You might also like

- Understanding AccountingDocument20 pagesUnderstanding Accountingrainman54321No ratings yet

- Posting in AccountingDocument9 pagesPosting in AccountingSanaa MohammedNo ratings yet

- The Cash Flow StatementsDocument13 pagesThe Cash Flow Statementsdeo omachNo ratings yet

- Finance For Non-Financial ManagerDocument23 pagesFinance For Non-Financial ManagerMahrous100% (7)

- Fundamentals 02 Accounting Interview QuestionsDocument37 pagesFundamentals 02 Accounting Interview Questionsnatalia.velianoskiNo ratings yet

- Bookkeeping Is The Recording of Financial Transactions. Transactions Include SalesDocument247 pagesBookkeeping Is The Recording of Financial Transactions. Transactions Include SalesSantosh PanigrahiNo ratings yet

- StarFarm Finance OfficerDocument7 pagesStarFarm Finance OfficerZany KhanNo ratings yet

- Review of The Accounting ProcessDocument18 pagesReview of The Accounting ProcessRoyceNo ratings yet

- Prepare Basic Financial StatementsDocument6 pagesPrepare Basic Financial StatementsMujieh NkengNo ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- JournalizationDocument36 pagesJournalizationDavid Guerrero Terrado100% (1)

- Bank ReconciliationDocument4 pagesBank Reconciliationknowledge musendekwaNo ratings yet

- Key financial reporting explainedDocument11 pagesKey financial reporting explainedhemanth727100% (1)

- Module 3 CFAS PDFDocument7 pagesModule 3 CFAS PDFErmelyn GayoNo ratings yet

- Accounting Payroll Services 1Document18 pagesAccounting Payroll Services 1Donna MarieNo ratings yet

- Faa U2Document10 pagesFaa U2kztrmfbc8wNo ratings yet

- SWIFT Payment GuideDocument7 pagesSWIFT Payment GuideZany KhanNo ratings yet

- General Ledger Reconciliations Guide Business Owners (39Document11 pagesGeneral Ledger Reconciliations Guide Business Owners (39Sherin ThomasNo ratings yet

- JKWCPA Accounting 101 For Small Businesses EGuideDocument13 pagesJKWCPA Accounting 101 For Small Businesses EGuideAlthaf CassimNo ratings yet

- Basic Accounting LectureDocument56 pagesBasic Accounting LectureJun Guerzon PaneloNo ratings yet

- Basic Accounting Concepts and PrinciplesDocument4 pagesBasic Accounting Concepts and Principlesalmyr_rimando100% (1)

- AccountingDocument44 pagesAccountingPrasith baskyNo ratings yet

- Accounting NotesDocument66 pagesAccounting NotesShashank Gadia71% (17)

- Accounting Survival Guide: An Introduction to Accounting for BeginnersFrom EverandAccounting Survival Guide: An Introduction to Accounting for BeginnersNo ratings yet

- Reporting Comprehensive Income, Equity Changes, and Key Financial StatementsDocument9 pagesReporting Comprehensive Income, Equity Changes, and Key Financial StatementsAbigail Elsa Samita Sitakar 1902113687No ratings yet

- Chapter-2 Intainship ProjectDocument8 pagesChapter-2 Intainship ProjectAP GREEN ENERGY CORPORATION LIMITEDNo ratings yet

- Trial Balance Guide: What is a Trial Balance and How to Prepare OneDocument20 pagesTrial Balance Guide: What is a Trial Balance and How to Prepare OneVikrant DityaNo ratings yet

- Unit 3 Assignment 2 Task 2Document4 pagesUnit 3 Assignment 2 Task 2Noor KilaniNo ratings yet

- Accounting overview for studentsDocument11 pagesAccounting overview for studentsCindy TorresNo ratings yet

- Financial Statement Analysis For Cash Flow StatementDocument5 pagesFinancial Statement Analysis For Cash Flow StatementOld School Value100% (3)

- Tally Ebook For BeginnerDocument39 pagesTally Ebook For Beginnerramaisgod88% (25)

- Accounting Records and System: The Chart of Accounts Debit and Credit The Accounting Process Transaction AnalysisDocument27 pagesAccounting Records and System: The Chart of Accounts Debit and Credit The Accounting Process Transaction Analysiscluadine dineros100% (1)

- How To Prepare Balance SheetDocument5 pagesHow To Prepare Balance SheetSIddharth CHoudharyNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- The Role of Accounting in BusinessDocument18 pagesThe Role of Accounting in BusinessJawad AzizNo ratings yet

- Financial Fraud SchemesDocument9 pagesFinancial Fraud SchemesPrabhu SachuNo ratings yet

