You might also like

- You’Re a Business Owner, Not a Dummy!: Understand Your Merchant AccountFrom EverandYou’Re a Business Owner, Not a Dummy!: Understand Your Merchant AccountRating: 2 out of 5 stars2/5 (1)

- Important Terms and Conditions: To Get The Complete Version, Please Visit WWW - Hsbc.co - inDocument10 pagesImportant Terms and Conditions: To Get The Complete Version, Please Visit WWW - Hsbc.co - inDeepak GuptaNo ratings yet

- Mitc RupifiDocument13 pagesMitc RupifiKARTHIKEYAN K.DNo ratings yet

- 2018 FRM CandidateGuideDocument14 pages2018 FRM CandidateGuideSagar SuriNo ratings yet

- SuperCard MITC PDFDocument47 pagesSuperCard MITC PDFPrudhvi RajNo ratings yet

- SUPERCARD Most Important Terms and Conditions (MITC)Document14 pagesSUPERCARD Most Important Terms and Conditions (MITC)Diwana Hai dilNo ratings yet

- CC Common MITCDocument6 pagesCC Common MITCSharadNo ratings yet

- NW SIBDocument5 pagesNW SIBLoesh WaranNo ratings yet

- Sosc Ver 210313Document3 pagesSosc Ver 210313Shashank AgarwalNo ratings yet

- Citibank Credit CardDocument6 pagesCitibank Credit CardgjvoraNo ratings yet

- PDS Revision Eng & BM Online (Final)Document6 pagesPDS Revision Eng & BM Online (Final)Faiziya BanuNo ratings yet

- Citi Rewards Domestic MITC FinalDocument8 pagesCiti Rewards Domestic MITC FinalGauravkNo ratings yet

- CC Common MitcDocument6 pagesCC Common Mitcsandhyakasturi123No ratings yet

- Most Important Terms & ConditionsDocument93 pagesMost Important Terms & Conditionslancy_dsuzaNo ratings yet

- Most Important Terms and ConditionsDocument5 pagesMost Important Terms and ConditionsaavisNo ratings yet

- Citi Banks Credit NormsDocument6 pagesCiti Banks Credit NormsAshutosh TripathiNo ratings yet

- CUB Credit Card T&CDocument7 pagesCUB Credit Card T&CPushpa RajNo ratings yet

- Bank of India (Card Products Department) Most Important Terms and Conditions (Mitcs)Document16 pagesBank of India (Card Products Department) Most Important Terms and Conditions (Mitcs)Arun CHNo ratings yet

- Citi Rewards Card ChargesDocument7 pagesCiti Rewards Card ChargesLokesh SuranaNo ratings yet

- Most Important Terms & Conditions: 1. Fees and Charges A. Fees Payable On The Credit Card by The CardmemberDocument6 pagesMost Important Terms & Conditions: 1. Fees and Charges A. Fees Payable On The Credit Card by The Cardmembermoives pointNo ratings yet

- Most Important Terms and Conditions - Citi Rewards Credit CardDocument8 pagesMost Important Terms and Conditions - Citi Rewards Credit CardneverNo ratings yet

- Most Important Terms & ConditionsDocument6 pagesMost Important Terms & ConditionsshanmarsNo ratings yet

- Yesbank Credit Cards Terms and ConditionsDocument32 pagesYesbank Credit Cards Terms and ConditionsGiri PrasathNo ratings yet

- Most Important Terms and ConditionsDocument7 pagesMost Important Terms and ConditionsSignupNo ratings yet

- CC Common MITCDocument6 pagesCC Common MITCRamarao ChNo ratings yet

- Product Disclosure Sheet: What Is This Product About?Document6 pagesProduct Disclosure Sheet: What Is This Product About?faisal_ahsan7919No ratings yet

- Yes Bank Mitc Byoc PDFDocument13 pagesYes Bank Mitc Byoc PDFHarinder SinghNo ratings yet

- Citi Rewards Card ChargesDocument8 pagesCiti Rewards Card ChargesHem Pushp MittalNo ratings yet

- MITC Paytm First Card 2019Document7 pagesMITC Paytm First Card 2019viwaNo ratings yet

- HCBC CC InfoDocument5 pagesHCBC CC Infooninx26No ratings yet

- So A 900920160610Document1 pageSo A 900920160610Francisco Oringo Sr ESNo ratings yet

- PremierMiles Terms and ConditionsDocument7 pagesPremierMiles Terms and ConditionsAnamika purohitNo ratings yet

- Citi Rewards Card ChargesDocument7 pagesCiti Rewards Card ChargesDivya NaikNo ratings yet

- Most Important Terms and ConditionsDocument8 pagesMost Important Terms and ConditionsTHIMMAPPA KODAVATINo ratings yet

