces the risk

and provides financial security in return of payment of a certain amount. Hence, we can say

that Insurance is a powerful weapon to manage risk.

According to D.S Hansell "Insurance may be defined as social device providing

compensation for the effects of misfortune, the payment being made from accumulated

contribution of all parties participating in the scheme"

Insurance is an agreement by which a company or the state undertakes to provide a

guarantee of compensation for specified loss, damage, illness or death in return for a

premium of a certain premium. In other words an insurance is a policy (contract) in which an

individual or entity receives financial protection or reimbursement against loss from an

insurance company. The company pools certain risk to make payments more affordable for

the insured. As Edwin and Peterson "Insurance is a contract by which one party for a

compensation called premium assumes particular risk of the other party or promise to pay

him or his nominee a certain sum of money on a specified contingency".

1.2 History of Insurance

The term of insurance developed through the faith and co-operation. The origin of

insurance is lost in antiquity. Evidence is on record that arrangements embodying the idea of

insurance were made in Bobylonia and India at quite an early period. In Rig-Veda, the most

sacred book of Hindus, reference were made in the concept yogkshema more or less akin to

the well being and security of the people. The codes of Hummurabi and of Manu had

recognized the advisability of provision for sharing the future losses.

The earliest traces of insurance in the ancient world are found in the form of marine

trade loans or carriers contract, which included an element of insurance. Evidence shows that

the marine insurance is the oldest from of insurance. Travelers by sea and land were very

much exposed to the risk of losing their vessels and merchandise because the piracies on the

open seas and highway robbery of caravans were very common. Besides, there were several

risks. The risk to owners of such ships was enormous and, therefore, to safeguard them,

which could not be conveniently borne by the unfortunate individual victim. The co-operative

devices were quite voluntary in the beginning, but the insurance development was not

confined to the Lombards and to the Hansa merchants, it spread throughout Spain, Portugal,

France, Holland and England.

After marine insurance, fire insurance developed in its present form. It originated in

Germany in beginning of the sixteen- century. It got momentum in England after the great

fire in 1966 when the fire losses were tremendous. Gradually all the types of insurance were

developed at this form.

1.2.1 Insurance in Context of Nepal

In our country, the concept of insurance can be traced down to the Guthi Systems

and joint family culture that has been prevalent since the ancient times. These systems have

provided security and assistance to individuals and families in time of need. With the change

in the economic and social perspectives and the increasing complexities of the up-coming

small-scale industries, an immense need for a domestic insurance company was felt to insure

against any loss that could arise due to mishaps in industries.

With the development of trade, commerce and industry, the necessity of insurance in

our country was felt long ago. But there was no evidence of any organized form of insurance

in Nepal until 1947. Society was organized in an agricultural basis and the socio-economic

organization took care of any problem or calamity confronted to the community.

Before the emergence of insurance company in Nepal, there were several broker

offices of Indian company operating in Nepal. The first insurance company in Nepal was

Nepal Malchalani Tatha Beema Company Ltd, which was established in 1947 A.D. as a

subsidiary Company of Nepal Bank Limited, the first commercial Bank of Nepal. The main

objective of that company was to transport the goods imported by the bank and to keep the

goods in its custody. The company took responsibility of cash transaction of the bank. After

sometimes, the company changed its name from Nepal Malchalani Tatha Bema Company Ltd

to Nepal Insurance and Transport Company Ltd.

Transporting goods and issuing insurance policies were the core objectives of Nepal

Insurance and Transport Company Ltd. but it mainly concentrated only on insurance sector.

So again, it changed its name and became Nepal Insurance Company Limited. Even though

Nepal Insurance Company Limited was established to sell insurance, it was reluctant to

accept other business except Nepal Bank Ltd. Since foreign (Indian) insurance Companies

were still transacting insurance business through their broker offices in Kathmandu and other

branches in major cities in Nepal before and after establishment of Nepal Insurance Company

Limited.

After the restoration of Democracy in 1990 A.D., Insurance environment began to

change simultaneously along with other factors. Thus to meet the requirement of the

changing situation Insurance Act 1968 was repelled by new Insurance Act 1992 (Beema Ain

2049 B S). The preamble of the act clearly states the purpose of the act. An insurance Board

was established to Systematize, regularize and develop the insurance business. To achieve the

goal as stated in the preamble, Beema Samiti (Insurance Board) was formed as an

autonomous body under the Insurance Act of 1992 A.D under the direct supervision of the

government. After the introduction of Insurance Act, 1992, the number of private insurance

companies came into existence. There are altogether 25 Insurance companies functioning in

Nepal both in life and non life insurance business in Nepal.

Amount and the first time life insurance institution insured amount technology on the basis of

data.

In 1744 A.D. passing the life insurance Act created the foundation of the modern

insurance. Thereafter different laws later removed the defects that came to the business.

Many companies were closed and some of them went and mixing or merging with another

insurance company. There is no controversy that the Life Insurance Act 1870 was passed to

control the operation of the life insurance business for protection of the customers. Before the

beginning of the 19 century many life insurance were that already established in the world.

We find that the life insurance business in our neighboring country India had started within

the establishment of the Mutual Association. In 1971, both life and the non life insurance

were nationalized in India; as a result, the Life Insurance Corporation for life and general

insurance company ltd for non life insurance were established. During the region of Elizabeth

1 the life insurance used to effect for only one year. After one year, it was not renewed, the

insurance automatically used to be cancelled. But the job of effecting long term insurance,

started from 18 century has been increased continuously.

1.3 Principle of Insurance

The main objective of every insurance contract is to give financial security and

protection to the insured from any future uncertainties. Insured must never ever try to misuse

this safe financial cover. Seeking profit opportunities by reporting false occurrences violates

the terms and conditions of and insurance contract. This breaks trust and result in breaching

of a contract and An insurer must always investigate any doubtable insurance claims. It is

also a duty of the insurer to accept and approve the genuine insurance claims made, as early

as possible without any further delay.

1.3.1Principle of Utmost Good Faith.

Principle of utmost good faith is a very basic and first primary principle of insurance.

According to this principle the insurance contract must be signed by both parties (i.e insurer

and insured) in an absolute good faith or belief and trust.

The person getting insured must willingly disclose and surrender to the insurer his

complete true information regarding the subject matter of insurance. The insurer's liability

gets void (i.e revoked or cancelled) if any fact about the subject matter of the insurance are

either omitted, hidden, falsified or presented in a wrong manner by the insured. The principle

of utmost good faith applies to all types of insurance contract.

1.3.2 Principle of Insurable Interest

The principle of insurable interest states that the person getting insured must have

insurable interest in the object of insurance. A person has an insurable interest when the

physical existence of the insured object gives him some gain but its non-existence will give

him a loss. In simple word, the insured person must suffer some financial by the damage of

the insured object.

For example:- the owner of a taxicab has insurable interest in the taxicab because he

is getting income from it. But if he sells it, he will not have an insurable interest left in that

taxicab. From the above example, we cannot conclude that, ownership plays a very crucial

role in evaluating insurable interest. Every person has insurable interest in his own life. A

merchant has insurable interest in his business of trading. Similarly a creditor has insurable

interest in his debtors.

