You might also like

- Capturing Value From Digital and Advanced Analytics in The O&G IndustryDocument10 pagesCapturing Value From Digital and Advanced Analytics in The O&G IndustryGabriel Tortolero JimenezNo ratings yet

- PETRONAS Activity Outlook 2019-2021Document39 pagesPETRONAS Activity Outlook 2019-2021Faiz RahmanNo ratings yet

- Opex 2019 The Drive Towards Operational Excellence in Oil and Gas Oil and Gas iqRNIFb0AhUSeZzZ1Z9WwJIZAWN3fSM6XmxOQCtOiG PDFDocument10 pagesOpex 2019 The Drive Towards Operational Excellence in Oil and Gas Oil and Gas iqRNIFb0AhUSeZzZ1Z9WwJIZAWN3fSM6XmxOQCtOiG PDFnaveenNo ratings yet

- Exit InterviewDocument11 pagesExit InterviewPatrick BarettoNo ratings yet

- HR Director Business Partner in United States Resume Joseph WadeDocument2 pagesHR Director Business Partner in United States Resume Joseph WadeJosephWadeNo ratings yet

- Chapter 13 - Solutions: Demand 34000 UnitsDocument7 pagesChapter 13 - Solutions: Demand 34000 UnitsJimena OchoaNo ratings yet

- 6 Economics 1 PDFDocument44 pages6 Economics 1 PDFjhon berez223344No ratings yet

- Competency MappingDocument14 pagesCompetency MappingKarthika KaimalNo ratings yet

- Management Guide: Board of DirectorsDocument39 pagesManagement Guide: Board of Directorsmohamed abd eldayemNo ratings yet

- ONGC CSR Final NikhilDocument66 pagesONGC CSR Final Nikhilenrique_sumit100% (1)

- Infographic Oil and Gas Downstream OperationDocument1 pageInfographic Oil and Gas Downstream OperationHWANG INBUMNo ratings yet

- CaltexDocument1 pageCaltexHabiba MukhtarNo ratings yet

- I'll Phone You Back - SchedullingDocument7 pagesI'll Phone You Back - SchedullingAnkurNo ratings yet

- Swot Analiza Hotela KinaDocument18 pagesSwot Analiza Hotela KinaKrystal ChapmanNo ratings yet

- Majalah IA Dec2018 PDFDocument72 pagesMajalah IA Dec2018 PDFmariazesualdaNo ratings yet

- Presented By: Presented By: - Rohit Goel Rohit Goel (M.B.A. HONS. 2.2) (M.B.A. HONS. 2.2) Roll No ROLL NO - 2207 2207Document12 pagesPresented By: Presented By: - Rohit Goel Rohit Goel (M.B.A. HONS. 2.2) (M.B.A. HONS. 2.2) Roll No ROLL NO - 2207 2207meetrohitgoel0% (1)

- Adjusting To HR Restructuring TrendsDocument3 pagesAdjusting To HR Restructuring TrendsSafiullah KhanNo ratings yet

- Upstream Operations: Key FiguresDocument6 pagesUpstream Operations: Key FiguresIssam KNo ratings yet

- Dual Career PathsDocument5 pagesDual Career Pathspatriciasantosx100% (1)

- Exxon Mobil Merger DetailsDocument20 pagesExxon Mobil Merger DetailsPranay Chauhan100% (2)

- HR RatiosDocument3 pagesHR RatiosnirmaldevalNo ratings yet

- Types of CompetenciesDocument17 pagesTypes of CompetenciesNikita SangalNo ratings yet

- The Ethical Nature of HRMDocument9 pagesThe Ethical Nature of HRMVishal Kant RaiNo ratings yet

- Human Resource Management in The Russian Oil and Gas Industry: The Contemporary Social Priorities.Document41 pagesHuman Resource Management in The Russian Oil and Gas Industry: The Contemporary Social Priorities.al.k472No ratings yet

- Improving Performance at The Hotel Paris: The New Job DescriptionsDocument12 pagesImproving Performance at The Hotel Paris: The New Job DescriptionsNazmus SakibNo ratings yet

- PetroSkills O&MDocument12 pagesPetroSkills O&Mfoobar2016No ratings yet

- Shell PakistanDocument92 pagesShell Pakistantalhagujjar2No ratings yet

- The Board-Management RelationshipDocument32 pagesThe Board-Management RelationshipAlisha SthapitNo ratings yet

