You might also like

- EcoDev FinalsDocument4 pagesEcoDev FinalsChristian De GuzmanNo ratings yet

- Systematic Country Diagnostic of The Philippines - Realizing The Filipino Dream For 2040Document8 pagesSystematic Country Diagnostic of The Philippines - Realizing The Filipino Dream For 2040Chelsea ArzadonNo ratings yet

- The Republic of Philippines The Next Asian TigerDocument3 pagesThe Republic of Philippines The Next Asian TigerirmmooNo ratings yet

- Capital: Manila City: Philippine EconomyDocument8 pagesCapital: Manila City: Philippine Economynathaniel saileNo ratings yet

- The Philippine EconomyDocument44 pagesThe Philippine EconomyMarie ManansalaNo ratings yet

- Ferdinand Marcos AdministrationDocument4 pagesFerdinand Marcos AdministrationChandria FordNo ratings yet

- SOC - PeTa 2Document18 pagesSOC - PeTa 2jeq9eNo ratings yet

- Eco AssignmentDocument36 pagesEco AssignmentKaran KumarNo ratings yet

- ASEAN PhilippinesDocument39 pagesASEAN PhilippinesleshamunsayNo ratings yet

- Philippines Under The Martial LawDocument9 pagesPhilippines Under The Martial LawTrina Candelaria100% (2)

- Philippine Sectors: Strong in Services and Agriculture, Weak in IndustryDocument3 pagesPhilippine Sectors: Strong in Services and Agriculture, Weak in IndustryEmmanuel BaccarayNo ratings yet

- Chapter 7 Economic Dev'tDocument6 pagesChapter 7 Economic Dev'tmonique payong100% (2)

- Module 3 - BaltazarDocument60 pagesModule 3 - BaltazarNiña BaltazarNo ratings yet

- Philippines' Struggle with Poverty and InequalityDocument79 pagesPhilippines' Struggle with Poverty and InequalityIrisGayleJavierNo ratings yet

- The Roots of The Philippines - Economic TroublesDocument22 pagesThe Roots of The Philippines - Economic TroublesConzie MntajesNo ratings yet

- Economy of Philippines AssignmentDocument34 pagesEconomy of Philippines AssignmentKaran KumarNo ratings yet

- Philippines manufacturing faces supply chain challengesDocument6 pagesPhilippines manufacturing faces supply chain challengesDONNAVEL ROSALESNo ratings yet

- Philippine Economy Under Marcos: Debt-Fueled Growth and Crony CapitalismDocument2 pagesPhilippine Economy Under Marcos: Debt-Fueled Growth and Crony CapitalismairaNo ratings yet

- Agriculture-Ppt 20230921 112817 0000Document20 pagesAgriculture-Ppt 20230921 112817 0000dinafo4802No ratings yet

- Assignment Pa 504Document14 pagesAssignment Pa 504Rolando Cruzada Jr.No ratings yet

- The Philipines Economy in The Martial Law RegimeDocument19 pagesThe Philipines Economy in The Martial Law Regimemerlence jhoy valdezNo ratings yet

- PhilippinesDocument10 pagesPhilippinesAkhil sonuNo ratings yet

- Philippine Economic and Political History Finals 1Document17 pagesPhilippine Economic and Political History Finals 1Christian Jay MoralesNo ratings yet

- Draft Final AssesmentDocument8 pagesDraft Final AssesmentRussell FloydNo ratings yet

- Philippine Economic Development and Agriculture SectorsDocument50 pagesPhilippine Economic Development and Agriculture Sectorsenaportillo13No ratings yet

- Ethiopia's Financial System and Stock Market DevelopmentDocument19 pagesEthiopia's Financial System and Stock Market Developmentyared haftuNo ratings yet

- The Presidency of Gloria Macapagal Arroyo (2001-2010)Document21 pagesThe Presidency of Gloria Macapagal Arroyo (2001-2010)Janselle MiguelNo ratings yet

- Gloria Macapagal Arroyo PresDocument23 pagesGloria Macapagal Arroyo PresLizmae BermudezNo ratings yet

- CTT - Public Finance (Prelim Exam)Document4 pagesCTT - Public Finance (Prelim Exam)geofrey gepitulanNo ratings yet

- The Average Inflation Rate For 2009 Was 3.2 Percent Compared With 9.3 Percent in 2008, and Is Projected atDocument5 pagesThe Average Inflation Rate For 2009 Was 3.2 Percent Compared With 9.3 Percent in 2008, and Is Projected atCharlene LeynesNo ratings yet

- On Chinese Economy in EcomoniesDocument13 pagesOn Chinese Economy in EcomoniesPiyush_jain004100% (3)

