You might also like

- Management of Non Performing Assests in Tiruchirapalli District Central Co-Operative Bank LTDDocument6 pagesManagement of Non Performing Assests in Tiruchirapalli District Central Co-Operative Bank LTDYadunandan NandaNo ratings yet

- It IsinDocument1 pageIt IsinRajat ChawlaNo ratings yet

- It IsinDocument1 pageIt IsinRajat ChawlaNo ratings yet

- Document (7) SbiDocument16 pagesDocument (7) Sbiyash wankhadeNo ratings yet

- Small Scale Industries' PerceptionDocument14 pagesSmall Scale Industries' PerceptionBraja kumbharNo ratings yet

- Status of MF ArticleDocument8 pagesStatus of MF ArticleajitbansalNo ratings yet

- Credit Deposit Ratio in MizoramDocument4 pagesCredit Deposit Ratio in MizoramZonun TluangaNo ratings yet

- Agricultural Credit in Pakistan: Constraints and OptionsDocument3 pagesAgricultural Credit in Pakistan: Constraints and OptionsSameen HussainNo ratings yet

- 3.1 Assessment of The Position of Credit Inclusion in India and Benchmarking Vis-À-Vis The Global PositionDocument1 page3.1 Assessment of The Position of Credit Inclusion in India and Benchmarking Vis-À-Vis The Global PositionRajat ChawlaNo ratings yet

- Interest Free Micro Finance As An Alternative Way For Financial InclusionDocument15 pagesInterest Free Micro Finance As An Alternative Way For Financial InclusionMuhammed K PalathNo ratings yet

- Sbi Customers Perception On CRM: A Study: M. Malla Reddy A. SureshDocument11 pagesSbi Customers Perception On CRM: A Study: M. Malla Reddy A. SureshPooja Singh SolankiNo ratings yet

- Dr. B. S. Navi : Impact of Regional Rural Banks On Rural Farmers - A Case Study of Belgaum DistrictDocument9 pagesDr. B. S. Navi : Impact of Regional Rural Banks On Rural Farmers - A Case Study of Belgaum DistrictvelmuruganNo ratings yet

- Micro Finance - Policy InitiativesDocument12 pagesMicro Finance - Policy Initiativesshashankr_1No ratings yet

- 52 Ijasrapr201752Document8 pages52 Ijasrapr201752TJPRC PublicationsNo ratings yet

- An Overview of Microfinance Service Practices in Nepal: Puspa Raj Sharma, PHDDocument16 pagesAn Overview of Microfinance Service Practices in Nepal: Puspa Raj Sharma, PHDRamdeo YadavNo ratings yet

- Project On Retail Assets of BOB OkDocument76 pagesProject On Retail Assets of BOB OkKanchan100% (1)

- Evaluating Kisan Credit Card Scheme's ImpactDocument52 pagesEvaluating Kisan Credit Card Scheme's ImpactGaurav DeshmukhNo ratings yet

- International Journal of Information Technology and Knowledge ManagementDocument6 pagesInternational Journal of Information Technology and Knowledge Managementrakeshkmr1186No ratings yet

- Samachar Lehar March 2012 IssueDocument198 pagesSamachar Lehar March 2012 IssueSanjay KumarNo ratings yet

- Agricultural Loan Satisfaction Study of Kerala Gramin Bank CustomersDocument7 pagesAgricultural Loan Satisfaction Study of Kerala Gramin Bank Customerskrishnatradingcompany udtNo ratings yet

- Ms. Pallavi Gupta Dr. Chhaya Mangal Mishra Dr. Tazyn RahmanDocument8 pagesMs. Pallavi Gupta Dr. Chhaya Mangal Mishra Dr. Tazyn RahmanKanika TandonNo ratings yet

- Name: B. Sai Chetan ROLL NO: 16311E0049 Branch/Year: Mba I YearDocument28 pagesName: B. Sai Chetan ROLL NO: 16311E0049 Branch/Year: Mba I YearFKNo ratings yet

