You might also like

- AFNetworkReachabilityManager HDocument4 pagesAFNetworkReachabilityManager HArindam BasuNo ratings yet

- AFNetworking HDocument1 pageAFNetworking HArindam BasuNo ratings yet

- AFHTTPSessionManager MDocument7 pagesAFHTTPSessionManager MArindam BasuNo ratings yet

- Read MeDocument4 pagesRead MeArindam BasuNo ratings yet

- ViewController MDocument1 pageViewController MArindam BasuNo ratings yet

- AFHTTPSessionManager HDocument6 pagesAFHTTPSessionManager HArindam BasuNo ratings yet

- AFHTTPRequestOperationManager HDocument8 pagesAFHTTPRequestOperationManager HArindam BasuNo ratings yet

- Info PlistDocument1 pageInfo PlistArindam BasuNo ratings yet

- AFHTTPRequestOperation HDocument2 pagesAFHTTPRequestOperation HArindam BasuNo ratings yet

- AFHTTPRequestOperationManager CodeDocument6 pagesAFHTTPRequestOperationManager CodeArindam BasuNo ratings yet

- AFHTTPRequestOperation MDocument4 pagesAFHTTPRequestOperation MArindam BasuNo ratings yet

- ListObject MDocument1 pageListObject MArindam BasuNo ratings yet

- Collinruffenach PbxuserDocument6 pagesCollinruffenach PbxuserArindam BasuNo ratings yet

- AppDelegate MDocument2 pagesAppDelegate MArindam BasuNo ratings yet

- AppDelegate MDocument2 pagesAppDelegate MArindam BasuNo ratings yet

- ELCAlbumPickerController MDocument5 pagesELCAlbumPickerController MArindam BasuNo ratings yet

- DetailsViewController MDocument9 pagesDetailsViewController MArindam BasuNo ratings yet

- iOS config file settingsDocument1 pageiOS config file settingsArindam BasuNo ratings yet

- ELCAlbumPickerController XibDocument9 pagesELCAlbumPickerController XibArindam BasuNo ratings yet

- Project PbxprojDocument9 pagesProject PbxprojArindam BasuNo ratings yet

- ELCOverlayImageView MDocument2 pagesELCOverlayImageView MArindam BasuNo ratings yet

- ELCImagePickerDemoViewController XibDocument7 pagesELCImagePickerDemoViewController XibArindam BasuNo ratings yet

- ELCImagePickerController MDocument4 pagesELCImagePickerController MArindam BasuNo ratings yet

- ELCAssetTablePicker XibDocument10 pagesELCAssetTablePicker XibArindam BasuNo ratings yet

- ELCConsole MDocument2 pagesELCConsole MArindam BasuNo ratings yet

- ELCAssetCell MDocument3 pagesELCAssetCell MArindam BasuNo ratings yet

- ELCAssetPicker XibDocument10 pagesELCAssetPicker XibArindam BasuNo ratings yet

- ELCAssetTablePicker MDocument6 pagesELCAssetTablePicker MArindam BasuNo ratings yet

- ELCAsset MDocument2 pagesELCAsset MArindam BasuNo ratings yet

- ELCImagePickerDemoAppDelegate MDocument2 pagesELCImagePickerDemoAppDelegate MArindam BasuNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cit Programme Guide 2021Document25 pagesCit Programme Guide 2021Abhir Singh haihay KalchuriNo ratings yet

- OBL RFP For PCI DSSDocument37 pagesOBL RFP For PCI DSSshakawathNo ratings yet

- Project File On E-CommerceDocument34 pagesProject File On E-CommerceHimanshu HNo ratings yet

- Soal Usbk B.inggrisDocument11 pagesSoal Usbk B.inggrisdila handayaniNo ratings yet

- Terms of Use - BrainlyDocument14 pagesTerms of Use - BrainlyMaría jose Ortega mejiaNo ratings yet