- Philippines Economic History and DevelopmentDocument18 pagesPhilippines Economic History and DevelopmentMita KashikaNo ratings yet

- Role of Agriculture in The Economic Development of A CountryDocument9 pagesRole of Agriculture in The Economic Development of A CountryJoey LagahitNo ratings yet

- The Strategic Importance of The Philippine Manufacturing SectorDocument6 pagesThe Strategic Importance of The Philippine Manufacturing SectorchialunNo ratings yet

- Dev Eco Chap 2Document28 pagesDev Eco Chap 2Harshit BadhwarNo ratings yet

- I Economic Development: Capita-Gdp-Has-Reached-An-All-Time-High-Under-Duterte/#1db297e169b1Document40 pagesI Economic Development: Capita-Gdp-Has-Reached-An-All-Time-High-Under-Duterte/#1db297e169b1Che MerluNo ratings yet

- Final Major OutputDocument12 pagesFinal Major OutputMJ LositoNo ratings yet

- The in Econom CE Indepen CE: Dian Y Sin DENDocument40 pagesThe in Econom CE Indepen CE: Dian Y Sin DENDhruv KaushikNo ratings yet

- Philippine Mobile Overview 2014Document35 pagesPhilippine Mobile Overview 2014ROXASNo ratings yet

- AGRICULTUREDocument2 pagesAGRICULTUREJericho CarabidoNo ratings yet

- MIMAECODocument11 pagesMIMAECODeanna Fajardo UsonNo ratings yet

- HistGov FinalExamDocument5 pagesHistGov FinalExamLourine Vanguardia MondragonNo ratings yet

- The New Thinking' For Agriculture: by Dr. William D. DarDocument13 pagesThe New Thinking' For Agriculture: by Dr. William D. DarLaurenz James Coronado DeMattaNo ratings yet

- Module 1 - Public EnterpriseDocument13 pagesModule 1 - Public EnterpriseHoney Jane Tabugoc TajoraNo ratings yet

- ICEP CSS - PMS Presentation-by-Dr-Ishrat-Husain Pakistan Macro Economy - Current Situation and Way ForwardDocument43 pagesICEP CSS - PMS Presentation-by-Dr-Ishrat-Husain Pakistan Macro Economy - Current Situation and Way ForwardNadeem SheikhNo ratings yet

- Balisacan-Pernia TheRoralRoadtoPovertyReduction JAAS2002Document22 pagesBalisacan-Pernia TheRoralRoadtoPovertyReduction JAAS2002Resty BalinasNo ratings yet

- Sustainable Transportation in the PhilippinesDocument18 pagesSustainable Transportation in the PhilippinesRommel GavietaNo ratings yet

- Philippines Economy Hindrances and Globalization ImpactsDocument3 pagesPhilippines Economy Hindrances and Globalization ImpactsJhezzarie DonezaNo ratings yet

- About - Contact - Mongabay On Facebook - Mongabay On TwitterDocument14 pagesAbout - Contact - Mongabay On Facebook - Mongabay On TwitterAhsan ZahidNo ratings yet

- FDNECON C72 Alcalde, Nicole 800-Word Essay For FinalsDocument6 pagesFDNECON C72 Alcalde, Nicole 800-Word Essay For FinalsNicole AlcaldeNo ratings yet

- Research Paper. Triple IDocument26 pagesResearch Paper. Triple IEdward CasimiroNo ratings yet

- Agriculture Development in ZambiaDocument49 pagesAgriculture Development in ZambiaKahimbiNo ratings yet

- Bicol College Economic SectorsDocument21 pagesBicol College Economic SectorsRAMIREZ, KRISHA R.No ratings yet

- Africa after COVID-19: De-globalisation and Recalibrating Nations’ Growth ProspectsDocument8 pagesAfrica after COVID-19: De-globalisation and Recalibrating Nations’ Growth Prospectsdemba sowNo ratings yet

- Eco PKDocument12 pagesEco PKwaseem ahsanNo ratings yet

- Stage of Economic Development in MalaysiaDocument1 pageStage of Economic Development in Malaysiafaizmikano0% (1)

- Assignment On Economic Indicators - ShaziaDocument25 pagesAssignment On Economic Indicators - ShaziapimsatmbaNo ratings yet

- Country Overview: Philippines Growth Through Innovation: AnalysisDocument35 pagesCountry Overview: Philippines Growth Through Innovation: AnalysisJasmine YlayaNo ratings yet

- People's Republic of ChinaDocument12 pagesPeople's Republic of ChinaAlex DimaNo ratings yet

