You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- VALUE ADDED TAX Notes From BIRDocument30 pagesVALUE ADDED TAX Notes From BIREmil BautistaNo ratings yet

- Camp John Hay Development Corporation vs. Central Board of Assessment Appeals (Cbaa)Document3 pagesCamp John Hay Development Corporation vs. Central Board of Assessment Appeals (Cbaa)lexxNo ratings yet

- Kanu Equipment DRC SASU Sales Quote for KIS KANDUDocument2 pagesKanu Equipment DRC SASU Sales Quote for KIS KANDUkandukissNo ratings yet

- 14 - Tax Planning Under Income Tax LawsDocument35 pages14 - Tax Planning Under Income Tax Lawsrohanfyaz00No ratings yet

- Short Tax Return For Individuals: Section ADocument8 pagesShort Tax Return For Individuals: Section Ajohndsmith22No ratings yet

- Payroll Activity SummaryDocument1 pagePayroll Activity SummaryChoo Li ZiNo ratings yet

- Child Support Scheme ExplainedDocument26 pagesChild Support Scheme ExplainedMustafa KamalNo ratings yet

- Taxation Law BasicsDocument9 pagesTaxation Law BasicsABHIJEETNo ratings yet

- Difference Between Tax and FeeDocument4 pagesDifference Between Tax and FeeAbhay KushwahaNo ratings yet

- Sri Ganesh TradersDocument1 pageSri Ganesh TradersHumera nawazNo ratings yet

- Accounting VoucherDocument1 pageAccounting Voucheradposting wNo ratings yet

- Computation 22-23Document2 pagesComputation 22-23Ruloans VaishaliNo ratings yet

- Chapter 27 Sales Interstate Exempted EntryDocument3 pagesChapter 27 Sales Interstate Exempted EntryTEJA SINGHNo ratings yet

- Income Tax DeclarationDocument2 pagesIncome Tax Declarationpedia cardioNo ratings yet

- CashDocument3 pagesCashDahirNo ratings yet

- Consumer MathDocument60 pagesConsumer MathJazz100% (3)

- EY Doing Business Slipsheet Booklet 7 Sept 2015Document32 pagesEY Doing Business Slipsheet Booklet 7 Sept 2015davidwijaya1986No ratings yet

- Corporate Tax Planning and Savings Strategies in 39 CharactersDocument28 pagesCorporate Tax Planning and Savings Strategies in 39 CharactersDivyaNo ratings yet

- Proforma - 121093Document1 pageProforma - 121093rudramaafia770No ratings yet

- CFAS Assignment - Direct & Indirect SOCFDocument1 pageCFAS Assignment - Direct & Indirect SOCFlheamaecayabyab4No ratings yet

- City of Manila Vs ColetDocument3 pagesCity of Manila Vs ColetErika ColladoNo ratings yet

- Government of India Receipt Budget 2022-23Document81 pagesGovernment of India Receipt Budget 2022-23Shubham JhaNo ratings yet

- 14 Employee Benefits That Are Tax-ExemptDocument4 pages14 Employee Benefits That Are Tax-ExemptLuke RobinsonNo ratings yet

- Business Tax Chapter 3 ReviewerDocument3 pagesBusiness Tax Chapter 3 ReviewerMurien LimNo ratings yet

- The Wealth-Tax Act, 1957Document16 pagesThe Wealth-Tax Act, 1957abhishek_ruiaNo ratings yet

- CH 14Document16 pagesCH 14Pilly PhamNo ratings yet

- Release NotesDocument13 pagesRelease NotesJbNo ratings yet

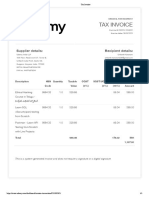

- Udhemy CourcesDocument1 pageUdhemy CourcesRam Sri100% (1)

- Cpar 2016Document6 pagesCpar 2016Rosemarie Miano TrabucoNo ratings yet

- Tempe Ordinance South PierDocument2 pagesTempe Ordinance South PierKTARNo ratings yet