1.3.3 Principle of Indemnity

Indemnity means a guarantee or assurance to put the insured in the same position in

which he was immediately prior to the happening of the uncertain event. It is applicable to

fire, marine and other general insurance.

Indemnity means security, protection and compensation given against damage, loss or

injury. According to the principle of indemnity, an insurance contract is signed only for

getting protected against unpredicted financial loss arising due to future uncertainties. Since,

insurance contract is not made for making profit, and its sole propose is to give compensation

in case of loss or damage. So in an insurance contract, the amount of compensation paid is in

proportion to the incurred losses. The amount of compensation is limited to the amount

assured or the actual loss, whichever is less. The compensation must not be more or less than

the actual loss/damage. As per the contract of indemnity the compensation is not paid if the

specified loss does not happen due to a particular reason during a specified period time. Thus

insurance is only for giving protection against losses and not for making profit.

However in case of life insurance, the principle of indemnity does not apply because

the value of human life cannot be measured in terms of money. So the principle of indemnity

is applicable to fire, marine and other general insurance. Principle of indemnity can be further

divided into two sub divisions.

a) Principle of Contribution

b) Principle of Subrogation

Principal of contribution is a corollary of the principle of indemnity. It applies to all

contract of indemnity, if the insured has taken out more than one policy on the subject matter.

According to the principle the insured can claim compensation only to the extent of actual

10

loss either from all insurers or from any one insurer. If one insurer pays full compensation

then that insurer can claim proportionate claim from other insurers. Similarly if the insured

claim full amounts of compensation form one insurer then he/she cannot claim for same

compensation from other insurer and make profit.

Principle of subrogation is an extension and another corollary of the principle of

indemnity. It also applies to all principle of indemnity. According to principle of subrogation

when the insured is compensated for the loss due to damage to his/her insured property, then

the ownership right of such property shift to the insurer. But the principle is valued only if the

damage property has any value after the event causing the damage. The insurer can benefit

out of subrogation rights only to the extent of the amount he has paid to the insured as

compensation.

1.3.4 Principle of Loss Minimization

According to the principle of loss minimization, insured must always try his/her level

best to minimize the loss of his insured property, in case of uncertain events like fire

breakdown, or blast. The insured must take all possible measures and necessary steps to

control and reduce the losses in such a scenario. The insured must not neglect and behave

irresponsibly during such events just because the property is insured. Hence it is the

responsibility of the insured to protect his insured property and avoid further losses.

For example:- If a house set on fire due to an electric short circuit. In this tragic

scenario, the insured must try his level best to stop by fire by all possible means like first

calling nearest fire department office, asking neighbors for emergency fire extinguisher, he

must not remain inactivate and watch his house burning, hoping that his house is insured.

11

1.3.5 Principle of Causa Proxima (Nearest Cause)

The loss of insured property can be caused by more than one cause in succession to be

another. The property may be insured against some cause and sometimes the damage may be

due to another cause which is not covered by the policy. So before compensation of any of

the damage or loss the proximate cause or the nearest cause must be found out. If the

proximate cause is the one which is insured against, the insurance company is bound to pay

the compensation but if the real cause of the damage of the insured property is due to any

other rather than the insured peril then the insurance company is not bound to pay any

compensation for the loss or damage of the property insured.

The Principle of causa proxima is also called principle of proximate cause, the principle

state that to find out whether the insurer is liable for the loss or not, the proximate (closest)

and not the remote (farest) must be looked into. For example a cargo ship's base was

punctured due to rat and so sea water entered and cargo was damaged. In this case there are

two causes for the damage.

i.

The ship the cargo ship getting punctured because of rats

ii.

The sea water entering ship through punctured

The risk of sea water is insured by the policy but the first cause of the punctured is not

covered by the policy. The nearest cause of damage is the sea water which is insured and

therefore the insurer must pay the compensation. Howerver, in case of life insurance, the

principle of proximate cause does not apply. Whatever may be the reason of death (whether

natural death or accidental death) the insurer is liable to pay the amount of insurance.

12

1.4 Types of Insurance

1.4.1 Life Insurance

Insurance provides protection against a wide variety of risks. However, life insurance

provides sum of amount against the various risks relating to the human being body through

issuing different policies. Life insurance is a type of insurance plan conducted by the insurers

which is directly related with providing assurance against the economic part of total human

life. It is financial instrument for providing post death resources to support survivors or pay

obligations of the state of the deceased.

Since the earning power of an individual is the greatest assets a person does have, it

really will be the most important part of human life. Life insurance is particularly concerned

with that aspect of human life. Since the insurance or assurance of a persons life is impossible

because of the certainty of the death of a person once born. Life insurance only provides

assurance against unseen future accident and it helps to live comfortably in retirement life.

Life insurance is written to economically protect the insured against financial loss in the

circumstances like living upto the age of retirement when he will not have potential earning

power, protecting insureds beneficiary if the untimely death of the insured took place, or

protecting the interest of the other parties like insured creditor who are economically

associated with the life of the insured. Life insurance provides a protection for two major

contingencies. A man insures his life either to make provision for leaving a certain sum for

his dependents when he dies, which may happen he is able to say and accumulated sufficient

amount. Life insurance has several business and financial advantage. In life insurance it is

provided that the insured interest amount is to become payable in the happening of death or in

some cases on the attainment of certain age, whichever is earlier. The concept of Life

Insurance is based on pooling the risks of many to a group, accumulating a fund by

13

contribution from the members of the group and paying from this fund the losses of those

who suffers loss.

1.4.2 Non-life Insurance

Insurance, other than life and social insurance are called non-life or general insurance.

The subject matter affected under it is in nature of property. The insurance company provides

indemnity to the insured. Such compensation should be based on the actual value. Non-life

insurance is also known as general insurance. It is a pure insurance because it can measure

any risk in terms of money. General insurance is the insurance of property and liabilities risks

of insured against some specified cost i.e, the premium. It includes property insurance,

liability insurance and other forms of insurance. General insurance considers all the risk and

it provides certainty against risk through certain sum of money. This part of insurance

includes the insurance and risk transfer of the property and liability of the insured where,

property insurance against loss arising from the ownership or use of the property, include

two general classifications.

The first, indemnifies- the insured in the event of loss growing out of damages too or

destruction of his /her property. The second form pays damages for which the insured is

legally liable, the consequence of negligent acts that result in injuries to other persons or

damage to their property. This is known as Liability Insurance. General insurance is

responsible to payment of an amount to the insured. But when the incident is held by

negligence of insured, the insurer is not responsible to pay any amount against risk.