- The Rise of the African Multinational Enterprise (AMNE): The Lions Accelerating the Development of AfricaFrom EverandThe Rise of the African Multinational Enterprise (AMNE): The Lions Accelerating the Development of AfricaNo ratings yet

- Parents Guide To SNT - 05 - 2021Document14 pagesParents Guide To SNT - 05 - 2021YanoNo ratings yet

- AIA Philam Life Life Insurance Trust DeedDocument1 pageAIA Philam Life Life Insurance Trust DeedYanoNo ratings yet

- Brochures Coffeeprodguide PDFDocument28 pagesBrochures Coffeeprodguide PDFColumbia GomezNo ratings yet

- The Best Answer To "Sell Me This Pen" - 4 Tips To Sell in A Super Competitive IndustryDocument4 pagesThe Best Answer To "Sell Me This Pen" - 4 Tips To Sell in A Super Competitive IndustryYanoNo ratings yet

- Gall Bladder Stone FlushDocument5 pagesGall Bladder Stone FlushfumsmithNo ratings yet

- How To Grow Basil - Houzz PDFDocument16 pagesHow To Grow Basil - Houzz PDFYanoNo ratings yet

- 2 Inbar A Manual For Vegetative Propagation of Bamboos PDFDocument74 pages2 Inbar A Manual For Vegetative Propagation of Bamboos PDFYano100% (1)

- Abaca Fibre PDFDocument4 pagesAbaca Fibre PDFYanoNo ratings yet

- Coffee CultivationDocument65 pagesCoffee CultivationMadhavi RaoNo ratings yet

- SuperwormsDocument2 pagesSuperwormsYanoNo ratings yet

- Guidelines For Cultivating Ethiopian Lowland BambooDocument68 pagesGuidelines For Cultivating Ethiopian Lowland BambooEverboleh ChowNo ratings yet

- Directory of Womens Organization PDFDocument653 pagesDirectory of Womens Organization PDFYano0% (1)

- 2 Leao Research Part1Document30 pages2 Leao Research Part1YanoNo ratings yet

- 2 Inbar A Manual For Vegetative Propagation of Bamboos PDFDocument74 pages2 Inbar A Manual For Vegetative Propagation of Bamboos PDFYano100% (1)

- HB Chapter1 BambooCultivation SelectionofSpecies PDFDocument10 pagesHB Chapter1 BambooCultivation SelectionofSpecies PDFYanoNo ratings yet

- Registered Veterinary Drugs and Products-Manufacturers Updated PDFDocument5 pagesRegistered Veterinary Drugs and Products-Manufacturers Updated PDFYanoNo ratings yet

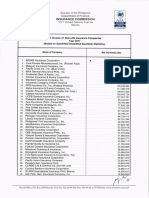

- Rankings of Insurance Brokers - Premiums Produced - 2016 PDFDocument3 pagesRankings of Insurance Brokers - Premiums Produced - 2016 PDFYanoNo ratings yet

- PhilHealth Guidebook PDFDocument127 pagesPhilHealth Guidebook PDFYanoNo ratings yet

- Premiums Earned of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesPremiums Earned of Non Life Insurance Companies - Year 2017 PDFYanoNo ratings yet

- Philippines Non-Life Insurance Assets 2017Document2 pagesPhilippines Non-Life Insurance Assets 2017YanoNo ratings yet

- Non-Life Insurance Companies Report Net Income of PHP 3.5B in 2017Document2 pagesNon-Life Insurance Companies Report Net Income of PHP 3.5B in 2017YanoNo ratings yet

- Rankings of Insurance Brokers - Premiums Produced - 2016 PDFDocument3 pagesRankings of Insurance Brokers - Premiums Produced - 2016 PDFYanoNo ratings yet

- Paid Up Capital of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesPaid Up Capital of Non Life Insurance Companies - Year 2017 PDFYanoNo ratings yet

- Rankings of Insurance Brokers - Commissions Earned - 2016 PDFDocument3 pagesRankings of Insurance Brokers - Commissions Earned - 2016 PDFYanoNo ratings yet

- Premiums Earned of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesPremiums Earned of Non Life Insurance Companies - Year 2017 PDFYanoNo ratings yet

- Net Premiums Written of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesNet Premiums Written of Non Life Insurance Companies - Year 2017 PDFYanoNo ratings yet

- Gross Premiums Written of Non Life Insurance Companies - Year 2017 PDFDocument4 pagesGross Premiums Written of Non Life Insurance Companies - Year 2017 PDFYanoNo ratings yet

- Networth of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesNetworth of Non Life Insurance Companies - Year 2017 PDFYanoNo ratings yet

- Philippines Electronics Cluster CompetitivenessDocument21 pagesPhilippines Electronics Cluster CompetitivenessYanoNo ratings yet

