You might also like

- IP law secures exclusive rights of inventorsDocument5 pagesIP law secures exclusive rights of inventorsKevin Ken Sison GancheroNo ratings yet

- Cta 2D CV 06681 D 2006aug31 Ref PDFDocument17 pagesCta 2D CV 06681 D 2006aug31 Ref PDFKevin Ken Sison GancheroNo ratings yet

- How To Properly Adjudicate DebatesDocument4 pagesHow To Properly Adjudicate DebatesKevin Ken Sison GancheroNo ratings yet

- Executive Poli KevDocument4 pagesExecutive Poli KevKevin Ken Sison GancheroNo ratings yet

- Until R8Document25 pagesUntil R8Kevin Ken Sison GancheroNo ratings yet

- 12 - New Filipino Maritime Agencies, Inc. vs. DatayanDocument17 pages12 - New Filipino Maritime Agencies, Inc. vs. DatayanKevin Ken Sison GancheroNo ratings yet

- 11 - Pinlac vs. PeopleDocument14 pages11 - Pinlac vs. PeopleKevin Ken Sison GancheroNo ratings yet

- Arraignment and PretrialDocument8 pagesArraignment and PretrialKevin Ken Sison Ganchero100% (1)

- Urgent MotionDocument2 pagesUrgent MotionKevin Ken Sison GancheroNo ratings yet

- TroDocument8 pagesTrokaiaceegeesNo ratings yet

- FCN US GermanyDocument27 pagesFCN US GermanyKevin Ken Sison GancheroNo ratings yet

- Castillo Castro E. Castro F. de Vera Fadera Fernando Frias Ganchero Lim RementinaDocument1 pageCastillo Castro E. Castro F. de Vera Fadera Fernando Frias Ganchero Lim RementinaKevin Ken Sison GancheroNo ratings yet

- Special Agreement: Jointly Notified To The Court On 12 September 2016Document22 pagesSpecial Agreement: Jointly Notified To The Court On 12 September 2016len_dy010487No ratings yet

- ALS TaxLawRevREMEDIES090610Document5 pagesALS TaxLawRevREMEDIES090610Dianna Louise Dela GuerraNo ratings yet

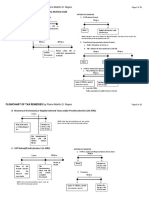

- Flowchart of Tax Remedies I. Remedies UnDocument12 pagesFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- Anzaldo vs. ClaveDocument7 pagesAnzaldo vs. ClaveKevin Ken Sison GancheroNo ratings yet

- NCBA ReviewerDocument8 pagesNCBA ReviewerKevin Ken Sison GancheroNo ratings yet

- Digests Ipl 9-9-16Document3 pagesDigests Ipl 9-9-16Kevin Ken Sison GancheroNo ratings yet

- Admin agencies' quasi-legislative power & A.O. No. 308Document2 pagesAdmin agencies' quasi-legislative power & A.O. No. 308Kevin Ken Sison GancheroNo ratings yet

- 04 Crisologo V SingsonDocument6 pages04 Crisologo V SingsonKevin Ken Sison GancheroNo ratings yet

- Managing Buried Treasure Across Frontiers: The International Law of Transboundary AquifersDocument11 pagesManaging Buried Treasure Across Frontiers: The International Law of Transboundary AquifersKevin Ken Sison GancheroNo ratings yet

- How To Properly Adjudicate DebatesDocument4 pagesHow To Properly Adjudicate DebatesKevin Ken Sison GancheroNo ratings yet

- Japan SocietyDocument34 pagesJapan SocietyKevin Ken Sison GancheroNo ratings yet

- Rule 39: Execution, Satisfaction and Effect of JudgmentsDocument26 pagesRule 39: Execution, Satisfaction and Effect of JudgmentsKevin Ken Sison GancheroNo ratings yet

- How To Properly Adjudicate DebatesDocument4 pagesHow To Properly Adjudicate DebatesKevin Ken Sison GancheroNo ratings yet

- LTD Consolidated Case DigestsDocument122 pagesLTD Consolidated Case DigestsKevin Ken Sison Ganchero100% (1)

- Oral Advocacy TipsDocument7 pagesOral Advocacy TipsShoaib KhanNo ratings yet

- Tax Law I: Nature of Income Madrigal V Rafferty Facts:: Divided Into 2 in Computing For The Additional Income TaxDocument2 pagesTax Law I: Nature of Income Madrigal V Rafferty Facts:: Divided Into 2 in Computing For The Additional Income TaxKevin Ken Sison GancheroNo ratings yet