- Accounting Worksheet and Financial StatementsDocument12 pagesAccounting Worksheet and Financial StatementsChona MarcosNo ratings yet

- Bookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthFrom EverandBookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthNo ratings yet

- Accounting KnowledgeDocument6 pagesAccounting KnowledgeAung TikeNo ratings yet

- What Is An Extended TrialDocument19 pagesWhat Is An Extended TrialocalmaviliNo ratings yet

- Sulema InglesDocument11 pagesSulema InglesBanmer AjanelNo ratings yet

- Tally 9Document18 pagesTally 9Romendro ThokchomNo ratings yet

- Accounting OverviewDocument13 pagesAccounting OverviewMae AroganteNo ratings yet

- Lesson 16: Accounting Practice SetDocument47 pagesLesson 16: Accounting Practice SetMai Ruiz100% (1)

- Module 6 - Worksheet and Financial Statements Part IDocument12 pagesModule 6 - Worksheet and Financial Statements Part IMJ San Pedro100% (1)

- Bookeeping EntrepDocument71 pagesBookeeping EntrepJanelle Ghia RamosNo ratings yet

- Financial AccountingDocument5 pagesFinancial AccountingRiza CabellezaNo ratings yet

- GHANA COMMUNICATION TECHNOLOGY UNIVERSITY ACCOUNTING CYCLEDocument7 pagesGHANA COMMUNICATION TECHNOLOGY UNIVERSITY ACCOUNTING CYCLEYano NettleNo ratings yet

- Econ 303Document5 pagesEcon 303ali abou aliNo ratings yet

- The Post Of Trial Balance (Bing)Document5 pagesThe Post Of Trial Balance (Bing)rezarenonnNo ratings yet

- The Principles and History of Accounting: Block ReviewDocument88 pagesThe Principles and History of Accounting: Block ReviewLlora Jane GuillermoNo ratings yet

- Preparation TB and BSDocument21 pagesPreparation TB and BSMarites Domingo - Paquibulan100% (1)

- Management Accounting Jargons/ Key TerminologiesDocument11 pagesManagement Accounting Jargons/ Key Terminologiesnimbus2050No ratings yet

- Trial Balance & Accounting ConceptsDocument32 pagesTrial Balance & Accounting ConceptsPaul Ayoma100% (1)

- Concept and Meaning of Trial BalanceDocument3 pagesConcept and Meaning of Trial BalanceJAY PATELNo ratings yet

- So, You Want To Learn Bookkeeping! Lesson 5: The General Ledger and JournalsDocument15 pagesSo, You Want To Learn Bookkeeping! Lesson 5: The General Ledger and JournalsJamelenFloroCodillaGuzonNo ratings yet

- General Ledger Default AccountsDocument4 pagesGeneral Ledger Default AccountsAhmed ElghannamNo ratings yet

- Cash Flow StatementDocument20 pagesCash Flow StatementKarthik Balaji100% (1)

- Case Product CostingDocument3 pagesCase Product CostingSatesh KalimuthuNo ratings yet

- F&N Eyes New Market Opportunities: Corporate NewsDocument2 pagesF&N Eyes New Market Opportunities: Corporate NewsSatesh KalimuthuNo ratings yet

- WbsDocument2 pagesWbsSatesh KalimuthuNo ratings yet

- KHINDDocument21 pagesKHINDSatesh Kalimuthu33% (3)

- RatiosDocument3 pagesRatiosSatesh Kalimuthu100% (1)

- YTL Buys Rival Lafarge Malaysia: Corporate NewsDocument3 pagesYTL Buys Rival Lafarge Malaysia: Corporate NewsSatesh KalimuthuNo ratings yet

- SFL Aims To Build Malaysia's First Durian ConfectionaryDocument2 pagesSFL Aims To Build Malaysia's First Durian ConfectionarySatesh KalimuthuNo ratings yet

- Case Study Nike, Inc. - Cost of CapitalDocument6 pagesCase Study Nike, Inc. - Cost of Capitalabrown5_csustan100% (2)

- Short Essay 1: UnrestrictedDocument8 pagesShort Essay 1: UnrestrictedSatesh KalimuthuNo ratings yet

- IIIDocument910 pagesIIISatesh KalimuthuNo ratings yet

- 2011pbfeam 112Document33 pages2011pbfeam 112Akbar Shara FujiNo ratings yet

- Experian MaidsDocument2 pagesExperian MaidsSatesh KalimuthuNo ratings yet

- COMPANYDocument16 pagesCOMPANYSatesh KalimuthuNo ratings yet

- Question 1 MFRS 108 AnswerDocument1 pageQuestion 1 MFRS 108 AnswerSatesh KalimuthuNo ratings yet