- QualityAssuranceProgram BenchbookDocument66 pagesQualityAssuranceProgram BenchbookRhod Bernaldez EstaNo ratings yet

- SKM600GB12T4 22892098.fast IGBT.62mmDocument6 pagesSKM600GB12T4 22892098.fast IGBT.62mmDejanStarčevićNo ratings yet

- Serializer UserGuideDocument45 pagesSerializer UserGuideJavo CoreNo ratings yet

- Spyder Family HONEYWELLDocument1 pageSpyder Family HONEYWELLRaphael LopesNo ratings yet

- Spice2001 07Document136 pagesSpice2001 07許智湧No ratings yet

- "Sss53S: Eazsiabesÿs I InstructionsDocument8 pages"Sss53S: Eazsiabesÿs I InstructionsAvishka ChanukaNo ratings yet

- NowYoureTalking ARRL Ed2Pr4 1995Document408 pagesNowYoureTalking ARRL Ed2Pr4 1995theeyeintheskyNo ratings yet

- High PassDocument2 pagesHigh PassMamoon BarbhuyanNo ratings yet

- IHGStandards-IHG Technical SpecificationsDocument36 pagesIHGStandards-IHG Technical Specificationsatlcomputech100% (2)

- Returned Receipt For Equipment: Land Transportation OfficeDocument68 pagesReturned Receipt For Equipment: Land Transportation Officemaricris punayNo ratings yet

- Gigabyte GA-AX370-Gaming K3 Rev1.0Document43 pagesGigabyte GA-AX370-Gaming K3 Rev1.0Juan RiquelmeNo ratings yet

- Practical Course For ATMEL MicrocontrollersDocument45 pagesPractical Course For ATMEL MicrocontrollersSubhash SumanNo ratings yet

- Veritas University SIWES Report on Networking at Code of Conduct Bureau & Galaxy BackboneDocument36 pagesVeritas University SIWES Report on Networking at Code of Conduct Bureau & Galaxy BackboneVICTORNo ratings yet

- SRC ProposalDocument6 pagesSRC ProposalVanlal KhiangteNo ratings yet

- Sistec Ec - 403 DCSDocument15 pagesSistec Ec - 403 DCSmab434No ratings yet

- 2008-2011 Domestic Battery Charger Maintenance and Service ManualDocument300 pages2008-2011 Domestic Battery Charger Maintenance and Service ManualmbgprsmsNo ratings yet

- Chisel BookDocument34 pagesChisel BookGuoli LvNo ratings yet

- GPM - Vco - Mods 2Document2 pagesGPM - Vco - Mods 2Abo OmarNo ratings yet

- Compact Low-Frequency Control Element: Datasheet LFDocument4 pagesCompact Low-Frequency Control Element: Datasheet LFpmacs10No ratings yet

- Purple Finder PDFDocument12 pagesPurple Finder PDFsahil jadonNo ratings yet

- Configure circuit breaker accessories with SDx moduleDocument1 pageConfigure circuit breaker accessories with SDx moduleMuhammad Firman FahrirozanNo ratings yet

- Sample Layer 3 - SFO - LTE - SC3B - Part3 - GoodZone - 01.2 Qualcomm - IPERFDocument1,411 pagesSample Layer 3 - SFO - LTE - SC3B - Part3 - GoodZone - 01.2 Qualcomm - IPERFVijay VasaNo ratings yet

- What's The Difference Between CTS, Multisource CTS, and Clock MeshDocument7 pagesWhat's The Difference Between CTS, Multisource CTS, and Clock MeshRenju TjNo ratings yet

- 2nd Sem DIP Electrical Circuits - Dec 2014 PDFDocument3 pages2nd Sem DIP Electrical Circuits - Dec 2014 PDFPrasad C MNo ratings yet

- SLD GSS NalandaDocument1 pageSLD GSS NalandaRahul KumarNo ratings yet

- Change Over Socomec ATYS-PMDocument2 pagesChange Over Socomec ATYS-PMHrvoje DubravaNo ratings yet

- Toshiba 32av700e LCD TV SCHDocument44 pagesToshiba 32av700e LCD TV SCHMuhammad Ihsan100% (1)

- Check Point Appliance Comparison Chart PDFDocument8 pagesCheck Point Appliance Comparison Chart PDFChau LhNo ratings yet

- Office Vocabulay KeyDocument4 pagesOffice Vocabulay KeytinydaisyNo ratings yet

- Time Domain Response of Second Order Linear CircuitsDocument15 pagesTime Domain Response of Second Order Linear CircuitsMOHSINALI MOMINNo ratings yet