You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- OnepagemarketingplanDocument1 pageOnepagemarketingplanJael Alejandra Torres CalderonNo ratings yet

- Euromonitor - New Emerging MarketsDocument17 pagesEuromonitor - New Emerging MarketsKG Sison100% (1)

- Euromonitor - New Emerging MarketsDocument17 pagesEuromonitor - New Emerging MarketsKG Sison100% (1)

- Cross Culture DiversityDocument61 pagesCross Culture DiversityKG SisonNo ratings yet

- By PseDocument29 pagesBy PseJa Mi LahNo ratings yet

- CHED strategic plan guides PH higher edDocument18 pagesCHED strategic plan guides PH higher edPeter Jonas DavidNo ratings yet

- Regionalanalysisofasia 140925090310 Phpapp01Document106 pagesRegionalanalysisofasia 140925090310 Phpapp01crouch88No ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- As 1683.23-2000 Methods of Test For Elastomers Rubber - Vulcanized - Determination of Resistance To LiquidsDocument8 pagesAs 1683.23-2000 Methods of Test For Elastomers Rubber - Vulcanized - Determination of Resistance To LiquidsSAI Global - APACNo ratings yet

- Gamma-Oryzanol From Rice Bran Oil - A ReviewDocument10 pagesGamma-Oryzanol From Rice Bran Oil - A ReviewAnonymous h8GtcsINo ratings yet

- GULFDocument33 pagesGULFJORDAN FREENo ratings yet

- Foundation of EnergyDocument121 pagesFoundation of Energyapi-3765936No ratings yet

- GER3620L Nov 3 09b 1Document60 pagesGER3620L Nov 3 09b 1rafieeNo ratings yet

- G3306 Gas Petroleum EnginepdfDocument4 pagesG3306 Gas Petroleum EnginepdfGustavo López CarriónNo ratings yet

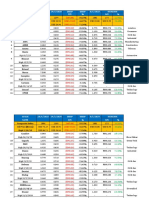

- Audit Report On The Accounts of Petroleum Division and OGRA Audit Year 2021-22Document391 pagesAudit Report On The Accounts of Petroleum Division and OGRA Audit Year 2021-22for anyNo ratings yet

- 2018 To 2020 Stock Price Drop & Price Increase On Friday 8 May 2020Document9 pages2018 To 2020 Stock Price Drop & Price Increase On Friday 8 May 2020Ahmad FadzlanNo ratings yet

- Describe The Characteristics of The Various Fractions From The Fractional Distillation of PetroleumDocument1 pageDescribe The Characteristics of The Various Fractions From The Fractional Distillation of PetroleumYew Chow ShuanNo ratings yet

- Case StudyDocument21 pagesCase StudyMuhamad Shahrizal BeraniNo ratings yet

- 41 Osmeña v. Orbos, G.R. No. 99886, March 31 1993 PDFDocument8 pages41 Osmeña v. Orbos, G.R. No. 99886, March 31 1993 PDFJeunice VillanuevaNo ratings yet

- JASO Engine Oil ListDocument9 pagesJASO Engine Oil ListMichaelNo ratings yet

- 0653 s11 QP 22 PDFDocument20 pages0653 s11 QP 22 PDFmarryNo ratings yet

- Fuels and Combustion OverviewDocument28 pagesFuels and Combustion OverviewDrupad PatelNo ratings yet

- Conference BroucherDocument8 pagesConference BroucherSoumen MahatoNo ratings yet

- Grease Analysis - Monitoring Grease ServiceabilityDocument6 pagesGrease Analysis - Monitoring Grease Serviceabilitysyuhaimi82No ratings yet

- RD TR r00024 005Document6 pagesRD TR r00024 005Rebekah SchmidtNo ratings yet

- (Magazine) Hydrocarbon Processing 01 2014Document103 pages(Magazine) Hydrocarbon Processing 01 2014Huy Văn ĐoànNo ratings yet

- Petroleum, Oil, Lubricants (POL) SafetyDocument30 pagesPetroleum, Oil, Lubricants (POL) SafetyEagle1968100% (1)

- Rough Seas On The Link560Document17 pagesRough Seas On The Link560Clarissa Paragas100% (1)

- Environmental Science - Chapter2-1Document25 pagesEnvironmental Science - Chapter2-1Mark AngeloNo ratings yet

- JW Elastomeric Seals Components For The Oil Gas Iss 10.1 2017 v1Document72 pagesJW Elastomeric Seals Components For The Oil Gas Iss 10.1 2017 v1Yogi173No ratings yet

- 033 2010 Abstracts Chemreactor 19 VienaDocument637 pages033 2010 Abstracts Chemreactor 19 VienaChau Mai100% (1)

- An Essay On Fuel Scarcity and Nigeria MassesDocument3 pagesAn Essay On Fuel Scarcity and Nigeria MassesvictorNo ratings yet

- Lancer (CY, CX) : Lubricants and FluidsDocument4 pagesLancer (CY, CX) : Lubricants and Fluidsاشرف صابرNo ratings yet

- 101 COMPUTER EMBROIDERY Garment WorkshopDocument1,414 pages101 COMPUTER EMBROIDERY Garment WorkshopharisikhanNo ratings yet

- Oil and Gas Contacts DatabaseDocument16 pagesOil and Gas Contacts DatabaseKizzy SubriNo ratings yet

- Energy Production and Consumption in EU 2013Document5 pagesEnergy Production and Consumption in EU 2013aio2No ratings yet

- Learnenglish Podcasts Professionals Emotional IntelligenceDocument20 pagesLearnenglish Podcasts Professionals Emotional IntelligenceChandrasekhar ReddyNo ratings yet

- Touch N Buy - Com SunPassDocument1 pageTouch N Buy - Com SunPassnmillan007No ratings yet