- NZY Company should adopt late outsourcing for IT systems and e-commerce websiteDocument3 pagesNZY Company should adopt late outsourcing for IT systems and e-commerce websiteAyesha Rahman MomoNo ratings yet

- Sample Personal Statement 2 0Document4 pagesSample Personal Statement 2 0Ly Hoang100% (1)

- SpiceJet - E-Ticket - PNR - FH4RQK 12 Nov 2022 Kolkata-Delhi For MR. AGRAWALDocument3 pagesSpiceJet - E-Ticket - PNR - FH4RQK 12 Nov 2022 Kolkata-Delhi For MR. AGRAWALAmeet Kumar AgarwalNo ratings yet

- SFM New TheoryDocument91 pagesSFM New TheoryDinesh JainNo ratings yet

- Procedures For Filing of ESTATE TAXDocument2 pagesProcedures For Filing of ESTATE TAXJennylyn Biltz AlbanoNo ratings yet

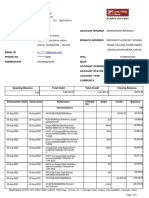

- View account statement and balance detailsDocument2 pagesView account statement and balance detailsPreeti SinghNo ratings yet

- 1580740668762Document26 pages1580740668762A.E.PNo ratings yet

- RBI E-Mandate Guidelines FAQsDocument3 pagesRBI E-Mandate Guidelines FAQsDjxjfdu fjedjNo ratings yet

- Rapid Bus bank statement analysisDocument48 pagesRapid Bus bank statement analysisAraman AmruNo ratings yet

- Customer Satisfaction Towards HDFC BANKS and SBIDocument89 pagesCustomer Satisfaction Towards HDFC BANKS and SBIdivya palaniswamiNo ratings yet

- 1 - CCAvenue Integration - Ver 2.0 PDFDocument33 pages1 - CCAvenue Integration - Ver 2.0 PDFPrathamesh LingayatNo ratings yet

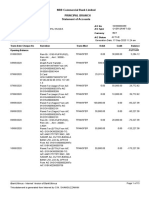

- NRB Commercial Bank Limited Principal Branch Statement of AccountsDocument15 pagesNRB Commercial Bank Limited Principal Branch Statement of AccountsS.M. Shamsuzzaman SalimNo ratings yet

- Automotive Consulting Solution: Warranty Management - Fast Start For Automotive SuppliersDocument61 pagesAutomotive Consulting Solution: Warranty Management - Fast Start For Automotive SuppliersMädeNo ratings yet

- Dental Office ManualDocument42 pagesDental Office Manualchoir master of manyNo ratings yet

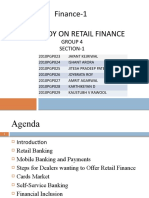

- A Study On Retail Finance - Group4 - Section 1Document32 pagesA Study On Retail Finance - Group4 - Section 1Kitto TurtleNo ratings yet

- Power BinsDocument1 pagePower Binsrickymarts100% (2)

- IDFCFIRSTBankstatemntDocument8 pagesIDFCFIRSTBankstatemntMOHAMMAD IQLASHNo ratings yet

- E Commerce in India Literature ReviewDocument54 pagesE Commerce in India Literature ReviewShahnoor Hossain50% (2)

- Detailed Statement: Citibank Rewards Platinum CardDocument4 pagesDetailed Statement: Citibank Rewards Platinum CardSudhir BarwalNo ratings yet

- Annual Report 2020Document444 pagesAnnual Report 2020haseen ullahNo ratings yet

- Credit Card ReportDocument136 pagesCredit Card Reportjoe_inbaNo ratings yet

- Account StatementDocument2 pagesAccount Statementmaharshi DaddyNo ratings yet

- Credit CardsDocument21 pagesCredit Cardsdixita_chotalia3829100% (1)

- SAP in House Cash With MySAP ERPDocument28 pagesSAP in House Cash With MySAP ERPulanaro100% (1)