You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Alberta Economic Multipliers 2011Document66 pagesAlberta Economic Multipliers 2011Ffedsw NicksNo ratings yet

- Sample Feasibility Study On Convention CenterDocument127 pagesSample Feasibility Study On Convention Centerjelo_lozano4998100% (4)

- Global Economic Impact Study of Shopify: April 2021Document38 pagesGlobal Economic Impact Study of Shopify: April 2021darkjfman_680607290No ratings yet

- Public Transportation Investment Boosts EconomyDocument77 pagesPublic Transportation Investment Boosts EconomyAgus HudoyoNo ratings yet

- Atag PDFDocument80 pagesAtag PDFyusuf efendiNo ratings yet

- CV - Kennedy Onyango Nanga, (Statistician)Document5 pagesCV - Kennedy Onyango Nanga, (Statistician)konangaNo ratings yet

- PWC Study: The Economic Impacts of The Oil and Natural Gas Industry On The U.S. EconomyDocument85 pagesPWC Study: The Economic Impacts of The Oil and Natural Gas Industry On The U.S. EconomyEnergy TomorrowNo ratings yet

- Learning Module Blended Flexible Learning: Macro Perspective of Tourism and Hospitality (THCC 214)Document9 pagesLearning Module Blended Flexible Learning: Macro Perspective of Tourism and Hospitality (THCC 214)MARITONI MEDALLA100% (1)

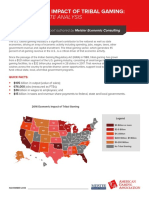

- Economic Impact of Tribal GamingDocument2 pagesEconomic Impact of Tribal GamingKJZZ PhoenixNo ratings yet

- Retail Property Insights 19, 2012Document47 pagesRetail Property Insights 19, 2012nhuacuja3551100% (1)

- Uber Case Study PDFDocument3 pagesUber Case Study PDFlakshay sharmaNo ratings yet

- Airport EIA Final ReportDocument20 pagesAirport EIA Final ReportMcKenzie StaufferNo ratings yet

- Economic Impact Study of The Clay Center For Arts and Sciences of West VirginiaDocument40 pagesEconomic Impact Study of The Clay Center For Arts and Sciences of West VirginiaMike SmithNo ratings yet

- Marshall Mountain Park - Professional Services Contract - SEG - EXECUTEDDocument15 pagesMarshall Mountain Park - Professional Services Contract - SEG - EXECUTEDNBC MontanaNo ratings yet

- Memphis Regional Megasite Economic ImpactDocument19 pagesMemphis Regional Megasite Economic ImpactThe Jackson SunNo ratings yet

- Economic Impact of Mexican Visitors Along the US-Mexico BorderDocument21 pagesEconomic Impact of Mexican Visitors Along the US-Mexico BorderCesar LoyaNo ratings yet

- Bowitz Economic ImpactsDocument8 pagesBowitz Economic ImpactsOlaya Pamela ParceroNo ratings yet

- Impact of World Cup On India 4oct2023Document4 pagesImpact of World Cup On India 4oct2023Keval RajparaNo ratings yet

- EMSI CCNY Economic Impact Report Executive SummaryDocument9 pagesEMSI CCNY Economic Impact Report Executive SummaryCCNY CommunicationsNo ratings yet

- Coca Cola in South Africa PDFDocument145 pagesCoca Cola in South Africa PDFbaby_tapnoiNo ratings yet

- THC 1 Module FinalDocument71 pagesTHC 1 Module Finalmisaki takahashiNo ratings yet

- 2018 Tesla Economic Impact StudyDocument12 pages2018 Tesla Economic Impact StudyFred Lamert100% (1)

- Economic Impact of TourismDocument22 pagesEconomic Impact of TourismFabforyou Collectionz100% (2)

- Summary Economic Impact Analysis NGA Relocation in North St. LouisDocument3 pagesSummary Economic Impact Analysis NGA Relocation in North St. LouisnextSTL.comNo ratings yet

- Finance Quiz Chapter 1-3Document44 pagesFinance Quiz Chapter 1-3DeLa RicheNo ratings yet

- Destination Canada Tourism Fact Sheet 2021 - EN-2Document2 pagesDestination Canada Tourism Fact Sheet 2021 - EN-2ゼンダー・No ratings yet

- NPS 2021 Visitor Spending EffectsDocument72 pagesNPS 2021 Visitor Spending EffectsShannon StowersNo ratings yet

- Tax+Alert+2023 1107 Pillar+Two+AnalysisDocument28 pagesTax+Alert+2023 1107 Pillar+Two+AnalysisTrương Minh ThắngNo ratings yet

- Sustainable Tourism Prelim Reviewer Topic 1 To 6 (Complete)Document12 pagesSustainable Tourism Prelim Reviewer Topic 1 To 6 (Complete)deniseangelarodrigoNo ratings yet

- 2014 Mentor Marina ReportDocument42 pages2014 Mentor Marina ReportThe News-HeraldNo ratings yet