You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Botswana Economy Recent Developments and ProspectsDocument60 pagesBotswana Economy Recent Developments and ProspectsmisterbeNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Furnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFDocument1 pageFurnmart Ltd. (FURNMART-BW) - Interim Report For Period End 31-Jan-2018 (English) PDFmisterbeNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Global Concrete Report 2021Document35 pagesGlobal Concrete Report 2021misterbe100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Furnmart Ltd. (FURNMART-BW) - Annual Report For Period End 31-Jul-2017 (English) PDFDocument68 pagesFurnmart Ltd. (FURNMART-BW) - Annual Report For Period End 31-Jul-2017 (English) PDFmisterbeNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- DangCem Peers ComparisonDocument15 pagesDangCem Peers ComparisonDavid HundeyinNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- ShriramCity - InvestorUpdate - June 2013Document20 pagesShriramCity - InvestorUpdate - June 2013misterbeNo ratings yet

- Corporate Presentation Highlights Shriram City GrowthDocument35 pagesCorporate Presentation Highlights Shriram City GrowthmisterbeNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- ChinaTribunal JUDGMENT 1stmarch 2020Document562 pagesChinaTribunal JUDGMENT 1stmarch 2020misterbeNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- NBFC To BANKDocument6 pagesNBFC To BANKmisterbeNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Allegiant Travel Company Forward-Looking Statements and ProjectionsDocument39 pagesAllegiant Travel Company Forward-Looking Statements and ProjectionsmisterbeNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Shriram City Union Finance Limited FY 2015 Performance ReviewDocument11 pagesShriram City Union Finance Limited FY 2015 Performance ReviewmisterbeNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- SHRIRAM CITY UNION FINANCE LIMITED PERFORMANCE REVIEW 2014Document19 pagesSHRIRAM CITY UNION FINANCE LIMITED PERFORMANCE REVIEW 2014misterbeNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Trading and Business Update: (Stock Code: 100)Document2 pagesTrading and Business Update: (Stock Code: 100)misterbeNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- 0Document86 pages0misterbeNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Tsaker Chemical Group Limited 彩 客 化 學 集 團 有 限 公 司: Positive Profit AlertDocument2 pagesTsaker Chemical Group Limited 彩 客 化 學 集 團 有 限 公 司: Positive Profit AlertmisterbeNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Upward Toiling of Our Hidden Champions - Issue 3 (Part 1) : Dear Clients and PartnersDocument5 pagesUpward Toiling of Our Hidden Champions - Issue 3 (Part 1) : Dear Clients and PartnersmisterbeNo ratings yet

- Fossil Group - in The Boat With Kosta - Ambérd CapitalDocument4 pagesFossil Group - in The Boat With Kosta - Ambérd CapitalmisterbeNo ratings yet

- Annual ReportDocument282 pagesAnnual ReportmisterbeNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Securities and Exchange Commission FORM 10-KDocument86 pagesSecurities and Exchange Commission FORM 10-KmisterbeNo ratings yet

- 2003 April Fitch AsiaDocument42 pages2003 April Fitch AsiamisterbeNo ratings yet

- SeaLink Travel Group Financial Report and Appendix 4E Year Ended 30 June 2017 PDFDocument56 pagesSeaLink Travel Group Financial Report and Appendix 4E Year Ended 30 June 2017 PDFmisterbeNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Fossil Initiating ReportDocument9 pagesFossil Initiating ReportmisterbeNo ratings yet

- Long-Value Investors Club - Fossil (FOSL)Document8 pagesLong-Value Investors Club - Fossil (FOSL)misterbeNo ratings yet

- Asia Pacific Investment UniverseDocument2 pagesAsia Pacific Investment UniversemisterbeNo ratings yet

- Luxottica Group "3Q 2016 Sales" Date: October 24, 2016Document19 pagesLuxottica Group "3Q 2016 Sales" Date: October 24, 2016misterbeNo ratings yet

- Fossil 2015 Full ARDocument132 pagesFossil 2015 Full ARmisterbeNo ratings yet

- 3Q16 Earnings PresentationDocument18 pages3Q16 Earnings PresentationmisterbeNo ratings yet

- Can Misfit Be A Good Fit - Ambérd CapitalDocument4 pagesCan Misfit Be A Good Fit - Ambérd CapitalmisterbeNo ratings yet

