You might also like

- Bangladesh: Bangladesh National Building Code (BNBC)Document47 pagesBangladesh: Bangladesh National Building Code (BNBC)gdl111100% (3)

- Conservation Status of Tree Species in Himchari National Park of Cox's Bazar, BangladeshDocument10 pagesConservation Status of Tree Species in Himchari National Park of Cox's Bazar, BangladeshmoonnaNo ratings yet

- Plantation and Management Plan For Camp 4, Cox's BazarDocument15 pagesPlantation and Management Plan For Camp 4, Cox's BazarmoonnaNo ratings yet

- Marina Bay Sands, Singapore 03 PDFDocument25 pagesMarina Bay Sands, Singapore 03 PDFmoonnaNo ratings yet

- Bristol Harbourside Building 10: Cullinan StudioDocument2 pagesBristol Harbourside Building 10: Cullinan StudiomoonnaNo ratings yet

- Chapter 14Document14 pagesChapter 14moonnaNo ratings yet

- Rietveld Schröder House's Open Plan and De Stijl DesignDocument8 pagesRietveld Schröder House's Open Plan and De Stijl DesignmoonnaNo ratings yet

- CS of Charges 2017Document1 pageCS of Charges 2017moonnaNo ratings yet

- Architectural Spaces & Forms: 5 Year 2 Semester. Department of Architecture, AustDocument1 pageArchitectural Spaces & Forms: 5 Year 2 Semester. Department of Architecture, AustmoonnaNo ratings yet

- 26 Case Study Marina Bay Sands SingaporeDocument7 pages26 Case Study Marina Bay Sands SingaporeGladys MatiraNo ratings yet

- Dhaka Imarat Nirman Bidhimala-2008Document142 pagesDhaka Imarat Nirman Bidhimala-2008sazeda67% (3)

- Consumer Schedule of Charges 12-09-2017Document1 pageConsumer Schedule of Charges 12-09-2017moonnaNo ratings yet

- Marina Bay Sands, Singapore 03 PDFDocument25 pagesMarina Bay Sands, Singapore 03 PDFmoonnaNo ratings yet

- Site 64 Scaled FinalDocument1 pageSite 64 Scaled FinalmoonnaNo ratings yet

- Lecture 04 - Series Parallel NetworksDocument19 pagesLecture 04 - Series Parallel NetworksmoonnaNo ratings yet

- Assignment - FINAL 1Document2 pagesAssignment - FINAL 1moonnaNo ratings yet

- St-4 Lecture For MidDocument15 pagesSt-4 Lecture For MidmoonnaNo ratings yet

- Brick CloserDocument1 pageBrick ClosermoonnaNo ratings yet

- Chapter - 01 - Managerial Accounting PDFDocument9 pagesChapter - 01 - Managerial Accounting PDFmoonnaNo ratings yet

- Teacher'S Schedule Form: Summer Semester, 2014-2015Document1 pageTeacher'S Schedule Form: Summer Semester, 2014-2015moonnaNo ratings yet

- Chapter 02 Managerial AccountingDocument13 pagesChapter 02 Managerial AccountingmoonnaNo ratings yet

- Reinforced Concrete (RC) Vs Pre-Stressed Concrete (PC)Document2 pagesReinforced Concrete (RC) Vs Pre-Stressed Concrete (PC)moonnaNo ratings yet

- Lecture 03 - Parallel CircuitDocument21 pagesLecture 03 - Parallel CircuitmoonnaNo ratings yet

- Assignment - FINAL 1Document2 pagesAssignment - FINAL 1moonnaNo ratings yet

- Kahve Time: PedestrianDocument1 pageKahve Time: PedestrianmoonnaNo ratings yet

- Wood Boards, Planks & Tiles for ProjectsDocument1 pageWood Boards, Planks & Tiles for ProjectsmoonnaNo ratings yet

- Survey Tech - Course OutlineDocument5 pagesSurvey Tech - Course OutlinemoonnaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Credit Rating Agencies PDFDocument17 pagesCredit Rating Agencies PDFAkash SinghNo ratings yet

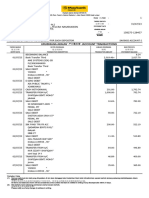

- Statement of AccountDocument2 pagesStatement of Accountmdyakubhnk85No ratings yet

