You might also like

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Format of Statutory Audit Report for Private Limited CompanyDocument11 pagesFormat of Statutory Audit Report for Private Limited CompanySwetha SNo ratings yet

- Apar FormatDocument26 pagesApar Formatpeace2047No ratings yet

- Procedure of Conversion of Private LTDDocument4 pagesProcedure of Conversion of Private LTDNisha11sharmaNo ratings yet

- SAVIOR Payroll Software User ManualDocument24 pagesSAVIOR Payroll Software User ManualDevang Soni100% (1)

- Auditing SEM-6: Company AuditDocument21 pagesAuditing SEM-6: Company AuditShilpan ShahNo ratings yet

- Investment Law Project Nisha Gupta Rajshri Singh and Raj Vardhan Agarwal (BBA - LLB (H) ) 8th SemesterDocument20 pagesInvestment Law Project Nisha Gupta Rajshri Singh and Raj Vardhan Agarwal (BBA - LLB (H) ) 8th Semesterraj vardhan agarwalNo ratings yet

- BOA Updates 01.2017 PDFDocument41 pagesBOA Updates 01.2017 PDFRojohn Mesiera ValenzuelaNo ratings yet

- Annual ReportDocument37 pagesAnnual ReportMukesh ManwaniNo ratings yet

- PwC summarizes key changes in India's new overseas investment rulesDocument5 pagesPwC summarizes key changes in India's new overseas investment rulesVishwas SharmaNo ratings yet

- Saftea Annual Report 2014Document54 pagesSaftea Annual Report 2014safteaNo ratings yet

- Foreign Exchange Management Act, 1999 (FEMA) : Prof. Dhaval BhattDocument22 pagesForeign Exchange Management Act, 1999 (FEMA) : Prof. Dhaval BhattMangesh KadamNo ratings yet

- R.kasi Vishwanathan & Bros. V Assist CIt (2014) 42 Taxmann - Com 176 Section 139 (5) - It 475-11 28.3.2016Document7 pagesR.kasi Vishwanathan & Bros. V Assist CIt (2014) 42 Taxmann - Com 176 Section 139 (5) - It 475-11 28.3.2016Prabhash ChandNo ratings yet

- On The Job Training Log Book: Faculty of CommerceDocument12 pagesOn The Job Training Log Book: Faculty of CommerceAnonymous Hig1tC2hNo ratings yet

- FEMA Rules & Policies: Government of India World Trade OrganisationDocument2 pagesFEMA Rules & Policies: Government of India World Trade OrganisationPradeep KumarNo ratings yet

- Accounting concepts guide recordingDocument8 pagesAccounting concepts guide recordingDeepu LuvesNo ratings yet

- From This Site You Can Get All The Reference Letter FormatDocument9 pagesFrom This Site You Can Get All The Reference Letter FormatPrasad PhawadeNo ratings yet

- ESOP and Sweat EquityDocument7 pagesESOP and Sweat EquityShehana RenjuNo ratings yet

- Lead Schedule: Refer To The Attached Sample Bank Confirmation TemplateDocument4 pagesLead Schedule: Refer To The Attached Sample Bank Confirmation TemplateChristian Dela CruzNo ratings yet

- Affidavit FormatDocument1 pageAffidavit Formatsourav84No ratings yet

- PMS AgreementDocument41 pagesPMS AgreementSandeep BorseNo ratings yet

- Audit of Forex TransactionsDocument4 pagesAudit of Forex Transactionsnamcheang100% (2)

- Slump Sale and Slump Exchange ExplainedDocument36 pagesSlump Sale and Slump Exchange ExplainedVicky Murthy0% (1)

- Commonly Found Non-Compliances of SCH II&III of Companies Act - CA - Akshat BahetiDocument37 pagesCommonly Found Non-Compliances of SCH II&III of Companies Act - CA - Akshat BahetiCIBIL CHURUNo ratings yet