- PWC Oil Gas Guide 2019 PDFDocument148 pagesPWC Oil Gas Guide 2019 PDFRafael DamarNo ratings yet

- Strategy & HR LinkageDocument67 pagesStrategy & HR LinkageVineet JustaNo ratings yet

- Final EcotelDocument70 pagesFinal Ecoteljaybagadia100% (3)

- Leaves PolicyDocument5 pagesLeaves PolicyGul Raiz RanaNo ratings yet

- MA HR Issues Around The WorldDocument96 pagesMA HR Issues Around The WorldpensiontalkNo ratings yet

- Case Study BMWDocument8 pagesCase Study BMWAman KhobragadeNo ratings yet

- CeramicaCleoptra Brand Managment Plan ContainsDocument38 pagesCeramicaCleoptra Brand Managment Plan ContainsAbdulrhman TantawyNo ratings yet

- Allocating Resources Based on Performance ContributionsDocument23 pagesAllocating Resources Based on Performance ContributionsEkta Sandeep SharmaNo ratings yet

- HR Manager or Sr. HR Generalist or HR Business Partner or Sr. emDocument2 pagesHR Manager or Sr. HR Generalist or HR Business Partner or Sr. emapi-121342565100% (1)

- Job Specification - Technical ManagerDocument3 pagesJob Specification - Technical ManagerMian ZainNo ratings yet

- Petronas Activity Outlook 2017 2019Document46 pagesPetronas Activity Outlook 2017 2019SYED FADZIL SYED MOHAMEDNo ratings yet

- RRR Framework Professional StaffDocument10 pagesRRR Framework Professional StaffgenerationpoetNo ratings yet

- History of Oil Industry in PakistanDocument44 pagesHistory of Oil Industry in PakistanMuhammad IrfanNo ratings yet

- Egypt Oil Gas Market Report 2019-08-14Document52 pagesEgypt Oil Gas Market Report 2019-08-14midomatterNo ratings yet

- Process Engineer III - V Basic FunctionDocument4 pagesProcess Engineer III - V Basic FunctionmessiNo ratings yet

- HR ManagementDocument13 pagesHR ManagementcpierenNo ratings yet

- Upstream SeminarDocument61 pagesUpstream Seminarlaleye_olumideNo ratings yet

- Performance Appraisals in CadburyDocument2 pagesPerformance Appraisals in Cadburypratiksha240% (1)

- Chevron From ScribdDocument15 pagesChevron From ScribdcelinaNo ratings yet

- Indian IT BPO Industry AnalysisDocument13 pagesIndian IT BPO Industry AnalysisShivesh Ranjan100% (1)

- BP and Consolidation of Oil IndustryDocument2 pagesBP and Consolidation of Oil IndustryakankshaNo ratings yet

- Lack of Mechanical Integrity Blamed For Leak at Exxon Mobil RefineryDocument4 pagesLack of Mechanical Integrity Blamed For Leak at Exxon Mobil RefineryKalaivani ArunachalamNo ratings yet

- Shell Capital Markets Day 2016 Analyst Webcast Presentation Slides 160607122448Document80 pagesShell Capital Markets Day 2016 Analyst Webcast Presentation Slides 160607122448kglorstad100% (1)

- Strategic CEO President COO in San Diego CA Resume Michael StraussDocument3 pagesStrategic CEO President COO in San Diego CA Resume Michael StraussMichaelStraussNo ratings yet

- McKinsey On Oil & GasDocument8 pagesMcKinsey On Oil & Gasgweberpe@gmailcomNo ratings yet

- Customer Executive - Job DescriptionDocument7 pagesCustomer Executive - Job DescriptionMayank PandeyNo ratings yet

- Gino Sa Case Study AnalysisDocument62 pagesGino Sa Case Study AnalysisGopal MahajanNo ratings yet

- Group 3 Document Analyzes Profitability of Cola IndustryDocument9 pagesGroup 3 Document Analyzes Profitability of Cola IndustryNitesh SoniNo ratings yet

- Corwn, Cork and Seal - Group 6 - 2Document6 pagesCorwn, Cork and Seal - Group 6 - 2Sumit RajNo ratings yet