- An Auditor's Services: Principles of Auditing: An Introduction To International Standards On Auditing - CH 4Document47 pagesAn Auditor's Services: Principles of Auditing: An Introduction To International Standards On Auditing - CH 4febtrisia dewantiNo ratings yet

- RATIO HavellsDocument22 pagesRATIO HavellsMandeep BatraNo ratings yet

- ISO 9001:2000 Goat Production Profitability AnalysisDocument38 pagesISO 9001:2000 Goat Production Profitability AnalysisJay AdonesNo ratings yet

- Super Secret Tax DocumentDocument4 pagesSuper Secret Tax Documentk11235883% (6)

- Analysis of Option Combination Strategies: February 2018Document11 pagesAnalysis of Option Combination Strategies: February 2018Shubham NamdevNo ratings yet

- Chapter 14 Financial StatementsDocument82 pagesChapter 14 Financial StatementsKate CuencaNo ratings yet

- Genealogy ReportDocument2 pagesGenealogy Reportzhaodonghk3No ratings yet

- Enterprise Valuation FINAL RevisedDocument45 pagesEnterprise Valuation FINAL Revisedchandro2007No ratings yet

- MamaearthDocument9 pagesMamaearthAmar Singh100% (1)

- Ahmed Khalid and Nadeem HanifDocument24 pagesAhmed Khalid and Nadeem HanifVaqar HussainNo ratings yet

- SabziwalaDocument6 pagesSabziwalaSomnath BhattacharyaNo ratings yet

- Calculating partnership profits and capital balancesDocument1 pageCalculating partnership profits and capital balancesDe Nev Oel0% (1)

- Assessment of Local Fiscal Performance DevelopmentsDocument2 pagesAssessment of Local Fiscal Performance DevelopmentsKei SenpaiNo ratings yet

- M2U SA 128457 Jul 2023Document5 pagesM2U SA 128457 Jul 2023syafiqah.mohdali38No ratings yet

- Finance SOP (Example - 1) (1553)Document4 pagesFinance SOP (Example - 1) (1553)Rindy Murti Dewi100% (1)

- Research Proposal:Share Market Efficiency: Is The Indian Capital Market Weak Form Efficient?Document13 pagesResearch Proposal:Share Market Efficiency: Is The Indian Capital Market Weak Form Efficient?Adil100% (4)

- SahooCommittee Ecbreport 20150225Document109 pagesSahooCommittee Ecbreport 20150225advpreetipundirNo ratings yet

- Phil. Home Assurance Corp vs. CADocument1 pagePhil. Home Assurance Corp vs. CACaroline A. LegaspinoNo ratings yet

- Technical Analysis Portfolio ConstructionDocument4 pagesTechnical Analysis Portfolio ConstructionChandrashekhar ChanduNo ratings yet

- GIC Report 2019 20 1Document84 pagesGIC Report 2019 20 1a aaaNo ratings yet

- Wealth Management in Delhi and NCR Research Report On Scope of Wealth Management in Delhi and NCR 95pDocument98 pagesWealth Management in Delhi and NCR Research Report On Scope of Wealth Management in Delhi and NCR 95pSajal AroraNo ratings yet

- Allapacan Company Bought 20Document18 pagesAllapacan Company Bought 20Carl Yry BitzNo ratings yet

- Chapter 3 Interest and EquivalenceDocument32 pagesChapter 3 Interest and EquivalenceBaker VlogsNo ratings yet

- Bank of Khyber Internship Report For The Year Ended 2010Document108 pagesBank of Khyber Internship Report For The Year Ended 2010Mohammad Arif67% (3)

- ch02 - Financial Planning Skills-Tb - Mckeown - 2eDocument18 pagesch02 - Financial Planning Skills-Tb - Mckeown - 2e李佳南No ratings yet

- CPA Licensure Exam Syllabus for Management Advisory ServicesDocument16 pagesCPA Licensure Exam Syllabus for Management Advisory ServiceskaderderkaNo ratings yet

- Hotel FranchiseDocument10 pagesHotel FranchiseTariku HailuNo ratings yet

- Equity Investment BrochureDocument3 pagesEquity Investment BrochureCHANDRAKANT RANANo ratings yet