- Sustainability and Poverty Outreach in Microfinance: the Sri Lankan Experience: To Resolve Dilemmas of Microfinance Practitioners and Policy MakersFrom EverandSustainability and Poverty Outreach in Microfinance: the Sri Lankan Experience: To Resolve Dilemmas of Microfinance Practitioners and Policy MakersNo ratings yet

- Customers' Attitude Towards Debit Cards - A StudyDocument4 pagesCustomers' Attitude Towards Debit Cards - A StudyViswa KeerthiNo ratings yet

- Yspthorat: 1 Managing Director, NABARDDocument26 pagesYspthorat: 1 Managing Director, NABARDManan RajpuraNo ratings yet

- Rural Credit: A Source of Sustainable Livelihood of Rural IndiaDocument16 pagesRural Credit: A Source of Sustainable Livelihood of Rural IndiaJitendra RaghuwanshiNo ratings yet

- VinuDocument7 pagesVinuvineet89No ratings yet

- Anu.T.Philip,: Customer Perception On Banking Services - A Study Among Public Sector and Private Sector BanksDocument14 pagesAnu.T.Philip,: Customer Perception On Banking Services - A Study Among Public Sector and Private Sector BankstawandaNo ratings yet

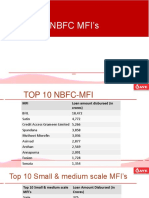

- Top 10 NBFC MFIs and their loan disbursement amountsDocument10 pagesTop 10 NBFC MFIs and their loan disbursement amountsNeeraj KumarNo ratings yet

- Final MRP ReportDocument58 pagesFinal MRP ReportMitali SenNo ratings yet

- Non-Performing Assets: A Study of State Bank of India: Dr.D.Ganesan R.SanthanakrishnanDocument8 pagesNon-Performing Assets: A Study of State Bank of India: Dr.D.Ganesan R.SanthanakrishnansusheelNo ratings yet

- Gap analysis of retail banking strategies of a nationalized bank from customer perspectivesDocument18 pagesGap analysis of retail banking strategies of a nationalized bank from customer perspectivesmanoj kumar DasNo ratings yet

- Analysis N DiscussionDocument16 pagesAnalysis N DiscussionjaikiNo ratings yet

- Banking Sector Liberalization in IndiaDocument4 pagesBanking Sector Liberalization in IndiabbasyNo ratings yet

- Analysis of Priority and Non-Priority Sector Npas of Indian Public Sectors BanksDocument6 pagesAnalysis of Priority and Non-Priority Sector Npas of Indian Public Sectors BanksAnshuman RoutNo ratings yet

- How India Lends Fy2023Document68 pagesHow India Lends Fy2023prajwaln876No ratings yet

- June_2015_1432983331__107 (1)Document4 pagesJune_2015_1432983331__107 (1)BARATH SHARMANo ratings yet

- A Study On Farmers Perception Towards Agricultural Loans in Rural Areas With Reference To Rayalaseema Region, Andhra PradeshDocument11 pagesA Study On Farmers Perception Towards Agricultural Loans in Rural Areas With Reference To Rayalaseema Region, Andhra PradeshIAEME PublicationNo ratings yet

- Ô Ô !"" #$% A % A & ' % A # ADocument11 pagesÔ Ô !"" #$% A % A & ' % A # ADiane RodriguesNo ratings yet

- Impact of Private Sector Banks On Public Sector BanksDocument248 pagesImpact of Private Sector Banks On Public Sector Banksjalender7No ratings yet

- Blessing Et Al Credit Demand PaperDocument10 pagesBlessing Et Al Credit Demand PaperDr Ezekia SvotwaNo ratings yet

- Customers' Perceptions Towards E-Banking Services - A Study of Select Public Sector Banks in Rayalaseema Region of Andhra PradeshDocument11 pagesCustomers' Perceptions Towards E-Banking Services - A Study of Select Public Sector Banks in Rayalaseema Region of Andhra Pradesharcherselevators100% (1)

- Findings, Suggessions and ConclusionDocument14 pagesFindings, Suggessions and ConclusionNishan DattaNo ratings yet