14

1.5 Background Information of Shikhar Insurance Company Limited

Insurance Company promoted by a young team of repeated industrial and business

industrial and business houses involved in various fields like Aviation, Banking

Manufacturing, Trading, Travel Trade, Media house, etc, Shikhar Insurance is an established

General Insurance Company which was registered in company registrar's office on 206102/15

B.S (March 28 2004) and got the authority to work in the insurance industry form regulatory

board (Beema Samati) on 2061/07/26 (November 11 2004). With a vision, geared up to face

the every challenge that a persists in the insurance industry. The challenges being developing

policies as per the requirement of the client at an economical price, filling the void of the

acute shortage of technical manpower in the insurance industry, introducing new product at

par with international standards, creating capacities within a markets so that the outflow of

the precious convertible can be minimized, etc.

15

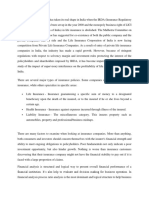

1.6 Organization Structure of Shikhar Insurance Company Limited.(Chart No.1)

Chairman

Board of

Director

Board of Director

Board of Director

Chief Executive

Officer

General Manager

Deputy General

Manager

HumanResour

ceDept.

Under

Writing

Dept

Staf

Staf

Marketin

g Dept

Account

s Dept.

Claim

Dept.

Staf

Staf

Staf

Adminis

tration

Dept.

Staf

16

1.6

Board of Directors of Shikhar Insurance Company Limited

Shikhar Insurance Company Ltd. has been promoted by a young team of reputed

Industrial and Business Houses of Nepal having vast experience and excellent leadership that

has steered their respective companies through the years. There are seventeen individuals

representing the various walks of life. They represent various diversified fields like Banking,

Insurance, Trading, Manufacturing, Aviation, Tourism etc. The Company expects to achieve

success under their abele guidance.

The below mentioned Board of Directors are responsible for the supervision of the

overall affairs of the Company.

Captain Bikas JB Rana is the Executive Chairman of Fishtail Air (P) Ltd, a Helicopter

Charter Company which was established in 1997. He is an experienced helicopter pilot with

an Instructor Pilot rating. He is the President of Air Operators Association of Nepal and was

elected unanimously for a second term as the President. Mr. Rana is a member of the Board

of Director, Civil Aviation Authority of Nepal. He is also involved in many social activities.

Mr. Ang Tshiring Sherpa is the Managing Director of Yeti Airlines Pvt. Ltd., which

was registered in November 1997 as a Private Limited Company with the three brothers

Lhakpa Sonam Sherpa, Ang Tshiring Sherpa and Ang Tending Sherpa as equal shareholders.

17

Yeti Airlines received its air operation certificate from the Civil Aviation Authority of Nepal

in May 1998 and conducted its first commercial flight in September 22, 1998 with Twin Otter

leased

from

the

Canadian

company.

Mr. Gaurav Agrawal is associated with Maliram Shiv Kumar Incorporated in Nepal as

Private Company in the year 1970 with the objective of establishing it as a trading house of

international repute, catering to commodity trading in private sector.The group specializes in

dealing textiles, consumer goods, edibles, construction materials etc. and the group act as

authorized distributer of SKF bearing in Nepal.

Lomus Investment is represented by Mr. Pradip Jung Panday. Mr. Panday has been

working in the Pharmaceutical industries for a long period of time. He is also associated with

International Leasing and Finance Company Ltd. Cosmos Cement Industries (P) Ltd. and

Nimbus Exim International. He is also the executive member of FNCCI Nepal.

18

Buddha Air Pvt. Ltd. is represented by Mr. Ramesh Kumar Luitel. Mr. Luitel has been

working in Buddha Air as Executive Manager in Expense Division of the Finance

Department.

Mr. I. P.Karmacharya is an Independent Director of Shikhar Insurance Company.

Mr. Rajendra Prasad Shrestha is an established businessman in the carpet industries of

Nepal. He is also involved in travel trade business.

19

Mr. Kiran Shekhar Amatya is an established businessman.

1.8

Management Team of Shikhar Insurance

Mr. Dip Prakash Panday, who has

more than a decade experience in the insurance field and now working in Shikhar Insurance

Company Ltd. (SICL). Before joining Shikhar Insurance Company Ltd., he served as the

General Manager at Everest Insurance for around 10 years. His professional ability and

prudence along with his strong belief in teamwork has helped him acquire experience in the

local as well as in the international market. He gives lectures on insurance in various

seminars organized by Beema Samiti and in other programs as well from time to time. He has

also attended various training programs regarding insurance in UK, India etc.

Email: dip@shikharinsurance.com

20

Mr. Bimal Raj Nepal started his career in insurance since June, 1970 from Rastriya

Beema Sansthan and had worked until 1995. Further, he continued the career in Premier

Insurance Co. (Nepal) Ltd. in 1995 and has recently been with Shikhar Insurance Co. Ltd.

since August, 2011. Hes core area of expertise is in Reinsurance and Claims. In pursuance of

his knowledge, he had the opportunity to be trained in the college of Insurance in India, UK

and Swiss Insurance Training Centre, Zurich (Switzerland) and had practical working

attachments with the various well-known companies/Reinsurers and Brokers in India and the

UK. He had also attended several seminars/conferences in Reinsurance in various countries

e.g., India, Bangladesh, Singapore, Thailand and Egypt.

Email: bimal@shikharinsurance.com

Ms. Maskay has a long experience in the insurance sector, being in Beema Sansthan

for more than 20 years. Since being exposed to insurance sector for so long period she has

indepth knowledge regarding the General Practice of Insurance. She is the first ACII

Chartered Insurer Lady of Nepal. During her span of career she has handled many

departments in Beema Sansthan like Motor Vehicle Insurance for 5 years, Fire Insurance for

12 years and Administration for 4-5 years. She conducts training classes on insurance

organized by Beema Samiti, Management Association of Nepal (MAN), Staff College and

she was also the member of the subcommittee for the fire tariff.

Email: sabita@shikharinsurance.com

21

Mr. Kafle has been in the insurance field for more than a decade and is the pioneer in

establishing Shikhar Insurance Company Ltd. During his more than ten years career in

Everest Insurance Company Ltd. he has acquired sound knowledge of various departments

like Underwriting, Reinsurance and Claim and also Research and Development. He has

participated in various seminars and training programs in Nepal and India. He conducts

programs organized by Beema Samiti and gives in-house training to staff as well. His core

strength lies in Underwriting so he assists the marketing team in dealing with the clients

related to the technical aspects of insurance. He is more of a technical guide to the marketing

team. He was working as an Assistant Manager in Everest Insurance Company Ltd. before

joining

Shikhar

Insurance

Company

Ltd.

Email: udit@shikharinsurance.com

Ms. Barishma has been in the insurance field for more than five years. She holds

MBA degree from Kathmandu University and is the pioneer in establishing Shikhar Insurance

Company Ltd. She has gained experience in various aspects of insurance like Marketing,

Aviation Insurance, and Media Planning during her service in Everest Insurance Company

Ltd. as an Assistant Manager. She has attended the Aviation training course organised by

marsh Ltd. In 2001 in UK.

