You might also like

- Tax Process QuestionnaireDocument4 pagesTax Process QuestionnaireRodney LabayNo ratings yet

- Inventory Report 2021-FinalDocument19 pagesInventory Report 2021-FinalEngr Mohammad Al-AminNo ratings yet

- Branch Visit ChecklistDocument2 pagesBranch Visit ChecklistJerryNo ratings yet

- Index of HR PoliciesDocument1 pageIndex of HR PoliciesBIPINNo ratings yet

- Tender Waiver Form 2015Document6 pagesTender Waiver Form 2015ahtin618No ratings yet

- SOP For Container Deposits Refund ProcessDocument20 pagesSOP For Container Deposits Refund ProcessThana BalanNo ratings yet

- Human Resource ManagementDocument15 pagesHuman Resource ManagementAditiNo ratings yet

- Transfer PricingDocument53 pagesTransfer PricingkannnamreddyeswarNo ratings yet

- Recruitment and Selection Policy and ProceduresDocument4 pagesRecruitment and Selection Policy and ProceduresKhuzama ZafarNo ratings yet

- At 04 Auditing PlanningDocument8 pagesAt 04 Auditing PlanningJelyn RuazolNo ratings yet

- Receivables ChecklistDocument6 pagesReceivables ChecklistAngeliNo ratings yet

- Petty Cash Fund Guidelines and ProceduresDocument2 pagesPetty Cash Fund Guidelines and ProceduresIrish VargasNo ratings yet

- Tam C-DotDocument50 pagesTam C-DotRitwikRitzNo ratings yet

- Career Change Resignation LetterDocument1 pageCareer Change Resignation LetterAriYanisNo ratings yet

- Proposed Disbursement ProcessDocument4 pagesProposed Disbursement ProcessmarvinceledioNo ratings yet

- BPI-OTC Payment of Fee - 1 PDFDocument2 pagesBPI-OTC Payment of Fee - 1 PDFPhilip Ebersole100% (1)

- 19 Audit ChecklistDocument21 pages19 Audit ChecklistHarishSampangiNo ratings yet

- Marketing Plan TemplateDocument51 pagesMarketing Plan TemplateshuvashishNo ratings yet

- Financial Accounting - Ch06 - Finalisation EntriesDocument13 pagesFinancial Accounting - Ch06 - Finalisation EntriesRameshKumarMuraliNo ratings yet

- The Human Resources Audit Assessment: If Yes: If YesDocument5 pagesThe Human Resources Audit Assessment: If Yes: If YesRahul GoleNo ratings yet

- Management Representation AaaDocument3 pagesManagement Representation AaaFaizan AlhamdNo ratings yet

- Comments On COA-PETDocument1 pageComments On COA-PETAddy GuinalNo ratings yet

- Procurement Process & PolicyDocument52 pagesProcurement Process & PolicyHimanshu Kushwaha100% (1)

- Car Gas Consumption PolicyDocument7 pagesCar Gas Consumption PolicyDivine Grace MandinNo ratings yet

- Supplier Registration Form: Company InformationDocument3 pagesSupplier Registration Form: Company InformationMian Bilal Askari100% (1)

- Public Sector Companies (Corporate Governance Compliance) Guidelines, 2013Document8 pagesPublic Sector Companies (Corporate Governance Compliance) Guidelines, 2013wakhanNo ratings yet

- Background Check FormDocument4 pagesBackground Check FormJF Dan0% (1)

- 17.0 Dress Code PolicyDocument5 pages17.0 Dress Code PolicyRenny M PNo ratings yet

- Toc Test of ControlDocument47 pagesToc Test of ControlWilliam Christopher100% (1)

- PHC-BOA UpdatesDocument67 pagesPHC-BOA UpdatesMaynard Mirano100% (1)

- Clearance Form (To Be Completed Before Leaving)Document2 pagesClearance Form (To Be Completed Before Leaving)Tafadzwa Edson PasiNo ratings yet

- Fixed Assets Policy and Procedure ManualDocument60 pagesFixed Assets Policy and Procedure ManualArup DattaNo ratings yet

- NFA Merit Selection PlanDocument28 pagesNFA Merit Selection PlanPauline Caceres AbayaNo ratings yet