- Administrative Law Psda SubmissionDocument10 pagesAdministrative Law Psda SubmissionVasundhara SaxenaNo ratings yet

- MSME affidavit for interest subventionDocument2 pagesMSME affidavit for interest subventionAmit Agarwal100% (2)

- Impact of GST On Stock MarketDocument14 pagesImpact of GST On Stock MarketSiddhartha0% (1)

- Confidential Information Case Study2Document3 pagesConfidential Information Case Study2SereneNo ratings yet

- 22 Stock Audit Report FormatDocument15 pages22 Stock Audit Report FormatSaptarshi CoomarNo ratings yet

- C & F - DRAFT - AGREEMENT - GGJ Solutions - Dated - 27.3.2021Document8 pagesC & F - DRAFT - AGREEMENT - GGJ Solutions - Dated - 27.3.2021Sparsh GargNo ratings yet

- Impact of Hand Sanitizer Format Gel Foam Liquid and Dose 2018 Journal ofDocument7 pagesImpact of Hand Sanitizer Format Gel Foam Liquid and Dose 2018 Journal ofRoxana Mihaela PopoviciNo ratings yet

- 250 QuestionsDocument44 pages250 QuestionsPrajeeth Nair100% (1)

- Dormant CompanyDocument3 pagesDormant CompanyAvaniJainNo ratings yet

- SZREIT ProspectusDocument372 pagesSZREIT Prospectusjojoboy123No ratings yet

- Inter Bank TransferDocument22 pagesInter Bank Transferpankajku2020100% (2)

- LLP AgreementDocument7 pagesLLP AgreementJay100% (1)

- SAR FormatDocument13 pagesSAR FormatAbhimanyu YadavNo ratings yet

- AGM TemplateDocument2 pagesAGM TemplateSheryl Ng0% (1)

- Cheque BounceDocument5 pagesCheque BounceLucky VinnakotaNo ratings yet

- Stock Yard Agreement TermsDocument18 pagesStock Yard Agreement TermsSalman QureshiNo ratings yet

- How To Persuade A ClientDocument1 pageHow To Persuade A ClientHani Rifani PutriNo ratings yet

- Listing Agreement 03-09-2009Document86 pagesListing Agreement 03-09-2009Subhash SahuNo ratings yet

- SECP Change in Registered Office Address 06 MarchDocument4 pagesSECP Change in Registered Office Address 06 Marchinfo.pbs2020No ratings yet

- Refunds: What Type of Refund Are You Applying For?Document2 pagesRefunds: What Type of Refund Are You Applying For?Leigh OlssonNo ratings yet

- Nedbank Payment Requisition FormDocument2 pagesNedbank Payment Requisition FormRidah SolomonNo ratings yet

- Bad Debts RecoveryDocument6 pagesBad Debts RecoveryThilaga Senthilmurugan100% (1)

- Introduction of Chartered AccountantDocument2 pagesIntroduction of Chartered AccountantAashish Aashri100% (1)

- TBDDocument34 pagesTBDArjun VijNo ratings yet

- New VAT Audit FormatDocument12 pagesNew VAT Audit FormatparulshinyNo ratings yet

- Data FOC Agreement 10042012 (Clean Final)Document9 pagesData FOC Agreement 10042012 (Clean Final)Mohsin ShaikhNo ratings yet

- Meghna Petroleum Limited: Chart of AccountsDocument21 pagesMeghna Petroleum Limited: Chart of AccountsAbu Shahadat Muhammad SayeemNo ratings yet

- How Foreign Companies Can Enter Into IndiaDocument4 pagesHow Foreign Companies Can Enter Into Indiaad18111989No ratings yet

- IB PPT On IMFDocument22 pagesIB PPT On IMFAtul YadavNo ratings yet

- Lending Works Lender Platform Terms and ConditionsDocument30 pagesLending Works Lender Platform Terms and ConditionsliakhuletzNo ratings yet