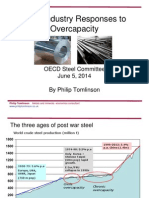

- Overcapacity - TomlinsonDocument21 pagesOvercapacity - TomlinsonmisterbeNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- PRC vs De Guzman: SC reverses CA, nullifies mandamus for physician oathDocument4 pagesPRC vs De Guzman: SC reverses CA, nullifies mandamus for physician oathJude FanilaNo ratings yet

- Weathering With You OST Grand EscapeDocument3 pagesWeathering With You OST Grand EscapeGabriel AnwarNo ratings yet

- The Ethics of Care and The Politics of EquityDocument37 pagesThe Ethics of Care and The Politics of EquityhammulukNo ratings yet

- FCE Rephrase and Word FormationDocument5 pagesFCE Rephrase and Word FormationMonicaNo ratings yet

- International Journal of Educational Development: Su Jung Choi, Jin Chul Jeong, Seoung Nam KimDocument10 pagesInternational Journal of Educational Development: Su Jung Choi, Jin Chul Jeong, Seoung Nam KimDen Yogi HardiyantoNo ratings yet

- MCVPN OvDocument25 pagesMCVPN Ovuzaheer123No ratings yet

- Hydro V NIA Case AnalysisDocument2 pagesHydro V NIA Case AnalysisClark Vincent PonlaNo ratings yet

- 518pm31.zahoor Ahmad ShahDocument8 pages518pm31.zahoor Ahmad ShahPrajwal KottawarNo ratings yet

- Gcse History Coursework ExamplesDocument4 pagesGcse History Coursework Examplesf1vijokeheg3100% (2)

- Nature of Organizational ChangeDocument18 pagesNature of Organizational ChangeRhenz Mahilum100% (1)

- Republic Vs CA and Dela RosaDocument2 pagesRepublic Vs CA and Dela RosaJL A H-Dimaculangan100% (4)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Residential Status Problems - 3Document15 pagesResidential Status Problems - 3ysrbalajiNo ratings yet

- Marpol 1 6 PPT Part 1Document110 pagesMarpol 1 6 PPT Part 1Aman GautamNo ratings yet

- Poem AnalysisDocument1 pagePoem AnalysisRosé Sanguila100% (1)

- Pernille Gerstenberg KirkebyDocument17 pagesPernille Gerstenberg KirkebymanufutureNo ratings yet

- Instrument Used To Collect Data Topic: Survey On Some Problems Single Parent Encountered in The Community of Parafaite HarmonieDocument5 pagesInstrument Used To Collect Data Topic: Survey On Some Problems Single Parent Encountered in The Community of Parafaite HarmonieDumissa MelvilleNo ratings yet

- Indian Hostile Narratives and Counter Narratives of PakistanDocument13 pagesIndian Hostile Narratives and Counter Narratives of PakistanJournals ConsultancyNo ratings yet

- The Aircraft EncyclopediaDocument196 pagesThe Aircraft Encyclopediaa h100% (11)

- Pointers-Criminal Jurisprudence/gemini Criminology Review and Training Center Subjects: Book 1, Book 2, Criminal Evidence and Criminal ProcedureDocument10 pagesPointers-Criminal Jurisprudence/gemini Criminology Review and Training Center Subjects: Book 1, Book 2, Criminal Evidence and Criminal ProcedureDivina Dugao100% (1)

- Title 5 - Tourism Demand 2021Document36 pagesTitle 5 - Tourism Demand 2021RAZIMIE BIN ASNUH -No ratings yet

- Case StudyDocument2 pagesCase StudyMicaella GalanzaNo ratings yet

- Interim Rules of Procedure Governing Intra-Corporate ControversiesDocument28 pagesInterim Rules of Procedure Governing Intra-Corporate ControversiesRoxanne C.No ratings yet

- Members AreaDocument1 pageMembers Areasipho gumbiNo ratings yet

- Sierra Gainer Resume FinalDocument2 pagesSierra Gainer Resume Finalapi-501229355No ratings yet

- Global 2Document90 pagesGlobal 2Amanu'el AdugnaNo ratings yet

- Cabbage As IntercropDocument1 pageCabbage As IntercropGrignionNo ratings yet

- 1 - Golden Bridge Investment (Z) LTD - EpbDocument90 pages1 - Golden Bridge Investment (Z) LTD - EpbMoses ziyayeNo ratings yet

- Sri Bhakti-Sandarbha 9Document20 pagesSri Bhakti-Sandarbha 9api-19975968No ratings yet

- Unit III International ArbitrageDocument14 pagesUnit III International ArbitrageanshuldceNo ratings yet

- Vs. AdazaDocument16 pagesVs. AdazawandererkyuNo ratings yet