- Income Taxation ReviewerDocument51 pagesIncome Taxation ReviewerKevin Ken Sison GancheroNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- BLTDocument30 pagesBLTJemson Yandug0% (1)

- Project (Main Body)Document78 pagesProject (Main Body)khansha ComputersNo ratings yet

- Polytechnic University of The Philippines: ST NDDocument10 pagesPolytechnic University of The Philippines: ST NDShania BuenaventuraNo ratings yet

- Chapter 15 PDFDocument14 pagesChapter 15 PDFAvox EverdeenNo ratings yet

- Franco FM Taxation 8Document4 pagesFranco FM Taxation 8pat patNo ratings yet

- Sample Assign From 2018 Student - Rated Excellent For AnalysisDocument11 pagesSample Assign From 2018 Student - Rated Excellent For AnalysisŁøuiša ŅøinñøiNo ratings yet

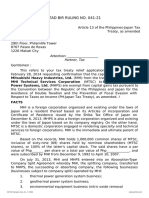

- Isla Lipana & Co., ITAD BIR Ruling No. 041-21 Dated September 29, 2021Document8 pagesIsla Lipana & Co., ITAD BIR Ruling No. 041-21 Dated September 29, 2021Carlota VillaromanNo ratings yet

- Xiii Xvi ReviewerDocument38 pagesXiii Xvi Reviewerjuna luz latigayNo ratings yet

- Chapter Three Accounting For Installment and Consignment SalsDocument25 pagesChapter Three Accounting For Installment and Consignment Salssenait eshetuNo ratings yet

- Income Taxation TableDocument11 pagesIncome Taxation TableRomela Eleria GasesNo ratings yet

- SCALP Handout 040Document2 pagesSCALP Handout 040Cher NaNo ratings yet

- Gross Income and Special CorporationsDocument4 pagesGross Income and Special CorporationsRosemarie CruzNo ratings yet

- Comprehensive Examination 1 TaxationDocument2 pagesComprehensive Examination 1 TaxationAlysa Sandra HizonNo ratings yet

- Itr3 PreviewDocument82 pagesItr3 PreviewAmit KumarNo ratings yet

- CIR v. PDI (Waiver)Document30 pagesCIR v. PDI (Waiver)Jerwin DaveNo ratings yet

- A. Powers To O. Rights of The AccusedDocument190 pagesA. Powers To O. Rights of The AccusedAiress Canoy CasimeroNo ratings yet

- 2 - CIR V Filinvest PDFDocument2 pages2 - CIR V Filinvest PDFSelynn CoNo ratings yet

- Net of Tax Meaning - Google SearchDocument1 pageNet of Tax Meaning - Google SearchEmmanuel ShaushiNo ratings yet

- Fin 254 Final ProjectDocument36 pagesFin 254 Final ProjectDpn BzNo ratings yet

- Projected IncomeDocument17 pagesProjected IncomecarlomaderazoNo ratings yet

- Intro to Income TaxDocument11 pagesIntro to Income TaxPrinces S. RoqueNo ratings yet

- Individual Taxpayer 1atax2Document21 pagesIndividual Taxpayer 1atax2Joneric RamosNo ratings yet

- 19b 20bDocument1 page19b 20bEzekiel T. MOSTIERONo ratings yet

- Note 8 - Tax Planning For CompaniesDocument9 pagesNote 8 - Tax Planning For CompaniesNur Dina AbsbNo ratings yet

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- Chapter 3, Fundamentals of Accounting IDocument76 pagesChapter 3, Fundamentals of Accounting IMustefa UsmaelNo ratings yet

- Clwtaxn - Lecture Week4Document17 pagesClwtaxn - Lecture Week4Maria Angelika ArcillaNo ratings yet

- RR 5-2021Document22 pagesRR 5-2021zelayneNo ratings yet

- Golpo 10 Task Performance 1.taxationDocument13 pagesGolpo 10 Task Performance 1.taxationNin JahNo ratings yet

- Installment Sales-: Loss On Repossession XXX Gain On Repossession XXXDocument5 pagesInstallment Sales-: Loss On Repossession XXX Gain On Repossession XXXJoyce Ann Agdippa BarcelonaNo ratings yet