22

Email: barishma@shikharinsurance.com

Mr. Nilesh Ratna Tuladhar is professionally qualified chartered accountant with more

than 15 years of work experience in accounting, finance, auditing and taxation fields. He

qualified his C.A. from ICAI, New Delhi and worked in India, U.K. and Nepal. Though

accounts and finance is his core areas, he wants to make contribution to other areas of the

organization as well through the experience he gained over the periods in various sectors. He

believes the finance is the backbone of any business organization, so timely and accurate

information along with other non financial indicators helps business to achieve its objective

and contribute its share to economic development of the country.

Email: nilesh@shikharinsurance.com

1.9 Vision And Mission of Shikhar Insurance Company Limited.

Since insurance is an arrangement by which a company or the state undertakes to

provide a guarantee of compensation for specified loss, damage, illness, or death in return for

payment of a specified premium. Shikhar Insurance is established with a vision of facing all

challenges in meeting all the requirements of the client's at most economical price.

Introducing new product which meet the international standard and believing that the

23

relationship between the insured and the insurer is that of confidence and trust. The main

objective and the goal of the company are to set the standard for the insurance industry by

providing quality service that exceeds customer's expectation. The company has the right

combination of dedicated service-oriented professionals for which one can always trust for an

excellent service and creating capabilities within the markets so that the outflow of precious

convertible currency can be minimized. Shikhar Insurance Company Limited ranks 3 rd

position out of 17 general insurance companies in the country and it aims to be and to remain

in number one position.

1.10 Different Branches of Shikhar Insurance Company Limited.

Here are altogether eighteen branches of Shikhar Insurance Company in different

parts of the country.

1.11 Different Departments of Shikhar Insurance

1. Administration and Human Resource Department

2. Marketing Department

3. Underwriting Department

4. Claim Department

5. Accounts Department

1.12 Product and Services Offered By Shikhar Insurance Company Ltd.

Human life is full of risk and uncertainties. Each and every step of life is full of risk. We

cannot eliminate risk; however, we can make provision for financial security against risk. As

insurance is developed to provide financial security to the general public against

24

uncertainties. Similarly, Shikhar Insurance also provides different variety of services in many

sectors in order to minimize the risk and to overcome the financial boarder of the people. Till

this day Shikhar Insurance been providing services in the field such as listed below.

i.

Fire Insurance

ii.

Motor Insurance

iii.

Marine Insurance

iv.

Engineering Insurance

v.

Household Insurance

vi.

Public Liability Insurance

vii.

Travel Medical Insurance

viii.

Burglary Insurance

ix.

Bankers Blanket Indemnity Insurance

x.

Money Insurance

xi.

Trekking Insurance

xii.

Cattle Insurance

xiii.

Health Insurance

xiv.

Personal Accident Insurance

xv.

Group Personal Accident Insurance

25

xvi.

Group Medical Insurance

xvii.

Other Miscellaneous Insurance

1.13

Objective of Internship

Internships can be extremely beneficial to students, graduates, or anyone looking for

hands-on expertise. As an intern, we can develop knowledge, competencies, and experience

related directly to our career goal. MBA at Kings College was launched in affiliation with

International American University (IAU), USA with a vision to produce world class

management graduates right at the home country.

So internship is a part of studies for the MBA graduates to have a real life

experiences in the field. For this, the College has created exposure foe the students Internship

Project. Because most of the employers hire almost exclusively from MBA internship pool,

this is extremely important part of the MBA learning process.

The internship program helps students to know about an organizational culture, to

know about their area of interest, to find their own strength and weakness. Students will be

able to get the practical application of theoretical knowledge which they had learned in the

College.

So As my interest in General Insurance Company where it has lots of opportunity and

after the earthquake, most of the people takes insurance as top of the requirement, I selected

an Shikhar Insurance for internship. The Shikhar Insurance Company Ltd, was established in

26.07.2016 as 15th General Insurance Company. The main purpose of establishing is to set

the standard for the insurance industry by providing quality service that exceeds customers

expectations.

26

As partial fulfillment of the requirement of the Masters of Business Administration

program me of Kings College, International American University, I was assigned to The

Operational Practice on Shikhar Insurance Company Ltd. to do a eight-weeks internship.

The main objective of an internship is to provide a practical knowledge to the students. It is a

best plat form to start a career to the students.

As internship also consist of three credit hours course. The internship will be provided

to the student as per there area of interest and their area of specialization. Some basic

objectives of an internship can be highlighted below:

Internship project helps to develop skills which will help them perform better at their

job.

It provides real life learning disclosure, diagnosing and analyzing the various

problems faced by the organization.

Provides real life view about their professions

Gives ideas to assess depth and magnitude of the various problems faced by the

organization.

Identify the alternatives for problem solutions

Establishes priorities to each problem and solution

Helps to developing the best choice of the problem solution as to facilitate

organization decision making

Internships greatly increase the chances that a student will gain full time employment.

So as per my interest in the insurance field, I got a wonderful opportunity to join as an

intern in the Shikhar Insurance.

The main objective of my internship in the Shikhar

Insurance Company Ltd. was to know about an General insurance practice and to develop my

career in the insurance level. As per my objective of internship, I got wonderful experience.

1.14

DETATILS OF INTERNSHIP AT ORGANIZATION

1.14.1 Background

27

Since internship was for two month, during internship assisted in to different department

like:

Underwriting Department

Claim Department

Reinsurance Department

Administrative Department

Human Resource Department

Marketing Department

1.14.2. Details of Underwriting Department:

Under the underwriting department I have learned the issue of the calculation

premium and issue of the following polices:

Marine Insurance Policy

The oldest form of insurance, the marine insurance policy will be written to provide

the security againt the perils of sea. Ships sailing on are exposed to various kinds of risk.

They may colloid against one another, spring a leak, caught by fire, captured enemies and

seized by pirates. The ship and cargo may be lost in such a case and a tremendous loss may

be caused to its owners. Such risks if not covered will greatly discourage the international

trade, which is mostly sea borne. That is why the marine insurance is considered to be the

land mind of modern international trade, which is indispensable auxiliary. The modified

modern insurance policy provides the protection against various risks which does not belong

to sea. The modern insurance policy provides the protection against inland transit loss, which

is arising in the way to seller and buyer, and protection against loading and unloading also. In

practice we can see following insurance policy under marine insurance: a) Ship insurance b)

cargo insurance c) Freight insurance.

Fire Insurance

28

Fire insurance had been originated in Germany in the beginning of sixteenth century.

Fire insurance policies are issued to indemnity owners of property, whether buildings or

contents, against destruction or damage caused by fire and lightening. In generic form fire

insurance provides indemnity for loss or damage caused by fire. Fire insurance policy may be

taken on residential houses or on factories and business premises. Under fire insurance

policy, if any property lost by fire the insured amount would pay as indemnity. The property

should be in its full market value. The claim under the fire insurance policy is determined on

the basis of present value of property. The field of fire insurance can be modified or extended

to include a number of peril closely allied to fire like wind , storm, earthquake, riot and strike,

damage, terrorism, explosion, landslide or else. Insurer may charge higher premium as per the

nature of risk and insurance policy.