- Impact of Microfinance On Income Generation and Living Standards A Case Study of Dera Ghazi Khan DivisionDocument8 pagesImpact of Microfinance On Income Generation and Living Standards A Case Study of Dera Ghazi Khan DivisionDia MalikNo ratings yet

- MUDRADocument7 pagesMUDRAdjamitbravoNo ratings yet

- A Research Proposal On Influence of Banks' Demands For Security On Percentage of Loan Sanctioned For Farmers Under: Service Area Approach (SAA) IndiaDocument10 pagesA Research Proposal On Influence of Banks' Demands For Security On Percentage of Loan Sanctioned For Farmers Under: Service Area Approach (SAA) IndiaSamarpit MathurNo ratings yet

- BFP-B Policy Study Mobile Financial ServicesDocument103 pagesBFP-B Policy Study Mobile Financial ServicesArif Khan NabilNo ratings yet

- Out-Reach and Impact of TheDocument5 pagesOut-Reach and Impact of TheYaronBabaNo ratings yet

- Non Performing Loans ThesisDocument8 pagesNon Performing Loans Thesisggzgpeikd100% (2)

- The Effect of Consumer Loans On Public Sector Employees in West Bank Using Elsi Short FormDocument24 pagesThe Effect of Consumer Loans On Public Sector Employees in West Bank Using Elsi Short FormGwyneth Mae GallardoNo ratings yet

- NPA of Jammu and Kashmir BankDocument22 pagesNPA of Jammu and Kashmir BankE-sabat RizviNo ratings yet

- Findings, Suggestions and ConclusionDocument14 pagesFindings, Suggestions and ConclusionKrishnanu KarNo ratings yet

- A Critical Study On Non Performing Assets of Microfinance Institutions in India (With Special Reference To Pre and Post Covid-19)Document7 pagesA Critical Study On Non Performing Assets of Microfinance Institutions in India (With Special Reference To Pre and Post Covid-19)Palak ParakhNo ratings yet

- Perceptions On Banking Service in Rural India An EDocument21 pagesPerceptions On Banking Service in Rural India An EanilNo ratings yet

- American Journal of Engineering Research (AJER) : e-ISSN: 2320-0847 p-ISSN: 2320-0936 Volume-4, Issue-7, pp-170-175Document6 pagesAmerican Journal of Engineering Research (AJER) : e-ISSN: 2320-0847 p-ISSN: 2320-0936 Volume-4, Issue-7, pp-170-175AJER JOURNALNo ratings yet

- Analyzing impacts and outreach of microcredit in Borno StateDocument3 pagesAnalyzing impacts and outreach of microcredit in Borno StateYaronBabaNo ratings yet

- 4.micro Finance & Social InclusionDocument27 pages4.micro Finance & Social InclusionSaurabh SinghNo ratings yet

- Role of RBI in Funding Agricultural DevelopmentDocument13 pagesRole of RBI in Funding Agricultural DevelopmentAmrit Kajava100% (2)

- An Analysis of The Recruitment Methodology of Sales Officers in A Private BankDocument56 pagesAn Analysis of The Recruitment Methodology of Sales Officers in A Private BankAnsari SufiyanNo ratings yet

- Chanda 2012 Working Paper2Document53 pagesChanda 2012 Working Paper2Guga PrasadNo ratings yet

- Different Sources of Finance To PLCDocument12 pagesDifferent Sources of Finance To PLCAsif AbdullaNo ratings yet

- Prototype Memorandum and Articles of A Microfinance BankDocument18 pagesPrototype Memorandum and Articles of A Microfinance BankDenis Koech67% (3)

- Integrate Physical and Financial Supply ChainsDocument8 pagesIntegrate Physical and Financial Supply Chainsishan19No ratings yet

- Changing Structure of Appropriations in Vedda Agriculture - James BrowDocument20 pagesChanging Structure of Appropriations in Vedda Agriculture - James BrowGirawa KandaNo ratings yet

