You might also like

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- What is Financial Accounting and BookkeepingFrom EverandWhat is Financial Accounting and BookkeepingRating: 4 out of 5 stars4/5 (10)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Cheat Sheet For AccountingDocument4 pagesCheat Sheet For AccountingshihuiNo ratings yet

- Accounting Cheat SheetDocument7 pagesAccounting Cheat Sheetopty100% (15)

- Cheat Sheet Exam 1Document1 pageCheat Sheet Exam 1Shashi Gavini Keil100% (2)

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionFrom EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionRating: 5 out of 5 stars5/5 (1)

- The Portable MBA in Finance and AccountingFrom EverandThe Portable MBA in Finance and AccountingRating: 4 out of 5 stars4/5 (19)

- Accounting Cheat Sheet FinalsDocument5 pagesAccounting Cheat Sheet FinalsRahel CharikarNo ratings yet

- Inbm 110 - Accounts Study Sheet: Chapter 1 & 2Document5 pagesInbm 110 - Accounts Study Sheet: Chapter 1 & 2Laura TaiNo ratings yet

- CheatDocument1 pageCheatIshmo KueedNo ratings yet

- Accounting Cheat SheetsDocument4 pagesAccounting Cheat SheetsGreg BealNo ratings yet

- Accounting Cheat SheetDocument2 pagesAccounting Cheat Sheetanoushes1100% (2)

- ACC1002X Cheat Sheet 2Document1 pageACC1002X Cheat Sheet 2jieboNo ratings yet

- General Accounting Cheat SheetDocument35 pagesGeneral Accounting Cheat SheetZee Drake100% (5)

- ACCT 101 Cheat SheetDocument1 pageACCT 101 Cheat SheetAndrea NingNo ratings yet

- Cheat Sheet For Financial AccountingDocument1 pageCheat Sheet For Financial Accountingmikewu101No ratings yet

- Financial Accounting: Tools For Business Decision-Making, Third Canadian EditionDocument6 pagesFinancial Accounting: Tools For Business Decision-Making, Third Canadian Editionapi-19743565100% (1)

- Microeconomics Formulas & ConceptsDocument20 pagesMicroeconomics Formulas & Conceptsgavka100% (1)

- Midterm Cheat SheetDocument4 pagesMidterm Cheat SheetvikasNo ratings yet

- Target Costing & Variance AnalysisDocument1 pageTarget Costing & Variance AnalysispinkrocketNo ratings yet

- Closing Journal EntriesDocument1 pageClosing Journal EntriesMary91% (11)

- Accounting Cheat SheetDocument2 pagesAccounting Cheat SheetvgirotraNo ratings yet

- Basic Everyday Journal EntriesDocument2 pagesBasic Everyday Journal EntriesMary73% (15)

- Basic Impact of Everyday Journal Entries On The Income StatementDocument2 pagesBasic Impact of Everyday Journal Entries On The Income StatementMary100% (1)

- Account ClassificationDocument2 pagesAccount ClassificationMary96% (23)

- Classification of AccountsDocument3 pagesClassification of AccountsSaurav Aradhana100% (1)

- 5 Components COSO Framework ExplainedDocument6 pages5 Components COSO Framework ExplainedGabrielNo ratings yet

- General Accounting Cheat SheetDocument35 pagesGeneral Accounting Cheat SheetHectorNo ratings yet

- Basics of AccountingDocument20 pagesBasics of AccountingvirtualNo ratings yet

- Financial Ratio Analysis FormulasDocument4 pagesFinancial Ratio Analysis FormulasVaishali Jhaveri100% (1)

- Dividend Discount and Residual Income Models ExplainedDocument2 pagesDividend Discount and Residual Income Models ExplainedMohammad DaulehNo ratings yet

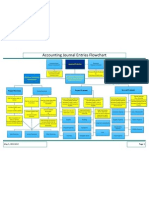

- Accounting Journal Entries Flowchart PDFDocument1 pageAccounting Journal Entries Flowchart PDFMary75% (4)

- Fnce 100 Final Cheat SheetDocument2 pagesFnce 100 Final Cheat SheetToby Arriaga100% (2)

- Finance Cheat SheetDocument2 pagesFinance Cheat SheetMarc MNo ratings yet

- Class of AccountsDocument5 pagesClass of AccountssalynnaNo ratings yet

- Accounting NotesDocument66 pagesAccounting NotesShashank Gadia71% (17)

- Journal Entries For Long Lived AssetsDocument2 pagesJournal Entries For Long Lived AssetsMary100% (20)

- Cheat Sheet Final - FMVDocument3 pagesCheat Sheet Final - FMVhanifakih100% (2)

- Financial Accounting 3Document47 pagesFinancial Accounting 3Roxana Istrate100% (1)