- Chapter 1 - Foundations of Engineering EconomyDocument28 pagesChapter 1 - Foundations of Engineering EconomyJohn Joshua MontañezNo ratings yet

- Astral Records LTD., North America: Some Financial Concerns: October 2008Document11 pagesAstral Records LTD., North America: Some Financial Concerns: October 2008MbavhaleloNo ratings yet

- Capital Gains Tax Questions AnsweredDocument4 pagesCapital Gains Tax Questions AnsweredRedfield GrahamNo ratings yet

- Fin623 Solved MCQs For EamsDocument24 pagesFin623 Solved MCQs For EamsSohail Merchant79% (14)

- Taxation (Romania) : Tuesday 12 June 2012Document12 pagesTaxation (Romania) : Tuesday 12 June 2012anytta_24No ratings yet

- Free Cash FlowDocument6 pagesFree Cash FlowAnh KietNo ratings yet

- Suggested Answer CAP I 2009Document81 pagesSuggested Answer CAP I 2009Meghraj AryalNo ratings yet

- Iscal EARDocument311 pagesIscal EARDjalma MoreiraNo ratings yet

- Financial Management Strategy FinalDocument24 pagesFinancial Management Strategy FinalsayedhossainNo ratings yet

- Dilemma Company Financial Position Statement 2021Document2 pagesDilemma Company Financial Position Statement 2021lizzie patauegNo ratings yet

- Project Number: 1: Submitted To: Prof. Dennis RagauskasDocument5 pagesProject Number: 1: Submitted To: Prof. Dennis RagauskasDilrajSinghNo ratings yet

- Introduction To Securities & Investments: Financial Services Industry - IntroductionDocument5 pagesIntroduction To Securities & Investments: Financial Services Industry - IntroductionJohn Dale VacaroNo ratings yet

- Treasury ManagementDocument10 pagesTreasury ManagementHarshit GoyalNo ratings yet

- Black Book On Direct Tax EffectDocument49 pagesBlack Book On Direct Tax Effectshiakhrustam621No ratings yet

- Cheque Introduction: A Cheque Is A Document of Very Great Importance in TheDocument13 pagesCheque Introduction: A Cheque Is A Document of Very Great Importance in The777priyankaNo ratings yet

- Stock Audit ReportDocument46 pagesStock Audit ReportGmd NizamNo ratings yet

- New Anand PharmaDocument1 pageNew Anand PharmaShri Rani Sati officeNo ratings yet

- BLKL 5 Banking Industry and StructureDocument21 pagesBLKL 5 Banking Industry and Structurelinda kartikaNo ratings yet

- Financial Performance Analysis of TJSB Sahakari Bank Ltd.Document12 pagesFinancial Performance Analysis of TJSB Sahakari Bank Ltd.Yash KhairnarNo ratings yet

- 29 06 Main TradingDocument14 pages29 06 Main TradingZahir Khan100% (1)

- 02 Financial Statements Case StudyDocument3 pages02 Financial Statements Case StudyanitalauymNo ratings yet

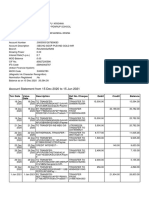

- Account statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021Document9 pagesAccount statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021SRINIVASARAO JONNALANo ratings yet

- FILE GIẢI SÁCH READING TOTAL-đã chuyển đổiDocument23 pagesFILE GIẢI SÁCH READING TOTAL-đã chuyển đổiNhư QuỳnhNo ratings yet

- Personal Financial Planning 2nd Edition Altfest Test BankDocument11 pagesPersonal Financial Planning 2nd Edition Altfest Test Bankcynthia100% (23)

- Case Study Nike, Inc. - Cost of CapitalDocument6 pagesCase Study Nike, Inc. - Cost of Capitalabrown5_csustan100% (2)

- Financial ManagementDocument34 pagesFinancial ManagementAbisellyNo ratings yet

- Reviewer - ParCorDocument13 pagesReviewer - ParCoramiNo ratings yet

- Balance Sheet of Kansai Nerolac PaintsDocument5 pagesBalance Sheet of Kansai Nerolac Paintssunilkumar978No ratings yet

- Cambridge Assessment International Education: Accounting 0452/22 October/November 2017Document12 pagesCambridge Assessment International Education: Accounting 0452/22 October/November 2017pyaaraasingh716No ratings yet

- EVA and NPV valuation methods comparisonDocument16 pagesEVA and NPV valuation methods comparisonJosh SmithNo ratings yet