- Audit Programme - Order To CashDocument14 pagesAudit Programme - Order To CashTang SamNo ratings yet

- Audit Report ROPADocument10 pagesAudit Report ROPAgianneism100% (1)

- Depreciation Schedule ExampleDocument8 pagesDepreciation Schedule ExampleJenelyn PontiverosNo ratings yet

- Work ExperienceDocument2 pagesWork Experienceapi-384152146No ratings yet

- Internal Controls QuestionnaireDocument5 pagesInternal Controls QuestionnaireCarlos Eduardo C. da SilvaNo ratings yet

- Post Fixture ActivitiesDocument2 pagesPost Fixture Activitiessaikumar selaNo ratings yet

- Appointment of Members of Evaluation Committees Request For ProposalsDocument2 pagesAppointment of Members of Evaluation Committees Request For ProposalsKAMALUDDINNo ratings yet

- TD-HSE-FORM-003 Supplier Evaluation FormDocument4 pagesTD-HSE-FORM-003 Supplier Evaluation FormDamalie100% (1)

- Audit Programme and Checklists For Completion of Audit Audit ProgrammeDocument26 pagesAudit Programme and Checklists For Completion of Audit Audit ProgrammejafarNo ratings yet

- PCF PolicyDocument4 pagesPCF Policyking100% (1)

- UNIT 4 The Revenue Cycle Detailed Report BSA 2 1Document45 pagesUNIT 4 The Revenue Cycle Detailed Report BSA 2 1Harvey AguilarNo ratings yet

- IC Internal Audit Checklist 8624Document3 pagesIC Internal Audit Checklist 8624Tarun KumarNo ratings yet

- Prize Redemption FormDocument1 pagePrize Redemption FormRahul GuptaNo ratings yet

- Grievance CommitteeDocument6 pagesGrievance Committeeboopathi.n100% (1)

- Group-3 KRA & KPI-NEW PDFDocument12 pagesGroup-3 KRA & KPI-NEW PDFVishal KashyapNo ratings yet

- DOLE Monitoring of Compliance With JMC 20-04A Checklist As of 08 Jun 21Document4 pagesDOLE Monitoring of Compliance With JMC 20-04A Checklist As of 08 Jun 21Colleen Rose GuanteroNo ratings yet

- Audit Report Fil AsiaDocument2 pagesAudit Report Fil AsiaMarvin Celedio0% (1)

- KRA & KPIDocument2 pagesKRA & KPIPunkaj DubeyNo ratings yet

- Implementing A Procurement Internal Audit ProgramDocument10 pagesImplementing A Procurement Internal Audit ProgramFaruk H. IrmakNo ratings yet

- Tax Audit Checklist For The Revised Form 3CD: Part ADocument36 pagesTax Audit Checklist For The Revised Form 3CD: Part AKoolmindNo ratings yet

- Comprehensive InsuranceDocument8 pagesComprehensive InsuranceBebong VillanuevaNo ratings yet

- Health & Safety Procedural Manual Procedure For Internal Audits MNE/OHS/P04Document3 pagesHealth & Safety Procedural Manual Procedure For Internal Audits MNE/OHS/P04Richu PaliNo ratings yet

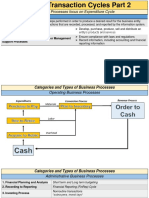

- AT 06-07 Transaction Cycles Part 2Document12 pagesAT 06-07 Transaction Cycles Part 2EeuhNo ratings yet

- Modul 5 Auditing2Document14 pagesModul 5 Auditing2maeNo ratings yet

- Purchase and Disbursement CycleDocument30 pagesPurchase and Disbursement CycleVenus Lyka LomocsoNo ratings yet

- JKR ATJ2C-85 (Pindaan2017) - 5 - 12Document135 pagesJKR ATJ2C-85 (Pindaan2017) - 5 - 12Nurul Syafiqah Ghazali100% (3)

- Chapter 1Document12 pagesChapter 1Na'Tashia Nicole HendersonNo ratings yet

- CFAS Reviewer - Module 1 & 2Document12 pagesCFAS Reviewer - Module 1 & 2Lizette Janiya SumantingNo ratings yet