- Most Important Terms & ConditionsDocument75 pagesMost Important Terms & Conditionsjamin2020No ratings yet

- PNB MITC ConditionsDocument38 pagesPNB MITC Conditionswestm4248No ratings yet

- Most Important Terms and Conditions: As On The Date of Levy of The ChargeDocument7 pagesMost Important Terms and Conditions: As On The Date of Levy of The ChargeMohammed Tabrez ulla KhanNo ratings yet

- Most Important Terms and ConditionsDocument20 pagesMost Important Terms and Conditionsdharmendra palNo ratings yet

- Citibank - CREDITCARD CONDITIONSDocument8 pagesCitibank - CREDITCARD CONDITIONSkrishna_1238No ratings yet

- Outstanding To EMIDocument3 pagesOutstanding To EMIIobNo ratings yet

- Most Important Terms & Conditions: 1. Fees and Charges A. Fees Payable On The Credit Card by The CardmemberDocument6 pagesMost Important Terms & Conditions: 1. Fees and Charges A. Fees Payable On The Credit Card by The CardmembermanojNo ratings yet

- HBL - Updated Charges Wef From 1-Jan-2018Document3 pagesHBL - Updated Charges Wef From 1-Jan-2018Mubin AshrafNo ratings yet

- Balance Conv TandCs Final 1Document12 pagesBalance Conv TandCs Final 1kannankadirveluNo ratings yet

- Yes Private Credit Card MITC PDFDocument8 pagesYes Private Credit Card MITC PDFkiran saiNo ratings yet

- Mitc 8271022000045Document6 pagesMitc 8271022000045Kumar KumarNo ratings yet

- Cash Lite Pds enDocument7 pagesCash Lite Pds enSyarmimi LiyanaNo ratings yet

- Mitc For Amazon Pay Credit CardDocument7 pagesMitc For Amazon Pay Credit Cardsomeonestupid19690% (1)

- Bajaj Tiger CC MITC NewDocument12 pagesBajaj Tiger CC MITC NewMinatiNo ratings yet

- Encash TNC NEFTDocument10 pagesEncash TNC NEFTSurajNo ratings yet

- SOC - CC MITC 2.01 - With Schedule of ChargesDocument8 pagesSOC - CC MITC 2.01 - With Schedule of Chargessyed imranNo ratings yet

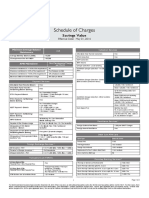

- Schedule of Charges: Savings ValueDocument2 pagesSchedule of Charges: Savings ValueNavjot SinghNo ratings yet

- Insta Loan On Card TCDocument3 pagesInsta Loan On Card TCpavanivinNo ratings yet

- Insta Loan On Card TCDocument3 pagesInsta Loan On Card TCMANIKANDAN ANANTHARAJANNo ratings yet

- Yes First Mitc Credit Cards EnglishDocument13 pagesYes First Mitc Credit Cards Englishpriyanka jagtapNo ratings yet

- October 2023Document5 pagesOctober 2023isaiahdesmondbrown1No ratings yet

- Terms & Conditions: SOC Brochure: Size (Close) 92 X 185 MMDocument6 pagesTerms & Conditions: SOC Brochure: Size (Close) 92 X 185 MMArnab Nandi100% (1)

- Citigold Account - Schedule of Charges: All Below Mentioned Benefits Are Now Free of ChargeDocument1 pageCitigold Account - Schedule of Charges: All Below Mentioned Benefits Are Now Free of ChargeNikhil RaviNo ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- Project WBS ChartDocument4 pagesProject WBS ChartMohit AroraNo ratings yet

- Revised HMEL - Bathinda Production Schedule 1Document1 pageRevised HMEL - Bathinda Production Schedule 1Mohit AroraNo ratings yet

- OD429179211415106100Document1 pageOD429179211415106100Mohit AroraNo ratings yet

- Production Capacity of Barauni Refinery: MMTPA Million Metric Tonne Per AnnumDocument1 pageProduction Capacity of Barauni Refinery: MMTPA Million Metric Tonne Per AnnumMohit AroraNo ratings yet

- Warranty Clause 14Document4 pagesWarranty Clause 14Mohit AroraNo ratings yet

- MEM No - 010 Rev-1Document30 pagesMEM No - 010 Rev-1Mohit AroraNo ratings yet

- Pipeline Engineering: BTG Program For Graduate Engineers Pipeline & City Gas DistributionDocument3 pagesPipeline Engineering: BTG Program For Graduate Engineers Pipeline & City Gas DistributionMohit AroraNo ratings yet

- Development of Tourism in Dubai Grace Chang MazzaDocument24 pagesDevelopment of Tourism in Dubai Grace Chang MazzaMohit AroraNo ratings yet