- Basics Accounting PrinciplesDocument22 pagesBasics Accounting PrincipleshsaherwanNo ratings yet

- BVA CheatsheetDocument3 pagesBVA CheatsheetMina ChangNo ratings yet

- General Accounting Cheat SheetDocument35 pagesGeneral Accounting Cheat Sheetazulceleste0_0100% (1)

- Managerial Accounting Mid-Term Cheat SheetDocument6 pagesManagerial Accounting Mid-Term Cheat SheetĐạt Nguyễn100% (1)

- Accounting GuideDocument153 pagesAccounting Guidebam04100% (1)

- Gross Pay CalculationsDocument2 pagesGross Pay CalculationsMary100% (3)

- End of The Year Adjustment For Allowance For Doubtful AccountsDocument1 pageEnd of The Year Adjustment For Allowance For Doubtful AccountsMary100% (1)

- Cfa Level I - Us Gaap Vs IfrsDocument4 pagesCfa Level I - Us Gaap Vs IfrsSanjay RathiNo ratings yet

- Accounting Equations and Concepts GuideDocument1 pageAccounting Equations and Concepts Guidealbatross868973No ratings yet

- The Ultimate Financial Management Cheat SheetDocument3 pagesThe Ultimate Financial Management Cheat SheethazimNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Fruits BookDocument114 pagesFruits BookMD. Monzurul Karim Shanchay100% (2)

- Diabetes and Diabetic CareDocument73 pagesDiabetes and Diabetic CareMD. Monzurul Karim Shanchay100% (1)

- The Holy AL-Quran (Bengali Translation)Document701 pagesThe Holy AL-Quran (Bengali Translation)MD. Monzurul Karim ShanchayNo ratings yet

- Best Stories of The Quran-Part 3Document244 pagesBest Stories of The Quran-Part 3MD. Monzurul Karim Shanchay100% (1)

- I Love You, O Beloved ProphetDocument123 pagesI Love You, O Beloved ProphetMD. Monzurul Karim ShanchayNo ratings yet

- The Treasures of Good DeedsDocument24 pagesThe Treasures of Good DeedsMD. Monzurul Karim Shanchay100% (1)

- Women's Hadith CompilationDocument233 pagesWomen's Hadith CompilationMD. Monzurul Karim Shanchay100% (1)

- Living History by Hillary Rodham ClintonDocument303 pagesLiving History by Hillary Rodham ClintonMD. Monzurul Karim ShanchayNo ratings yet

- Islam & ArtDocument108 pagesIslam & ArtMD. Monzurul Karim ShanchayNo ratings yet

- Having A BabyDocument172 pagesHaving A BabyMD. Monzurul Karim Shanchay100% (1)

- Best Stories of The Quran-Part 2Document239 pagesBest Stories of The Quran-Part 2MD. Monzurul Karim Shanchay100% (2)

- Best Stories of The Quran-Part 1Document238 pagesBest Stories of The Quran-Part 1MD. Monzurul Karim Shanchay100% (1)

- Beloved Prophet Muhammad (Peace Be Upon Him)Document297 pagesBeloved Prophet Muhammad (Peace Be Upon Him)MD. Monzurul Karim Shanchay100% (1)

- Prayer RulingDocument130 pagesPrayer RulingMD. Monzurul Karim ShanchayNo ratings yet

- Regular Irregularities-Hanif SanketDocument75 pagesRegular Irregularities-Hanif SanketMD. Monzurul Karim ShanchayNo ratings yet

- News Writting and Editing-Sikandar FayezDocument190 pagesNews Writting and Editing-Sikandar FayezMD. Monzurul Karim ShanchayNo ratings yet

- Mirza Galib's PoetryDocument93 pagesMirza Galib's PoetryMD. Monzurul Karim ShanchayNo ratings yet

- Short Disclosure Language Bengali GrammarDocument379 pagesShort Disclosure Language Bengali GrammarMD. Monzurul Karim ShanchayNo ratings yet

- I Am Mine-Uttom KumarDocument263 pagesI Am Mine-Uttom KumarMD. Monzurul Karim ShanchayNo ratings yet

- Entire Travel-Humayun AhmedDocument360 pagesEntire Travel-Humayun AhmedMD. Monzurul Karim Shanchay100% (1)

- Bengali Grammar-Exam. PreparationDocument43 pagesBengali Grammar-Exam. PreparationMD. Monzurul Karim Shanchay100% (2)

- Bengali Grammar by Jyotibhusan ChakiDocument309 pagesBengali Grammar by Jyotibhusan ChakiMD. Monzurul Karim Shanchay100% (1)

- God Really ExistsDocument71 pagesGod Really ExistsMD. Monzurul Karim Shanchay100% (1)

- Book of Facts by Isaac AsimovDocument158 pagesBook of Facts by Isaac AsimovMD. Monzurul Karim ShanchayNo ratings yet