- MB Lal CommitteeDocument23 pagesMB Lal CommitteechemsaneNo ratings yet

- The 12 Best Practices in Contract ManagementDocument21 pagesThe 12 Best Practices in Contract ManagementomerumeromerNo ratings yet

- Orion Pharma Limited Integrated Annual Report 2019-20 PDFDocument340 pagesOrion Pharma Limited Integrated Annual Report 2019-20 PDFFouzia FarihaNo ratings yet

- Handramohan Akshmipathy: ENIOR Quality Professional - Nearly 26 Years of ExperienceDocument5 pagesHandramohan Akshmipathy: ENIOR Quality Professional - Nearly 26 Years of ExperienceANIL PLAMOOTTILNo ratings yet

- 39 QC Job DescriptionDocument24 pages39 QC Job DescriptionAli YudiNo ratings yet

- Pengawasan Era 4.0Document23 pagesPengawasan Era 4.0bnkp thomasNo ratings yet

- TES-AMM (Singapore) Pte. LTD.: Company Registration No. 200508881RDocument43 pagesTES-AMM (Singapore) Pte. LTD.: Company Registration No. 200508881RJoyce ChongNo ratings yet

- BCB 101 - Accreditation Criteria - QMSDocument4 pagesBCB 101 - Accreditation Criteria - QMSAhammad Niyas kNo ratings yet

- Sample Letter For Audit ServicesDocument2 pagesSample Letter For Audit Servicesbaby100% (2)

- Audit Report in Case of Non Statutionry and Non Profit OrgDocument5 pagesAudit Report in Case of Non Statutionry and Non Profit OrgVIJAY PAREEKNo ratings yet

- Iso 27001Document100 pagesIso 27001Marek Sulich100% (1)

- Inspector General's Report On Chicago's Buildings DepartmentDocument43 pagesInspector General's Report On Chicago's Buildings DepartmentMitch ArmentroutNo ratings yet

- Clinical Audit For Medical StudentsDocument6 pagesClinical Audit For Medical StudentsAmal SaeedNo ratings yet

- Board ManualDocument5 pagesBoard ManualTwite_Daniel2No ratings yet

- Procedures For On-Site EvaluationDocument7 pagesProcedures For On-Site EvaluationEnes BuladıNo ratings yet

- Paul Klenk EA ResumeDocument2 pagesPaul Klenk EA ResumepaulklenkNo ratings yet

- The Mosaic VisionDocument27 pagesThe Mosaic VisionherbsyNo ratings yet

- Olfu Integrated PPT Auditing Assurance Concepts and ApplicationsDocument12 pagesOlfu Integrated PPT Auditing Assurance Concepts and ApplicationsGenesis Anne MagsicoNo ratings yet

- Auditing in The Maritime Industry: A Case Study of The Offshore Support Vessel SegmentDocument15 pagesAuditing in The Maritime Industry: A Case Study of The Offshore Support Vessel Segmentbehera2001No ratings yet

- 12 TransGrid Risk Management FrameworkDocument22 pages12 TransGrid Risk Management FrameworkDavid CheishviliNo ratings yet

- GAC02A2 2018 AO1 Suggested SolutionDocument11 pagesGAC02A2 2018 AO1 Suggested SolutionNandi MliloNo ratings yet

- IATF 16949:2016: Transition OverviewDocument7 pagesIATF 16949:2016: Transition OverviewIrwansyah Zaidan100% (1)

- Engagement Partner Review ChecklistDocument5 pagesEngagement Partner Review ChecklistHARSHA REDDYNo ratings yet

- Looting With Putin: How City of London Suits Joined The Moscow Gold RushDocument6 pagesLooting With Putin: How City of London Suits Joined The Moscow Gold RushhavanurNo ratings yet

- The Philippine Institute of Certified Public AccountantsDocument1 pageThe Philippine Institute of Certified Public AccountantsLuzz LandichoNo ratings yet

- Auditing Standards and Auditors Performance1Document7 pagesAuditing Standards and Auditors Performance1alfikooNo ratings yet

- Oceana Group Limited - Executive Summary of Forensic Investigation FindingsDocument7 pagesOceana Group Limited - Executive Summary of Forensic Investigation FindingshyenadogNo ratings yet