- Profitability NPL Analysis of United Commercial BankDocument12 pagesProfitability NPL Analysis of United Commercial BankImtiaz Mahmud EmuNo ratings yet

- MFI Audit Course Manual1Document39 pagesMFI Audit Course Manual1Amandeep SinghNo ratings yet

- LO4194 PayrollDocument431 pagesLO4194 Payrollhammad016No ratings yet

- Trinidad and Tobago Passes New Insurance ActDocument333 pagesTrinidad and Tobago Passes New Insurance ActSarahNo ratings yet

- Bài kiểm tra trắc nghiệm tổng hợp các chủ đề - Xem lại bài làmDocument22 pagesBài kiểm tra trắc nghiệm tổng hợp các chủ đề - Xem lại bài làmAh TuanNo ratings yet

- G.R. No. L-46158 - Tayug Vs Central Bank - Administrative Rules and Regulations (Digest)Document14 pagesG.R. No. L-46158 - Tayug Vs Central Bank - Administrative Rules and Regulations (Digest)Apoi FaminianoNo ratings yet

- CH2 The FSDocument13 pagesCH2 The FSPatrisha Georgia AmitenNo ratings yet

- Secrecy of Bank Deposits Notes - 2Document12 pagesSecrecy of Bank Deposits Notes - 2Lica CiprianoNo ratings yet

- Lecture # 2 (Non-Traditional Project Delivery Method)Document35 pagesLecture # 2 (Non-Traditional Project Delivery Method)Usama EjazNo ratings yet

- ICICI Bank AGM Notice 2019Document363 pagesICICI Bank AGM Notice 2019Sadiq SayaniNo ratings yet

- Vornado Realty Trust 2016 Annual ReportDocument216 pagesVornado Realty Trust 2016 Annual ReportsuedtNo ratings yet

- Vice President Director Finance in Philadelphia PA Resume Nino ToscanoDocument2 pagesVice President Director Finance in Philadelphia PA Resume Nino ToscanoNinoToscanoNo ratings yet

- Angel Warehousing vs. Cheldea 23 SCRA 19 (1968)Document3 pagesAngel Warehousing vs. Cheldea 23 SCRA 19 (1968)Fides DamascoNo ratings yet

- StatconDocument299 pagesStatconruben diwasNo ratings yet

- WP Content Uploads FHA Waterfall Worksheet Users GuideDocument46 pagesWP Content Uploads FHA Waterfall Worksheet Users GuideKathy Westbrooke Powell-WadeNo ratings yet

- Subject: Idt: PROJECT ON: Export-Import Bank of India - Role, Functions and FacilitiesDocument23 pagesSubject: Idt: PROJECT ON: Export-Import Bank of India - Role, Functions and FacilitiesSachin PatelNo ratings yet

- G.R. No. 189871 August 13, 2013Document6 pagesG.R. No. 189871 August 13, 2013Josephine BercesNo ratings yet

- Fundamental Analysis of Banking SectorDocument54 pagesFundamental Analysis of Banking SectorZui Mhatre100% (1)

- Creation of Series Using List, Dictionary & NdarrayDocument65 pagesCreation of Series Using List, Dictionary & Ndarrayrizwana fathimaNo ratings yet

- Test Bank - Problems and Essays 2008Document148 pagesTest Bank - Problems and Essays 2008okkie50% (6)

- Laws Guiding Government Assistance and Ethics in Private EducationDocument32 pagesLaws Guiding Government Assistance and Ethics in Private EducationMaria ElizaNo ratings yet

- DOCTRINE: The Court Refuses To Allow The Execution of A Corporate Judgment DebtDocument22 pagesDOCTRINE: The Court Refuses To Allow The Execution of A Corporate Judgment DebtBernalyn Domingo AlcanarNo ratings yet

- 2021年政府工作报告发(中英双语对照)Document60 pages2021年政府工作报告发(中英双语对照)tian xuNo ratings yet

- Meezan BankDocument56 pagesMeezan BankKhurram ShahzadNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- Sss Loan Form 2013Document3 pagesSss Loan Form 2013John Carlo M. SamaritaNo ratings yet