- Citibank CFO PresentationDocument29 pagesCitibank CFO PresentationDiego de AragãoNo ratings yet

- Register A Transport Company in KenyaDocument16 pagesRegister A Transport Company in KenyaSamsonNo ratings yet

- Buy Back of SecuritiesDocument7 pagesBuy Back of SecuritiesTaruna SanotraNo ratings yet

- Bylaws of CorporationDocument9 pagesBylaws of CorporationAboromo LimotoNo ratings yet

- A.8.1 Engagement Letter 31032023 - Statutory AuditDocument4 pagesA.8.1 Engagement Letter 31032023 - Statutory AuditAyush AgrawalNo ratings yet

- EL_Unlisted Companies Individual without IFCDocument13 pagesEL_Unlisted Companies Individual without IFCNAYAN PATELNo ratings yet

- Certificate From Supervisor (Blood Relation)Document1 pageCertificate From Supervisor (Blood Relation)kanavNo ratings yet

- Ratio AnalysisDocument42 pagesRatio AnalysiskanavNo ratings yet

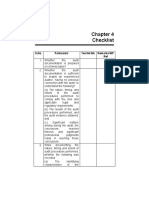

- Checklist: S.No. Particulars Yes/No/NA Remarks/WP RefDocument4 pagesChecklist: S.No. Particulars Yes/No/NA Remarks/WP RefkanavNo ratings yet

- Ms Word Format Audit Engagement Letter Cos Act 2013Document10 pagesMs Word Format Audit Engagement Letter Cos Act 2013kanavNo ratings yet

- T1 - Cases Company Introduction, KindsDocument17 pagesT1 - Cases Company Introduction, KindskanavNo ratings yet

- Mesicic4 GRD Audit2 PDFDocument3 pagesMesicic4 GRD Audit2 PDFkanavNo ratings yet

- T1 - Cases Company Introduction, KindsDocument17 pagesT1 - Cases Company Introduction, KindskanavNo ratings yet

- Ms Word Format Audit Engagement Letter2 Cos Act 2013Document9 pagesMs Word Format Audit Engagement Letter2 Cos Act 2013kanavNo ratings yet

- MCQ - Auditing - PL PDFDocument31 pagesMCQ - Auditing - PL PDFWesley Smith73% (44)

- D) To Submits The Accounts To The GovernmentDocument2 pagesD) To Submits The Accounts To The GovernmentkanavNo ratings yet

- D) To Submits The Accounts To The GovernmentDocument2 pagesD) To Submits The Accounts To The GovernmentkanavNo ratings yet

- JIODocument7 pagesJIOkanavNo ratings yet

- Deepak Bhai - Repaired - FINALDocument107 pagesDeepak Bhai - Repaired - FINALNehaNo ratings yet

- PG MPDocument6 pagesPG MPsiajNo ratings yet

- DL7 - Practice - Assignment - 1 - ANURAG TEJA RATHNAMDocument4 pagesDL7 - Practice - Assignment - 1 - ANURAG TEJA RATHNAMSaahilNo ratings yet

- Future Focus Employee HandbookDocument49 pagesFuture Focus Employee Handbooksureshnov4No ratings yet

- Ch12 Transfer Pricing P12-15, P12-17, P12-24, P12-32, P12-35Document8 pagesCh12 Transfer Pricing P12-15, P12-17, P12-24, P12-32, P12-35kidflash1234No ratings yet

- Production SystemsDocument24 pagesProduction SystemsAsad KhanNo ratings yet

- Case Study 1Document3 pagesCase Study 1Nam Phuong Nguyen100% (1)

- Group Account Manager experienceDocument2 pagesGroup Account Manager experienceIshaan YadavNo ratings yet

- 2 - Network PlanningDocument6 pages2 - Network PlanningFilipeNo ratings yet

- Cost AccountingDocument57 pagesCost AccountingM.K. TongNo ratings yet

- Preliminary q1 9 Audit ChecklistDocument10 pagesPreliminary q1 9 Audit ChecklistJulius Hendra100% (2)