- N"",rio DL-?X: - , LR - Oc - B 'T (Lo TT", - (-,TD' ' "' A'Document9 pagesN"",rio DL-?X: - , LR - Oc - B 'T (Lo TT", - (-,TD' ' "' A'Mohit AroraNo ratings yet

- Consumer BehaviourDocument43 pagesConsumer BehaviourMohit AroraNo ratings yet

- Vis BreakingDocument12 pagesVis BreakingMohit Arora100% (1)

- Easy Guide To HSBC Credit Card Fees and ChargesDocument2 pagesEasy Guide To HSBC Credit Card Fees and ChargesboboinksNo ratings yet

- HSBCDocument91 pagesHSBCSufyan Safwan SulaimanNo ratings yet

- HSBC Vs CatalanDocument1 pageHSBC Vs CatalanJL A H-DimaculanganNo ratings yet

- HSBC MM FinalDocument15 pagesHSBC MM FinalRobinsNo ratings yet

- HSBC Hong Kong Scholarship 2014-15Document8 pagesHSBC Hong Kong Scholarship 2014-15VeniceLiNo ratings yet

- HSBC GbpusdDocument6 pagesHSBC GbpusdAnonymous UJmjrHWIhNo ratings yet

- Project of HSBC - Harish DhanjaniDocument4 pagesProject of HSBC - Harish DhanjaniArvind ChauhanNo ratings yet

- Pesonal Loan Application FormDocument36 pagesPesonal Loan Application FormmaheshNo ratings yet

- HSBC Guide To Treasury ManagementDocument308 pagesHSBC Guide To Treasury ManagementkunalwarwickNo ratings yet

- Proposal On HSBCDocument14 pagesProposal On HSBCsuhag603No ratings yet

- Delegation of Power People Vs VeraDocument2 pagesDelegation of Power People Vs VeraRuss TuazonNo ratings yet

- HSBC Bank (China) Company Limited: Who We AreDocument4 pagesHSBC Bank (China) Company Limited: Who We ArewaterleviNo ratings yet

- HSBC Death Claim FormDocument5 pagesHSBC Death Claim Form健康生活園Healthy Life GardenNo ratings yet

- This Blacklist in Cooperation With The Banks Involved and The Injured VictimsDocument5 pagesThis Blacklist in Cooperation With The Banks Involved and The Injured VictimsAndrew Rivelin50% (2)

- NEW HSBC Loan FormDocument4 pagesNEW HSBC Loan FormEdrick EstradaNo ratings yet

- Republic of The Philippines Quezon City: Court AppealsDocument38 pagesRepublic of The Philippines Quezon City: Court AppealsHerzl Hali V. HermosaNo ratings yet

- Swot hsb4cDocument10 pagesSwot hsb4chxm77No ratings yet

- Inegrated SolutionsDocument2 pagesInegrated Solutionsgkrish2No ratings yet

- Eastern Shipping Lines, Inc. vs. Court of Appeals, 190 SCRA 512, October 17, 1990Document15 pagesEastern Shipping Lines, Inc. vs. Court of Appeals, 190 SCRA 512, October 17, 1990Jeng GacalNo ratings yet

- Internship Report On E-Banking of HSBC BankDocument134 pagesInternship Report On E-Banking of HSBC BankSaquib Azam100% (2)

- HSBC vs. ShermanDocument2 pagesHSBC vs. ShermanElead Gaddiel S. AlbueroNo ratings yet

- HSBC Vs Sps Broqueza DigestDocument1 pageHSBC Vs Sps Broqueza DigestRyan Suaverdez100% (1)

- INB372.14 Yellow Group Case 2 Answer ScriptDocument3 pagesINB372.14 Yellow Group Case 2 Answer ScriptলীলাবতীNo ratings yet

- HSBC IfscDocument2 pagesHSBC Ifscharpreet0% (1)

- People v. Vera, 1937Document2 pagesPeople v. Vera, 1937LawiswisNo ratings yet

- Project Report On HSBC BankDocument35 pagesProject Report On HSBC BankNukaraju_maroju0% (1)

- Designing An Effective Training & Development Program of HSBC BankDocument26 pagesDesigning An Effective Training & Development Program of HSBC BankShahriar SakibNo ratings yet

- Customer Declaration: Each Page To Be Signed by at Least 1 Signatory As Per Mandate / Board ResolutionDocument3 pagesCustomer Declaration: Each Page To Be Signed by at Least 1 Signatory As Per Mandate / Board ResolutionShanuNo ratings yet

- HSBC Vs Sps. Bienvenido and BroquezaDocument2 pagesHSBC Vs Sps. Bienvenido and BroquezaShauna HerreraNo ratings yet

- 2019 AC Definitive IS - 0 PDFDocument362 pages2019 AC Definitive IS - 0 PDFJeanneNo ratings yet