Aviation Insurance Policy

Aviation insurance is related the risk occurring due to peril, hazards or risks created

by the aircraft. Aviation insurance provides the indemnity against the risk, which is created on

flight, landing and the time of take off of an aircraft. The subject matter of this type of

insurance will be aircraft itself, which require very huge capital investment. Aviation

insurance requires the risk of passenger, cargo, hull (plane) also. The Aviation Insurance is

essential and important in aviation field. Because of huge capital outlay, individual

organization operating the airlines business couldnt bear the risk associated with the aircraft

and the insurance companies particularly form a syndicate to bear the risk associated.

Automobile Insurance Policy

Automobile insurance policy is related to the risk of vehicles. It provides certainty

against the risk of accident. It is the insurance policy related to the vehicles running on the

road. It is directly related with providing the insurance against the peril or loss occurring with

29

respect to vehicle and with providing financial assistance to the insured to remit the third

party liability occurring to the damage caused by the vehicle. The Aviation insurance covers

the full comprehensive policy and third party liability insurance too.

Engineering Insurance Policy

Engineering insurance policy is directly related against the risk of engineering tools

and technique. Engineering insurance is related with the risk transfer arrangement against

peril, hazards or risk arising within manufacturing organization or within technical job

sectors. A manufacturer has the risk of break down of his/her plant and machinery and may

produce disqualified goods. However, Engineering insurance provides the protection against

that situation. Usually under this policy there will be basic risks contracts.

Boiler Insurance

Usually, all the big and small industry has installed the boiler machine to produce

steam power. Under this arrangement, the risk occurring due to explosion or damage of

industrial boiler will be insured. Where the boilers are used, there is always the possibility of

explosion or breakdown. Therefore, the boiler owner wants to get protection of such types of

risk. In such breakdowns the person may be injured or the property may be destroyed. At that

condition boiler insurance provides the protection against the risks of boiler.

Contractors All Risk Insurance

Under this arrangement the hazards, perils and losses occurring from the mutually

accepted risk class will be provided for the contractors, whether they are individuals or

organizations. Under this risk class the loss occurring from natural disasters, accidents or

other inevitable uncertainties will be incepted. It insures the contractors or builders financial

instability though there occurs heavy loss on contract, upon which they are working.

30

Machinery and All Insurer Risk Insurance

Under this arrangement the loss occurring due to the damage of the machinery will be

insured. Under this insurance an insured assure his/her machinery against the risk of

breakdown and failure. When the machine is broken-down at that situation s/he has to bear

the losses of worker wages and repairing cost too. But the machinery all risk insurance

provides the certainty against such types of risk. Such policy includes financing for the failed

machinery, providing financial security against the indirect cost like repairing cost, cost of the

idle workers or similar losses.

Miscellaneous Insurance Policy

There exists many insurance covering different fields of risk classes. A number of

coverages written by causality insurers are available that cannot be classified neatly as

liability, auto or crime insurance but nevertheless are important to those with the exposure

that these forms are designed to protect. They are discussed under the innocuous heading of

miscellaneous coverage and are written by property and liability insurance (Maher &

Cammack, 1974:344).

Household Policy

Under this policy insurer writes the insurance against the risk of personal

house/building and other properties. In this policy, the loss occurred due to the natural

disaster like earthquakes windstorm, lightening and the loss occurred due to the other

disasters like earthquake windstorm, lightening and the loss occurred due to the other

31

disasters like vandalism; riot is financially protected from the insurer if this insurance policy

is written.

Medical Aid Scheme Insurance

Under this policy insurer provides the financial support against the heath problem to

the insured. In this policy, insurer will be responsible to pay the all medical expenses for the

insured if the insured needs medical treatment unexpectedly within the insurance written

period.

Fidelity Guarantee Insurance

The word stays at the faith. But the fidelity guarantee insurance is attended in the case

of fraud and dishonesty. Under this policy the owner of the firm, organization gets the

guarantee against the fraud or betrays or dishonesty caused by the employees like

accountants, cashiers distributors etc. The insurer fulfills the loss occurring due to the discard

of the fidelity of the beloved person banks saving and loan associations, and other business

in which employees have access to large sums of money in variably carry fidelity bonds for

protection (Welshman & Meliche,1980:214).

Workmens Compensation and Employers Liability Insurance

This insurance is a means of motivation to the worker because a firm/organization

gives indemnity to the worker if they get occupational accident. For this purpose, the owner

of the firm on behalf of the worker will purchase workmens compensation and employers

liability insurance. In this policy the insurer provides the financial support if the worker

meets with the accident within the working place and time. This scheme will be written by

the owner of the firm to secure from the unexpected claims occurring due to the occupational

accident that took place on the work place. Workmens compensation and employers liability

32

insurance assumes the expenses of compensation and provide for medical, surgical and

hospitalization requirements as determined by the compensation laws of the state.

1.14.3 Details of Claim Department

I spent almost 12 days in the claim department of shikhar insurance Company Ltd.,

being with that department, I have learnt following things

Insurance an intangible product

What Insurers sell in Insurance business is not a material thing. Insurers' products are

immaterial objects Promises or words of mouth only. Should the insurers fail to meet their

commitments (promise) when in actual need, or if they adhere to some plea or others not to

fulfill their promises, it would definitely be detrimental to the clients. It might also lead to the

situation of 'no trust' towards the Insurance Industry as a whole.

Claims settlement Primary function of Insurers

The settlement of claims is one of the important functions of the insurers. In fact, the layman

understands the functions of an insurance company are to receive the premiums at the time of

affecting insurance and pay the claims whenever they crop up. Claims are thus the acid tests

for the Insurers.

Proper settlement of the claims requires a sound knowledge of the principle and practices

governing the insurance contracts, a through knowledge of terms and conditions of the

concerned Insurance policies, deep experience of the client's behaviors etc.

33

Claims Settlement Procedures

Claims settlement procedures can be considered under the three broad headings:

1. Preliminary procedures

2. Claims assessment procedures

3. Claims settlement procedures

1. Preliminary Procedures

Notification of Loss:

-

Policy conditions require that any incidence giving rise to claims or likely to give rise

to claim must immediately be notified to the Company.

Time limits by which the notification should be given are specified in the policy

condition.

Some require immediate notification whereas others require notice to be given as

early as possible.

Purpose of early notification is to enable the Insurers to investigate into the

circumstance of the loss and quantum of loss at its early stage. This also enables the

insurers to suggest measures to minimize the loss and measures to protect the salvage.

Moreover, early notification is necessary to find out the exact cause of loss and to

protect the evidences.

Unnecessary delay in notification of the loss adversely affects the Insurerers' position

and hence the claim might be treated as non-standard by them.

Notification in liability policies relate to:

i)

Notification of the happening of accident

34

ii)

-

Notification of the claim received by the insured or suit filed against them.

In many Policies, especially in accident and theft, Police Office has to be notified for

investigation of the incidence and also find the persons at fault.

Loss minimization:

-

Policy conditions impose the duty on the Insured to act as if he is un-insured.