- GroupJ Cola Wars ContinueDocument36 pagesGroupJ Cola Wars ContinueAnupam ChaplotNo ratings yet

- Ice-Fili Case Study: Strategic Recommendations Needed to Combat Industry Shrinkage and Rising CompetitionDocument11 pagesIce-Fili Case Study: Strategic Recommendations Needed to Combat Industry Shrinkage and Rising CompetitionteenuNo ratings yet

- Week 2Document112 pagesWeek 2Ankit HatalkarNo ratings yet

- Combined SPSS in Excel 456Document89 pagesCombined SPSS in Excel 456killer dramaNo ratings yet

- SDDocument1 pageSDkiller dramaNo ratings yet

- Key Takeaways From E&Y WebinarDocument2 pagesKey Takeaways From E&Y Webinarkiller dramaNo ratings yet

- Boeing 777 ADocument3 pagesBoeing 777 Akiller dramaNo ratings yet

- Nedbank Case Study - FinalDocument2 pagesNedbank Case Study - Finalkiller dramaNo ratings yet

- Scale For EFA For Resilience ModelDocument9 pagesScale For EFA For Resilience Modelkiller dramaNo ratings yet

- Paper More-Excel SheetDocument133 pagesPaper More-Excel Sheetkiller dramaNo ratings yet

- PAnelDocument11 pagesPAnelkiller dramaNo ratings yet

- Looper Height TagsDocument1 pageLooper Height Tagskiller dramaNo ratings yet

- P&G's Organizational EvolutionDocument6 pagesP&G's Organizational Evolutionkiller dramaNo ratings yet

- Ucalgary 2013 Kano LienaDocument349 pagesUcalgary 2013 Kano Lienakiller dramaNo ratings yet

- Oep SCMP A5 Minibrochure WebDocument8 pagesOep SCMP A5 Minibrochure Webkiller dramaNo ratings yet

- Research Papers Ref 30th JanDocument33 pagesResearch Papers Ref 30th Jankiller dramaNo ratings yet

- Syntax GG PlotDocument3 pagesSyntax GG Plotkiller dramaNo ratings yet

- Doe PracticeDocument237 pagesDoe Practicekiller dramaNo ratings yet

- Type I and Type II Errror in ACCDocument3 pagesType I and Type II Errror in ACCkiller dramaNo ratings yet

- Manual For Building ANP Decision ModelsDocument84 pagesManual For Building ANP Decision Modelskiller dramaNo ratings yet

- Specification For - OGPCS008 (Online Grading System)Document1 pageSpecification For - OGPCS008 (Online Grading System)killer dramaNo ratings yet

- LIC Zonal Grievance OfficersDocument1 pageLIC Zonal Grievance Officerskiller dramaNo ratings yet

- Reliance Trend Store ProjectDocument9 pagesReliance Trend Store Projectkiller dramaNo ratings yet

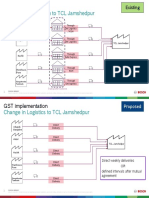

- Annexure 2 - Change in Logistics To TCL JamshedpurDocument2 pagesAnnexure 2 - Change in Logistics To TCL Jamshedpurkiller dramaNo ratings yet

- Executive Summary:: Sl. No. Areas Implications Under GSTDocument2 pagesExecutive Summary:: Sl. No. Areas Implications Under GSTkiller dramaNo ratings yet

- PH Case Mexico BOPDocument6 pagesPH Case Mexico BOPkiller dramaNo ratings yet

- Macro Note BookDocument56 pagesMacro Note Bookkiller dramaNo ratings yet

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDocument6 pagesWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaNo ratings yet

- Mo Os Best Post GST PDFDocument60 pagesMo Os Best Post GST PDFkiller dramaNo ratings yet

- Incomplete Solutions Case StudyDocument6 pagesIncomplete Solutions Case Studykiller dramaNo ratings yet

- Sqms QueryDocument2 pagesSqms Querykiller dramaNo ratings yet

- Randall's Advertising & Sales Promotion Case Study AnalysisDocument6 pagesRandall's Advertising & Sales Promotion Case Study Analysiskiller dramaNo ratings yet

- GST: A Metamorphic ReformDocument46 pagesGST: A Metamorphic Reformkiller dramaNo ratings yet

