You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Indian Bank Probationary Officer PO Previous Paper 2015 Download PDF 10.10.2016 PDFDocument49 pagesIndian Bank Probationary Officer PO Previous Paper 2015 Download PDF 10.10.2016 PDFAlpna PatelNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Indian Bank Probationary Officer PO Previous Year Paper 2015 Download PDFDocument45 pagesIndian Bank Probationary Officer PO Previous Year Paper 2015 Download PDFAlpna PatelNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Chapter 3: Retail Banking in India-An OverviewDocument26 pagesChapter 3: Retail Banking in India-An OverviewSanaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Bos 25030 CP 2Document24 pagesBos 25030 CP 2Alpna PatelNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Role of Central BankDocument32 pagesRole of Central BankAsadul Hoque100% (3)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Guanxi - Group 7Document7 pagesGuanxi - Group 7Alpna PatelNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- 27585ipcc Acc Vol1 Chapter-IpagesDocument18 pages27585ipcc Acc Vol1 Chapter-IpagesAlpna PatelNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Analogy: Option: A. Na B. Tok C. Tim D. PitDocument4 pagesAnalogy: Option: A. Na B. Tok C. Tim D. PitAlpna PatelNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Ratio AnalysisDocument6 pagesRatio AnalysisAlpna PatelNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- BRKRST 2558Document98 pagesBRKRST 2558boythanhdatNo ratings yet

- Please Refer To Our Contract of CarriageDocument11 pagesPlease Refer To Our Contract of CarriagekarinaNo ratings yet

- Prime Web Brochure PDFDocument14 pagesPrime Web Brochure PDFDnyaneshwar ChincholikarNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Airbnb's CRM Implementation and Customer-Facing ProcessesDocument9 pagesAirbnb's CRM Implementation and Customer-Facing Processesrohit nilawarNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Karthick Kumar Project - 7878Document109 pagesKarthick Kumar Project - 7878Karthick KumarNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Kamakoti FebDocument164 pagesKamakoti FebClaudia ShanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Nilson Report Issue 1175 - 0036Document10 pagesNilson Report Issue 1175 - 0036John MulderNo ratings yet

- Republic o F The Philippines Department o F Social Welfare and DevelopmentDocument6 pagesRepublic o F The Philippines Department o F Social Welfare and DevelopmentJasmin Mingo CalaNo ratings yet

- G6C2PDocument46 pagesG6C2PJian MeixinNo ratings yet

- Retail Multichannel Unit 2Document26 pagesRetail Multichannel Unit 2Nikita ShekhawatNo ratings yet

- JS2 Computer Studies Examination (Third Term)Document2 pagesJS2 Computer Studies Examination (Third Term)Ejiro Ndifereke100% (4)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Benefits ListDocument9 pagesBenefits Listapi-354681687No ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Logistics vs. Supply Chain ManagementDocument23 pagesLogistics vs. Supply Chain ManagementÁnh NguyễnNo ratings yet

- Financial Reporting and AnalysisDocument50 pagesFinancial Reporting and AnalysisGeorge Shevtsov83% (6)

- APPS Rating and ReviewsDocument83 pagesAPPS Rating and ReviewsApurbh Singh KashyapNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- AP - Cash in VaultDocument14 pagesAP - Cash in VaultNorie Jane CaninoNo ratings yet

- Https WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action DoPrintDocument1 pageHttps WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action DoPrintSyed HanafieNo ratings yet

- b2c E-Commerce ReviewDocument10 pagesb2c E-Commerce ReviewadiltsaNo ratings yet

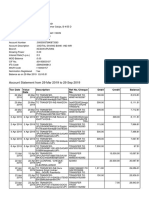

- Folio Number: 4301766 / 67: Page 1 of 2Document2 pagesFolio Number: 4301766 / 67: Page 1 of 2neelNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Page 7Document2 pagesPage 7hjhsingNo ratings yet

- Lembar Ukk Ud AbadiDocument62 pagesLembar Ukk Ud Abadibayufitriani3953% (15)

- Broker Success Issue 5Document20 pagesBroker Success Issue 5Graham ReibeltNo ratings yet

- Financial Accounting and Reporting Midterm Exam KeyDocument4 pagesFinancial Accounting and Reporting Midterm Exam KeyDonita Joy T. EugenioNo ratings yet

- Freight Broker Training ManualDocument9 pagesFreight Broker Training ManualTigranuhi MantashyanNo ratings yet

- Brochure 2023 - COMPRESSED EditedDocument5 pagesBrochure 2023 - COMPRESSED EditedCephas GathiiNo ratings yet

- Ekb OZVi JDKQ 37 Ho GDocument7 pagesEkb OZVi JDKQ 37 Ho GSahil SalujaNo ratings yet

- My ResumeDocument2 pagesMy ResumeDaramolaolabanjiNo ratings yet

- CRT Learning Module: Course Code Course Title Units Module TitleDocument21 pagesCRT Learning Module: Course Code Course Title Units Module Titlekat agustin100% (2)

- NBFC Es2020Document23 pagesNBFC Es2020Aditya GuptaNo ratings yet

- Interest Rate Individual BorrowerDocument1 pageInterest Rate Individual BorrowerSreeni ReddyNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)