- Respected CapitalDocument72 pagesRespected CapitalMD. Monzurul Karim ShanchayNo ratings yet

- Modern Islamic NamesDocument43 pagesModern Islamic NamesMD. Monzurul Karim Shanchay100% (1)

- Sustho Deho Prashanto MonDocument210 pagesSustho Deho Prashanto MonmamunngsNo ratings yet

- The Correct Procedure of PrayersDocument257 pagesThe Correct Procedure of PrayersMD. Monzurul Karim ShanchayNo ratings yet

- Learning The Holy AL-QuranDocument128 pagesLearning The Holy AL-QuranMD. Monzurul Karim ShanchayNo ratings yet

- Lecture Notes 2 Formation of A PartnershipDocument14 pagesLecture Notes 2 Formation of A PartnershipMegapoplocker MegapoplockerNo ratings yet

- Depreciation Expense, Rp. 25.000.000Document12 pagesDepreciation Expense, Rp. 25.000.000Roni SinagaNo ratings yet

- BAO6504 Lecture 2, 2014Document20 pagesBAO6504 Lecture 2, 2014LindaLindyNo ratings yet

- Fundamentals of Accountancy, Business & Management 2 Chapter 3 AssessmentDocument4 pagesFundamentals of Accountancy, Business & Management 2 Chapter 3 AssessmentKie Magracia BustillosNo ratings yet

- W4 C04 Completing The Accounting CycleDocument45 pagesW4 C04 Completing The Accounting CycleVân Anh NguyễnNo ratings yet

- ULOa Let's Analyze Week 8 9Document2 pagesULOa Let's Analyze Week 8 9emem resuentoNo ratings yet

- Module 17 - ReceivablesDocument8 pagesModule 17 - ReceivablesLuiNo ratings yet

- Module 4Document67 pagesModule 4Chicos tacos100% (3)

- CaseDocument11 pagesCasengogiahuy12082002No ratings yet

- Accounting Cycle - MALAYA KA NA COMPANYDocument7 pagesAccounting Cycle - MALAYA KA NA COMPANYkrisllyuyuyNo ratings yet

- Isc-Xii Debk Model Test PapersDocument160 pagesIsc-Xii Debk Model Test PapersRahul PareekNo ratings yet

- Theoretical Failure of IAS 41Document5 pagesTheoretical Failure of IAS 41Tosin YusufNo ratings yet

- 04 Accounts Receivable (Student) - 1Document24 pages04 Accounts Receivable (Student) - 1Christina DulayNo ratings yet

- Gillette Pakistan Quarterly ReportDocument15 pagesGillette Pakistan Quarterly Reportfaiq mallickNo ratings yet

- MACYS V JCP Company AnalysisDocument16 pagesMACYS V JCP Company AnalysisabrahamrejaNo ratings yet

- Financial Acct2 2nd Edition Godwin Test BankDocument63 pagesFinancial Acct2 2nd Edition Godwin Test Bankaramaismablative2ck3100% (20)

- MCOM - Ac - Paper - IDocument542 pagesMCOM - Ac - Paper - IKaran BindraNo ratings yet

- MARASIGAN LAPTOP REPAIR SHOP TRIAL BALANCEDocument7 pagesMARASIGAN LAPTOP REPAIR SHOP TRIAL BALANCEchezyl cadinongNo ratings yet

- Partnership (Dayag) : Advanced Acctg. IDocument33 pagesPartnership (Dayag) : Advanced Acctg. IJanysse Calderon100% (1)

- Notes Fa1Document20 pagesNotes Fa1som_tiwariNo ratings yet

- CH 1 Consolidation (SOFP)Document25 pagesCH 1 Consolidation (SOFP)ranashafaataliNo ratings yet

- TUGAS DOSEN Chapter 5Document15 pagesTUGAS DOSEN Chapter 5novita sariNo ratings yet

- Advanced Financial Accounting ExamDocument12 pagesAdvanced Financial Accounting ExamCyrene Joy RamaNo ratings yet

- COMM 111 Intro to Financial AccountingDocument21 pagesCOMM 111 Intro to Financial AccountingHenry TianNo ratings yet

- Accrual and PrepaymentDocument6 pagesAccrual and PrepaymentRia Athirah100% (1)

- Gym FinancialsDocument21 pagesGym FinancialsZahed AliNo ratings yet

- Dividend and BondsDocument3 pagesDividend and BondsJanuary Ann Bete100% (1)

- CFI FMVA Final Assessment Case Study 1ADocument12 pagesCFI FMVA Final Assessment Case Study 1Apadre pio kone100% (1)

- APC Ch6solDocument22 pagesAPC Ch6solAnonymous LusWvy100% (8)

- Chapter 4-Exercise SetDocument10 pagesChapter 4-Exercise SetNatalie JimenezNo ratings yet