This means that the Insured should take every precautions and measures to prevent or

minimize the loss.

Should the insured incidence occur, the insured has to take steps to protect the

property from further loss/ damage. For example, in the Motor Insurance, the Insured

should not leave the ill-fated vehicle unattended and the vehicle should be taken to the

safe place to prevent happening of the further loss.

Procedural:

Once notification of claim is received by the insurers, they check the followings:

i)

The relevant Policy documents and all attachments thereto

ii)

The loss is in the Policy period of Insurance

iii)

The loss is caused by the Insured Peril

iv)

The subject matter of the loss is the same as has been insured in the policy.

v)

Notice of loss is received in the stipulated time

Once the above details are checked, Insurance Company allots the Claim Number & opens

the separate Claim file.

Claim form:

35

Claim form is the document to record formal notification of claim with details of

Policy, circumstances of loss, nature of loss , extent of damage and other details.

Nature of claim forms varies from types of insurance.

Since Non-life insurance is the Policy of indemnity, questions are asked whether there

are other insurances covering the same subject matter. This enables the insurers to

enforce the right of Subrogation and contribution.

Issuance of claim form by the Company does not constitute an admission of liability.

Hence the claim form is issued 'without prejudice'

Claim forms are necessary in Fire, Motor and other accident insurances. In Marine

insurance, claim form is issued only on inland transit claims.

2. Investigative & Assessment procedures

Investigation and assessment of the loss begins immediately after receipt of notification.

Sometimes, even the receipt of the claim form is not awaited.

-

if quantum of loss is small, concerned Claim Officials themselves make investigation

& assessment.

Larger & complicated claims are given to independent professional surveyors, who

are specialized in the particular line.

Appointment of the surveyor is intimated to the claimant. The Surveyor is given all

relevant papers including Policy and endorsements, claims forms etc. The rest of the

papers he will collect from the insured or might ask the insured to submit him or the

insurance company subsequently if the papers are not immediately available.

Surveyors and Loss Assessors:

36

Surveyors are the independent persons who are given licence to work as the Insurance

surveyors by the Regulatory Authorities. In Nepal, Beema Samiti provides license to the

eligible persons after they attend the training courses organized by the Samiti from time to

time. The following persons are eligible to become a Surveyor:

a)

At least ten years' of working experience in Insurance Companies as

officer.

b)

Person holding at least Bachelor Degree in engineering subject.

c)

Person holding at least Bachelor degree from the Chartered Insurance

Institute or any other such organization recognized by them.

d)

Chartered Accountants.

Surveyors have been classified into five categories as below:

1) Class 'A' those working as surveyors for more than 15 years

2) Class 'B' those working as surveyors for more than 10 years

3) Class 'C' those working as surveyors for more than 5 years

4) Class

'D'

those

newly

licensed

or

working

as

surveyors

for

less than 5 years.

As per the regulation, Surveyors have to submit their reports within 15 days of their

appointment.

In large losses, preliminary surveyors are initially deputed to inspect and record the damages

or losses at the spot. Subsequently, another final Surveyor may be deputed to investigate and

37

assesses the loss or the preliminary surveyor himself may be asked to do the final assessment

job depending on the severity and quantum of loss and also the category of the surveyor.

Practice in Marine Insurance:

Since Marine Insurance is of International nature, the names of the Surveyors/ Loss

Assessors/Claim Settling Agents are named in the schedule of the Policy. Should the

consignor receive the goods in lost or damaged conditions, he has to apply to the surveyors

named in the policy and send their reports to the Insurers along with the other documents

relating to the claim. The consignee initially pays to the Surveyors their remunerations and

expenses which are reimbursed by the Insurance Company along with the final claims

assessment figure.

General Average (G.A.) losses are assessed by the by specialists i.e. Average Adjusters.

Claims Documents

Submission of other claim documents, along with claim form and survey reports, is necessary

to prove the incident and substantiate the claim. The types of documents required vary from

types of the insurance portfolio. Some examples of the documents needed are as under:

1) Fire Claims:

-

Police report of the incidence

Fire Brigade Report

In case of allied perils like storm/flood/ earthquake etc claims report of the

Metrological Department.

Letter of Subrogation if the incidence is suspected to be blamed to some third parties.

38

2) Marine Cargo Claims:

The types of documents required for Marine Cargo Claims depend on the nature of loss

total loss, partial loss, general average loss. However, the common documents required are as

below:

-

Original Policy: required to see that the interest said to have been lost or damaged is

the same as insured in the policy.

Invoice: provides evidence of the value of shipment.

Packing lists

Evidence for the receipt of the goods by transporters e.g. Bill of Lading, Consignment

Note, Airway Bill, Railway Receipt

Non-delivery or Shortage Certificate from the carriers or certificate or notes of the

delivery in damaged conditions.

Copies of the correspondence exchanged with the carriers, port authorities etc.

regarding the loss and asking them to make good the losses.

Letter of Subrogation

In case of inland transit, police report of the incidence to the carrying vehicle,

incidence of looting or theft or riot etc. resulting in the loss/damage of the cargo

3) Motor Insurance Claims:

-

Police report of the Incidence

Details of the third party claims Bodily injury / Property damage.

Quotations for the repairs of damaged vehicle/ Third Party property.

39

In case of their party injury details of the medical reports along with the medical

precipitins and bills, nature of the permanent total disablement. In case of the death of

the third party, post mortem report and the verdict of the Court.

3. Claims Settlement Procedures:

Once the claims are assessed by the Surveyors and the same is approved by the Insurers,

the claims are ready for settlement. Insurance Companies issue Discharge Vouchers which the

insured is required to sign and return the same to the company. Discharge Voucher fulfils the

following requirement:

Works as the receipt of the money by the insured

Discharges the insurers, having received the claims payment from all further liability

in respect of the said incidence.

Mostly insurers issues the cheque after the discharge voucher is duly signed and returned

to them. However, it is also the practice to attach the cheque along with the discharge

voucher.

Claims Disputes:

Dispute between the Insurance Company and the Insured arise when

i)

The company repudiates the claim in various grounds e.g. the subject matter of

insurance is different, the risks which caused the loss is not covered under the

ii)

policy, policy conditions not complied with etc.

The quantum of loss as assessed or as offered by the insurance company is not

satisfactory to the claimant.

In Nepal, if the companies could not settle the disputes amicably, the Insured can file the

case with Beema Samiti, which also act as the semi-judicial body. Should their decision not

40

acceptable to either of the Parties, they can appeal to the district court within the stipulated

time.

Conclusion:

Claim settlement is one of the main and primary functions of insurance. Insurer's

reputation depends on how proper and quick settlements of claims are executed by them.

However, some insurance clients are sometimes found lodging fraudulent or aggravated

claims. Such claims have to be investigated and discouraged. Settlement of such fraudulent

claims encourages moral hazard which is detrimental to the insurers and the insurance

industries as a whole. Hence, claims management of the Insurance Company Insurers has

mainly to see:

-

Genuinely of claims that they are not fraudulent or exaggerated

Losses/damages reported are well within the preview of the policy.

