You might also like

- Disini v. Secretary of Justice, G.R. No. 203335, Feb. 11, 2014Document34 pagesDisini v. Secretary of Justice, G.R. No. 203335, Feb. 11, 2014Yves Tristan MenesesNo ratings yet

- SPA Corp.Document1 pageSPA Corp.cherry ongsonNo ratings yet

- CAS-Electronic DocumentsDocument1 pageCAS-Electronic Documentscherry ongsonNo ratings yet

- Relevant Rules During Tax AuditDocument2 pagesRelevant Rules During Tax Auditcherry ongsonNo ratings yet

- Transfer From HO To BRANCHDocument1 pageTransfer From HO To BRANCHcherry ongsonNo ratings yet

- TRAINDocument1 pageTRAINcherry ongsonNo ratings yet

- Private Retirement Benefit Plan RegulationDocument2 pagesPrivate Retirement Benefit Plan Regulationcherry ongsonNo ratings yet

- Asssessment ProcessDocument2 pagesAsssessment Processcherry ongsonNo ratings yet

- Advisory - Unavailability 1601EQ and 1601FQDocument1 pageAdvisory - Unavailability 1601EQ and 1601FQzadmirNo ratings yet

- SB 2059 PDFDocument33 pagesSB 2059 PDFcherry ongsonNo ratings yet

- Revenue Memorandum Order No. 10-2019 Foreign MissionariesDocument2 pagesRevenue Memorandum Order No. 10-2019 Foreign MissionariesCherry Amor OngsonNo ratings yet

- HB 8554Document15 pagesHB 8554cherry ongsonNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Special Terms and Conditions of RFQ SummaryDocument14 pagesSpecial Terms and Conditions of RFQ SummaryKarandeep SinghNo ratings yet

- Case DigestDocument7 pagesCase DigestGabriel Jhick SaliwanNo ratings yet

- GST Questions and ConceptsDocument52 pagesGST Questions and ConceptsShefali TailorNo ratings yet

- Final Report On The Audit of Peace Corps Panama IG-18-01-ADocument32 pagesFinal Report On The Audit of Peace Corps Panama IG-18-01-AAccessible Journal Media: Peace Corps DocumentsNo ratings yet

- Moot Problem Civil B.A.LL.B., B.B.A.LL.B., LL.B.Document15 pagesMoot Problem Civil B.A.LL.B., B.B.A.LL.B., LL.B.ishitaNo ratings yet

- L.R. & S.M. Vissanji Academy Secondary Section 2022-23 Preliminary Exam 1Document6 pagesL.R. & S.M. Vissanji Academy Secondary Section 2022-23 Preliminary Exam 1Sneh BhalodiaNo ratings yet

- EMEA Groupon Goods Marketplace ContractDocument11 pagesEMEA Groupon Goods Marketplace Contractcoach djunaediNo ratings yet

- Mba 3 Sem Tax Planning and Management Kmbfm02 2020Document2 pagesMba 3 Sem Tax Planning and Management Kmbfm02 2020Vinod GuptaNo ratings yet

- Curriculum For BSADocument5 pagesCurriculum For BSAEphreen Grace MartyNo ratings yet

- Amount of Net Taxable Income Rate Over But Not OverDocument1 pageAmount of Net Taxable Income Rate Over But Not OverDennah Faye SabellinaNo ratings yet

- TAX 42 - Exempt Sales GuideDocument10 pagesTAX 42 - Exempt Sales GuideEJ EduqueNo ratings yet

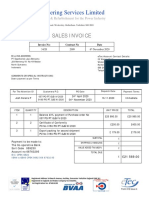

- Etec Engineering Services Limited: Sales InvoiceDocument1 pageEtec Engineering Services Limited: Sales InvoiceReedNo ratings yet

- IMEX Show Catalogue 2015 Low ResDocument314 pagesIMEX Show Catalogue 2015 Low ResMeghana VyasNo ratings yet

- CE CASECNAN WATER AND ENERGY COMPANY INC. vs. CIRDocument6 pagesCE CASECNAN WATER AND ENERGY COMPANY INC. vs. CIRJaysonNo ratings yet

- Vat Refund-Diplomats, International Agencies - Foreign Aided ProjectsDocument11 pagesVat Refund-Diplomats, International Agencies - Foreign Aided ProjectsnepalcaNo ratings yet

- REF/SIM/17092022!1.3: Corp. Off. A-37, Sector-60, NOIDA-201301 India, Tel.: (+91) 120 66880000, Fax: (+91) 120 6688014Document3 pagesREF/SIM/17092022!1.3: Corp. Off. A-37, Sector-60, NOIDA-201301 India, Tel.: (+91) 120 66880000, Fax: (+91) 120 6688014Sumit PandeyNo ratings yet

- "Commissioner of Internal Revenue v. San Roque Power Corporation, G.R. No. 187485, 8 October 2013Document1 page"Commissioner of Internal Revenue v. San Roque Power Corporation, G.R. No. 187485, 8 October 2013chescasantosNo ratings yet

- Tax Invoice for Kindle and Cover PurchaseDocument2 pagesTax Invoice for Kindle and Cover PurchaseAmit rajNo ratings yet

- McKnight's Pub Brew ConnoisseurDocument45 pagesMcKnight's Pub Brew ConnoisseurLesh GaleonneNo ratings yet

- Taxation Digest on VAT LiabilityDocument27 pagesTaxation Digest on VAT LiabilityBer Sib JosNo ratings yet

- Di New Pattern BFPDocument245 pagesDi New Pattern BFPDeepak LohiaNo ratings yet

- Underground Power Network UpgradeDocument30 pagesUnderground Power Network UpgradeKuldeep KumarNo ratings yet

- Shoe and Reaches Below Knee.: Hospital RatnagiriDocument25 pagesShoe and Reaches Below Knee.: Hospital RatnagiriNeelNo ratings yet

- Appointment of A Service Provider TO Supply and Deliver Np43S Plate Compactor RFQ (DPW H19/088 QI)Document5 pagesAppointment of A Service Provider TO Supply and Deliver Np43S Plate Compactor RFQ (DPW H19/088 QI)bubele pamlaNo ratings yet

- 9.3.11 (C) Structural Eng Fees Calculator For Multi-Disciplinary Projects - 2013 Fee ScalesDocument64 pages9.3.11 (C) Structural Eng Fees Calculator For Multi-Disciplinary Projects - 2013 Fee ScalesForbes Kamba100% (1)

- The Real Estate Law Review 8th EditionDocument388 pagesThe Real Estate Law Review 8th EditionLaudArch100% (2)

- Bill of Supply/Cash Receipt: (Please Bring This Receipt For Report Collection)Document2 pagesBill of Supply/Cash Receipt: (Please Bring This Receipt For Report Collection)manav lakhanpalNo ratings yet

- HIL Limited - Project Order Approval Form: Babulal & CompanyDocument2 pagesHIL Limited - Project Order Approval Form: Babulal & CompanyRavinandan KumarNo ratings yet

- Diah Rizkyan DewiDocument6 pagesDiah Rizkyan DewiAnastasia FoekNo ratings yet

- ABS-CBN Exempt from Quezon City Franchise TaxDocument14 pagesABS-CBN Exempt from Quezon City Franchise Taxmb_estanislaoNo ratings yet