- Chapter 7 Entry Strategies and Organizational StructuresDocument36 pagesChapter 7 Entry Strategies and Organizational StructuresAMAL WAHYU FATIHAH BINTI ABDUL RAHMAN BB20110906No ratings yet

- CH 01 (Day 01) PDFDocument7 pagesCH 01 (Day 01) PDFAnonymous yL88JjNo ratings yet

- Auditing and Accounting DifferencesDocument65 pagesAuditing and Accounting DifferencesTushar GaurNo ratings yet

- ISO 127025 Quality Manual SampleDocument6 pagesISO 127025 Quality Manual SampleTamer Farouk KhalifaNo ratings yet

- PM2 Project Management MethodologyDocument147 pagesPM2 Project Management MethodologyFernando100% (1)

- CV Project Assistant ZDocument2 pagesCV Project Assistant Zmaha AbdulazizNo ratings yet

- Audit Evidence and Documentation Ch 05Document59 pagesAudit Evidence and Documentation Ch 05juan60% (10)

- S 4 Hana Overview - PDF CatalogueDocument17 pagesS 4 Hana Overview - PDF CatalogueSayantani Bhattacharya0% (1)

- Personal Planning RecruitmentDocument23 pagesPersonal Planning RecruitmentalvhaNo ratings yet

- QFD-based fuzzy MCDM approach for supplier selectionDocument12 pagesQFD-based fuzzy MCDM approach for supplier selectionIman MashayekhNo ratings yet

- EMA's Impact on Sustainable Competitive AdvantagesDocument13 pagesEMA's Impact on Sustainable Competitive AdvantagesfahruNo ratings yet

- 2021 - PJM - L - 1 - 1627131557715-Project ManagementDocument58 pages2021 - PJM - L - 1 - 1627131557715-Project ManagementKumar AbhishekNo ratings yet

- Leica CCP Brochure enDocument4 pagesLeica CCP Brochure enn1kskeNo ratings yet

- SOP - MBA (Global)Document2 pagesSOP - MBA (Global)কোয়াফ ট্রেডার্স এন্ড এন্টারপ্রাইজNo ratings yet

- BS Industrial Security Management Evaluation InstrumentDocument13 pagesBS Industrial Security Management Evaluation Instrumentrodolfo king bautista100% (1)

- The Diaper Industry in 1974 - GR - 7 - ADocument15 pagesThe Diaper Industry in 1974 - GR - 7 - AaabfjabfuagfuegbfNo ratings yet

- Cost ClassificationDocument8 pagesCost Classificationyashwant ashokNo ratings yet

- Models of Service QualityDocument12 pagesModels of Service QualityAmmy D ExtrovertNo ratings yet

- Process of Employee RetentionDocument28 pagesProcess of Employee RetentionArun KumarNo ratings yet

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksFrom EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksRating: 4 out of 5 stars4/5 (1)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- Electronic Health Records: An Audit and Internal Control GuideFrom EverandElectronic Health Records: An Audit and Internal Control GuideNo ratings yet

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsFrom EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNo ratings yet

- GDPR for DevOp(Sec) - The laws, Controls and solutionsFrom EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsRating: 5 out of 5 stars5/5 (1)

- Audit and Assurance Essentials: For Professional Accountancy ExamsFrom EverandAudit and Assurance Essentials: For Professional Accountancy ExamsNo ratings yet

- Lean Auditing: Driving Added Value and Efficiency in Internal AuditFrom EverandLean Auditing: Driving Added Value and Efficiency in Internal AuditRating: 5 out of 5 stars5/5 (1)

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- Fraud 101: Techniques and Strategies for Understanding FraudFrom EverandFraud 101: Techniques and Strategies for Understanding FraudNo ratings yet