- Tax Rules For Domestic AirlinesDocument52 pagesTax Rules For Domestic AirlinesKath LeynesNo ratings yet

- A Project Management Bench Mark: Delhi MetroDocument26 pagesA Project Management Bench Mark: Delhi Metrodineshsoni29685No ratings yet

- Tax1 1 Basic Principles of Taxation 01.30.11-Long - For Printing - Without AnswersDocument10 pagesTax1 1 Basic Principles of Taxation 01.30.11-Long - For Printing - Without AnswersCracker Oats83% (6)

- National IncomeDocument4 pagesNational Incomesubbu2raj3372No ratings yet

- Form 1625062023 043026Document2 pagesForm 1625062023 043026SHIV BHAJANNo ratings yet

- Capital Gains Tax PDFDocument3 pagesCapital Gains Tax PDFvalsupmNo ratings yet

- Triveni TurbineDocument14 pagesTriveni Turbinecanaryhill100% (1)

- Cfap 1 Aafr PKDocument336 pagesCfap 1 Aafr PKArslan Shafique Ch100% (1)

- Bar ExamsDocument17 pagesBar ExamsCatherine PantiNo ratings yet

- Evangelita Vs Spouses Andolong III Et - Al.Document1 pageEvangelita Vs Spouses Andolong III Et - Al.Lara CacalNo ratings yet

- Bir Form 2305Document1 pageBir Form 2305rbolandoNo ratings yet

- Formal Letter Opf DemandDocument8 pagesFormal Letter Opf DemandrcpanganibanNo ratings yet

- Buying and SellingDocument19 pagesBuying and SellingNeri SangalangNo ratings yet

- Manufacturing OperationsDocument13 pagesManufacturing OperationsAlyssa Camille CabelloNo ratings yet

- BondAnalytics GlossaryDocument4 pagesBondAnalytics GlossaryNaveen KumarNo ratings yet

- An Irate Distributor: The Question of Profitability: Team 4Document12 pagesAn Irate Distributor: The Question of Profitability: Team 4Surbhi SabharwalNo ratings yet

- Salary Structure CreationDocument4 pagesSalary Structure CreationPriyankaNo ratings yet

- Advanced Cost Accounting Operating Costing On Hotel, Hosptal,& TransportDocument52 pagesAdvanced Cost Accounting Operating Costing On Hotel, Hosptal,& TransportVandana SharmaNo ratings yet

- Uy Law Office Balance SheetDocument2 pagesUy Law Office Balance SheetA c100% (1)

- Change in Demand and Supply Due To Factors Other Than PriceDocument4 pagesChange in Demand and Supply Due To Factors Other Than PriceRakesh YadavNo ratings yet

- Statement of Cash FlowsDocument10 pagesStatement of Cash Flowskimaya12No ratings yet

- November 21, 2014 Strathmore TimesDocument28 pagesNovember 21, 2014 Strathmore TimesStrathmore TimesNo ratings yet

- Chapter 10 - HW SolutionsDocument8 pagesChapter 10 - HW Solutionsa882906No ratings yet

- Settlement Terms Between Mizzou, Hillsdale Over Conservative Donor's InstructionsDocument74 pagesSettlement Terms Between Mizzou, Hillsdale Over Conservative Donor's InstructionsThe College FixNo ratings yet

- Financial Analysis of Hòa Phát Group Joint Stock CompanyDocument36 pagesFinancial Analysis of Hòa Phát Group Joint Stock CompanySang NguyễnNo ratings yet

- Axis Bank LTD Payslip For The Month of May - 2021Document2 pagesAxis Bank LTD Payslip For The Month of May - 2021Suman DasNo ratings yet

- Capstone ProjectDocument10 pagesCapstone ProjectinxxxsNo ratings yet

- Calpine Corp. The Evolution From Project To Corporate FinanceDocument4 pagesCalpine Corp. The Evolution From Project To Corporate FinanceDarshan Gosalia100% (1)

- Nonresident Alien Engaged in Trade or BusinessDocument2 pagesNonresident Alien Engaged in Trade or BusinessHEARTHEL KATE BUYUCCANNo ratings yet

- The Personal MBA (Summary)Document13 pagesThe Personal MBA (Summary)Boy BearishNo ratings yet