If the above two factors could be satisfies, requiring to submit some other not very relevant

documents could well be avoided, as surveyors investigations by site visits could normally

establish the incidences and losses.

41

1.14.4 Details of Re-Insurance Department

The practice of insurers transferring portions of risk portfolios to other parties by

some form of agreement in order to reduce the likelihood of having to pay a large

obligation resulting from an insurance claim. The intent of reinsurance is for an insurance

company to reduce the risks associated with underwritten policies by spreading risks

across alternative institutions. Throughout the internship period, I have learnt following

things with the help of Staff of shikhar Insurance Company Ltd.

42

Process :

Insurance

/Reinsurance

Why Re-Insurance

To create Capacity

To bring Flexibility offer new products

To maintain stability To Protect the company from fluctuation of claims experience

year to year. Without reinsurance facility , companys accounts would have swept

out with one bigger or accumulation of many small claims

Brokers

K.M. Dastur Reinsurance Brokers , Mumbai

J.B. Boda & Co. Ltd , New London

43

Method Re-Insurance

Treaty Reinsurance

Automatic arrangement

So, low admin cost

High Commission & local taxes borne by Reinsurers

Facultative Reinsurance

Full details of risks each time

Right to accept or reject

Commencement & end with period of Policy

REINSURANCE PROCESS

Basis of Re-Insurance Selection

Profile

44

Re-insurers paying capacity and their support

Financial Soundness

Must be dispersed worldwide and assist us in case of our needs

Fully integrated claims handling and claims management service

Treaty Reinsurers

GIC , India ------

LEADER

------

Tokio Marine , Bangkok

-----

Kuwait Re

-----

African Re

-----

Malaysian Re

-----

Best Re

-----

Travel Trip and Trekking

Sirius International

45

1.14.5 Details of Account Department:

As account department is one the important department of every organization which

keeps the records relating to the accounting and financial transaction. This is the department

which shows the financial position as well as the financial condition of every organization.

The information provided by this department is very useful for decision making.

Some basic things that I learned in the account department during the internship periods are

as follows:

Issue payment vouchers and record the receiving cash.

Posting all the booking transaction in to respective ledger as per the index number of

respective book.

46

Preparing monthly report.

As, the Insurances accounting treatment shall be done as per the rule prescribed by the

insurance Board, Beema Samiti.

The voucher payment procedures and cash receiving

procedures will be done as per the procedures of government. All the payment and receiving

amounts are converted in to Nepalese amount for Aviation Insurance Policies. And each and

every transaction should be entering into the accounting system on Premia Software.

1.14.6 Administration Department and Human Resource:

Administration department is another department of an organization which combines

all the resources required for the work to be done. This department helps smooth flow of

organization i.e day to day operation of organization. This department is interconnected with

each other department.

Following are the things which I learned in Administration.

Preparing Roster duties which are prepared by assigning the duties of staff during the

holidays.

Preparing quotation for CCTV installation and involved in the selection process.

Preparing Vacancy advertisement notice for Messenger.

Managing file in the drawer, as per date.

Recording keeping of all incoming and outgoing documents, letters in different

department as per the specification.

Maintaining adequate level of inventory of different types of condition which is

requiring in the process of issuing the policies.

47

CHAPTER TWO

ASSIGNMENTS/ ACTIVITIES /PROJECTS UNDERTAKEN

2.1 ASSIGNMENT UNDERTAKEN DURING THE INTERNSHIP

As internship was in insurance field and staff of the organization are more aware what

roles responsibilities should be given to intern.. However, I completed the following

assignment during my internship period:

Value Added Tax (VAT) Calculation

VAT claim report preparation and Online claim submission.

Indexing receipt and payment voucher as per the schedule prescribed by the Beema

Samiti

Calculation of premium for the insurance

Segregating amount for Co-insurance and facultative

48

2.2 PROJECT/ACTIVITIES / FUNCTIONS PERFORMED DURING THE

INTERNSHIP

Shikhar Insurance is one of the emerging insurance companies in terms of General

Insurance Company Ltd. It performs different activities which are scheduled in their budget

program.

Following are the activities/ functions performed during the internship:

Attended different insurance seminar

With the absent of related staff in specific area like Re-insurance, I maintain and

helps for the smooth operation of the work.

CHATPER THREE

PROGRAM WORKPLACE RELATIONSHIP

Since, the workplace was different than the usual in other internship. I was the 30 th

person to do internship in the Shikhar. So with full of enthusiasm I started my internship. The

work place so different then what I have thought. I had thought that, the new people, new

work place, different culture, some difficulties may arise. But I was absolutely proven wrong.

The co-operative, helpful behavior of the staff of Shikhar impressed me totally. In the

Shikhar, at top level, all the staffs were home based staff. They assisted me to learn, how to

perform different tasks with full support and love. Even all the staff members were happy

with me and with my work. At the end of the day, I got a farewell party from Insurance, with

token of love from every staff member, which was so overwhelming. In the short span of

time, I had become so friendly. We committed to be in touch and exchange each other contact

medium.

49

The working environment was so down to earth for my help. Senior level manager

used to invite me in any dinner reception thorough which I would be able to meet higher level

personalities and view the practices of insurance. They used to give me different practical

knowledge related to life as well as career which are so useful in day to day life. I am so

happy to be a part of Shikhar. With a short time period, I have been able to create a

harmonious relation with the Shikhar.

CHAPTER FOUR

CONCLUSION

My learning experience with the Insurance begins with my joining from 07 th July,

2015 to 6th September, 2015 which was of two months internship. My internship report

contains all the information about my work experience with the Insurance.

During internship in the Insurance, Shikhar, I came to know about General Insurance

practice in the accounting, administration, Underwriting, Claim and Re-Insurance. The intern

was good platform for learning and understands the implication of theoretical knowledge in

to practical, learnt to deal with different situations, had experience of organizations working

environment which affects an employee performance and the attitude towards work.

50

All in all, the experience of working and learning at the same time in such a reputable

organization is awesome. It will be unforgettable experience of my life where I learnt the way

to behave and polish my abilities at the organization level, had the experience and exposure

of performing and handling tasks, supervisor and subordinate relation and the development of

my knowledge, skills and abilities (KSA) and was able to practically apply my studies of

Management Level.

BIBLIOGRAPHY

http://www.britannica.com/topic/insurance

http://www.iap.net.pk/Displaypage.aspx?ID=2

http://www.ragnaroek-festival.com/index.php/en/?

option=com_k2&view=itemlist&task=user&id=1361

https://www.geico.com/more/saving/insurance-101/unusual-insurance-policies/

http://www.bsib.org.np/

http://shikharinsurance.com/

You might also like

- Ocular Trauma - BantaDocument211 pagesOcular Trauma - BantaLuisa Fernanda Arboleda100% (1)

- Project Report On Financial Performance of Life Insurance CompanyDocument11 pagesProject Report On Financial Performance of Life Insurance CompanyMasters VinodNo ratings yet

- HDFC ERGO SummeerIntern Ship Project ReportDocument70 pagesHDFC ERGO SummeerIntern Ship Project Reportskaushik040260% (5)

- Internship Report FormatDocument26 pagesInternship Report Formatashish tiwari0% (1)

- Internship Report On HR of InsuranceDocument50 pagesInternship Report On HR of InsuranceSabila Muntaha Tushi0% (1)

- Internship ReportDocument22 pagesInternship ReportBadari Nadh100% (1)

- Internship ReportDocument45 pagesInternship ReportTushar GargNo ratings yet

- Comparative Analysis of Different Insurance ProductsDocument53 pagesComparative Analysis of Different Insurance Productsgsaraogi85% (39)

- Fin 320 - Individual AssignmentDocument14 pagesFin 320 - Individual AssignmentAnis Umaira Mohd LutpiNo ratings yet

- Intern Report UniglobeDocument30 pagesIntern Report UniglobeShrestha Anjal100% (1)

- Presentation of InternshipDocument26 pagesPresentation of InternshipBishnu Dhamala0% (1)

- Rastriya Beema CompanyDocument35 pagesRastriya Beema CompanyAsmita Sharma67% (6)

- Internship Report On Popular Life Insurance CompanyDocument58 pagesInternship Report On Popular Life Insurance Companysrb199175% (16)

- Insurance Internship ReportDocument32 pagesInsurance Internship Reportian opondo0% (1)

- Internship Report On Peoples Insurance Company LimitedDocument28 pagesInternship Report On Peoples Insurance Company LimitedRafiuddin Biplab91% (11)

- Neha BistDocument31 pagesNeha BistSupreme ComputerNo ratings yet

- Summer Internship ReportDocument49 pagesSummer Internship ReportSỡumệŋ MaŋdalNo ratings yet

- ConclusionDocument2 pagesConclusionNeerajNo ratings yet

- Intern Report 1Document32 pagesIntern Report 1Asan Bilal100% (1)

- Mounika BBA Insurance PoliciesDocument51 pagesMounika BBA Insurance Policiessreevalli100% (1)

- Literature Review INSURANCEDocument16 pagesLiterature Review INSURANCEgunmeet60% (5)

- Tata Aia Talreja Edit56Document63 pagesTata Aia Talreja Edit56ankitverma9716100% (1)

- Internship ProjectDocument29 pagesInternship ProjectArun SinghNo ratings yet

- Asian Life InsDocument34 pagesAsian Life InsLaxman Thapa100% (1)

- A Project Report On ICICI Prudential Life InsuranceDocument37 pagesA Project Report On ICICI Prudential Life InsuranceSudha Sandesh Ambekar86% (42)

- Internship ReportDocument58 pagesInternship Reportdata teamNo ratings yet

- New Jubilee Internship ReportDocument92 pagesNew Jubilee Internship ReportYasir Ayaz100% (11)

- Internship ReportDocument33 pagesInternship ReportPriyanka A SNo ratings yet

- Shikhar Insurance ReportDocument12 pagesShikhar Insurance ReportRoshan AcharyaNo ratings yet

- Risk Management in Insurance IndustryDocument17 pagesRisk Management in Insurance IndustryAndrew GomezNo ratings yet

- INTERNSHIP REPORT XXXXXXXXXXXXXXXXXDocument39 pagesINTERNSHIP REPORT XXXXXXXXXXXXXXXXXResearcher BrianNo ratings yet

- Internship Report On Habib Bank Limited: University of GujratDocument65 pagesInternship Report On Habib Bank Limited: University of GujratMehran RiazNo ratings yet

- CSR Project On InsuranceDocument69 pagesCSR Project On Insurancedhwani0% (1)

- Summer Internship ReportDocument32 pagesSummer Internship ReportRaghav SinglaNo ratings yet

- Suggestion and ConclusionDocument4 pagesSuggestion and ConclusionSidhantha Jain100% (1)

- Project Report On Field Study in Insurance SectorDocument86 pagesProject Report On Field Study in Insurance Sectorsunny_choudhary@hotmail.com100% (1)

- HDFC Licnew FinalDocument71 pagesHDFC Licnew FinalRohit Kumar100% (1)

- Internship ReportDocument54 pagesInternship ReportNichole John ErnietaNo ratings yet

- Summer Internship ProjectDocument63 pagesSummer Internship ProjectHansha ThakorNo ratings yet

- Internship Report RSDocument58 pagesInternship Report RSLayes AhmedNo ratings yet

- Internship ReportDocument25 pagesInternship ReportKansiime MuhamedNo ratings yet

- Comparative Study On Icici Prudential Life Insurance and HDFC Standard Life InsuranceDocument9 pagesComparative Study On Icici Prudential Life Insurance and HDFC Standard Life InsuranceRakesh MishraNo ratings yet

- A Project Report ON: Royal Sundaram Insurance CompanyDocument12 pagesA Project Report ON: Royal Sundaram Insurance CompanyKritika PrasadNo ratings yet

- Risk Management in Life InsuranceDocument52 pagesRisk Management in Life InsuranceBhabani Shankar LenkaNo ratings yet

- Project On Motor Policy With Reference To New India Assurance Company LTDDocument72 pagesProject On Motor Policy With Reference To New India Assurance Company LTDDaMo DevendraNo ratings yet

- Internship ReportDocument5 pagesInternship ReportJahidul AlamNo ratings yet

- Comparative Performance Analysis of Life Insurance Companies EditedDocument85 pagesComparative Performance Analysis of Life Insurance Companies EditedSumana Sadhukhan0% (1)

- Mba Insurance Black BookDocument59 pagesMba Insurance Black BookleanderNo ratings yet

- Bharti Axa Life Insurance ProjectDocument80 pagesBharti Axa Life Insurance ProjectTripti Srivastava100% (1)

- Project Synopsis of Insurance CompanyDocument4 pagesProject Synopsis of Insurance CompanySamar GhorpadeNo ratings yet

- Marketing Strategies of Icici Prudential Life Insurance of College..Document69 pagesMarketing Strategies of Icici Prudential Life Insurance of College..Chitranjan SharmaNo ratings yet

- A SUMMER INTERNSHIP PROJECT REPORT (1) PoojaDocument41 pagesA SUMMER INTERNSHIP PROJECT REPORT (1) PoojaRubina MansooriNo ratings yet

- Internship PresentationsDocument9 pagesInternship PresentationsAnil vNo ratings yet

- A Project On "Customer Acquisition For Aditya Birla Sun Life Insurance Company, Pune."Document48 pagesA Project On "Customer Acquisition For Aditya Birla Sun Life Insurance Company, Pune."Shashank Rangari100% (1)

- Accounting Internship ReportDocument7 pagesAccounting Internship Reportsanthigolla_200260% (5)

- Project On Max Life InsuranseDocument48 pagesProject On Max Life InsuranseSumit PatelNo ratings yet

- Recruitment and Seletion (Birla Sun Life Insurance)Document49 pagesRecruitment and Seletion (Birla Sun Life Insurance)Aakash Chauhan100% (2)