You might also like

- Balance Sheet GuideDocument8 pagesBalance Sheet GuideDeepakHeikrujamNo ratings yet

- Accounting ReviewDocument63 pagesAccounting ReviewLee ChiaNo ratings yet

- Financial Statment AnalysisDocument9 pagesFinancial Statment AnalysisPraween BimsaraNo ratings yet

- Ratio Analysis: Dattaraj D. KarwarkerDocument39 pagesRatio Analysis: Dattaraj D. KarwarkerSarvesh KamatNo ratings yet

- Ratioanalyis Fred 140124075834 Phpapp02Document27 pagesRatioanalyis Fred 140124075834 Phpapp02Neo MothaoNo ratings yet

- Impact of Liquidity On ProfitabilityDocument44 pagesImpact of Liquidity On ProfitabilityRavi ShankarNo ratings yet

- Chapter 2 - 211031 - 121711Document34 pagesChapter 2 - 211031 - 121711CY YangNo ratings yet

- Ratio Analysis GuideDocument20 pagesRatio Analysis Guideanurag6866No ratings yet

- Assets and LiabilitiesDocument4 pagesAssets and LiabilitiesmoganNo ratings yet

- S2 3.analyze - Balance - SheetDocument16 pagesS2 3.analyze - Balance - SheetLimberg IllanesNo ratings yet

- OF Financial Statement: Dr. Quang NguyenDocument56 pagesOF Financial Statement: Dr. Quang NguyenQuang NguyễnNo ratings yet

- Task 2Document18 pagesTask 2Yashmi BhanderiNo ratings yet

- Chapter 3Document39 pagesChapter 3Hibaaq AxmedNo ratings yet

- Classification of RatiosDocument25 pagesClassification of RatiosAnonymous XZ376GGmNo ratings yet

- Chapter - 1 Working Capital Management - Introduction 1.1Document41 pagesChapter - 1 Working Capital Management - Introduction 1.1ChetanNo ratings yet

- Bus 505 - Final Exam Assignment - Umama Alam - 2125119660Document22 pagesBus 505 - Final Exam Assignment - Umama Alam - 2125119660Shiny StarNo ratings yet

- Chapter5 Summary Financial Statement Analysis-IIDocument11 pagesChapter5 Summary Financial Statement Analysis-IIkyungsooNo ratings yet

- Cash Flow and Funds FlowDocument17 pagesCash Flow and Funds FlowNitinNo ratings yet

- Ratio Analysis: Theory and ProblemsDocument51 pagesRatio Analysis: Theory and ProblemsAnit Jacob Philip100% (1)

- Chapter2 0Document56 pagesChapter2 0Eaindray OoNo ratings yet

- Objectives of Managerial Accounting ActivityDocument8 pagesObjectives of Managerial Accounting ActivitynishabilochiNo ratings yet

- Ratio AnalysisDocument113 pagesRatio AnalysisDevyansh GuptaNo ratings yet

- Chapter OneDocument24 pagesChapter OneffahddmmNo ratings yet

- Business Finance IIDocument73 pagesBusiness Finance IIyakubu I saidNo ratings yet

- Accounting concepts and financial statementsDocument135 pagesAccounting concepts and financial statementsDesi TVNo ratings yet

- Ratio AnalysisDocument39 pagesRatio AnalysisUmeshwari Rathore100% (1)

- Financialfeasibility 200129141325Document20 pagesFinancialfeasibility 200129141325Princess BaybayNo ratings yet

- Beginner Notes.Document157 pagesBeginner Notes.Varsha SinghNo ratings yet

- 0. Beginner Notes.Document157 pages0. Beginner Notes.nandinisonar05No ratings yet

- Actg1 - Chapter 3Document37 pagesActg1 - Chapter 3Reynaleen Agta100% (1)

- UNIT FOURDocument29 pagesUNIT FOURyimenueyassuNo ratings yet

- Hero Honda Motors: Submitted To: Professor Seema DograDocument19 pagesHero Honda Motors: Submitted To: Professor Seema Dograpriyankagrawal7No ratings yet

- Session 3Document13 pagesSession 3officialwork684No ratings yet

- Chap 3 Problem SolutionsDocument31 pagesChap 3 Problem SolutionsAhmed FahmyNo ratings yet

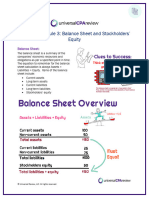

- Chapter 1 Module 3: Balance Sheet and Stockholders' EquityDocument6 pagesChapter 1 Module 3: Balance Sheet and Stockholders' Equityhmaz.roid91No ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Fund Flow AnalysisDocument20 pagesFund Flow AnalysisSoumya DakshNo ratings yet

- CHAPTER 3 NOTESDocument3 pagesCHAPTER 3 NOTESLeonardo WenceslaoNo ratings yet

- Finanacial Ratio AnalysisDocument39 pagesFinanacial Ratio AnalysisnurulNo ratings yet

- Forecast Financial Statements For Your New BusinessDocument15 pagesForecast Financial Statements For Your New BusinessBill Taylor100% (1)

- Financial Ratio AnalysisDocument11 pagesFinancial Ratio Analysispradeep100% (5)

- Balance Sheets and Its ConceptsDocument34 pagesBalance Sheets and Its ConceptsKamal KantNo ratings yet

- Balance SheetDocument11 pagesBalance SheetVilexy NuñezNo ratings yet

- Chapter 3 Solutions & NotesDocument17 pagesChapter 3 Solutions & NotesStudy PinkNo ratings yet

- Fabm 2Document5 pagesFabm 2Robillos FaithNo ratings yet

- Financial Statement AnalysisDocument33 pagesFinancial Statement AnalysisAriela Davis100% (1)

- Financial Reporting & Analysis in 40 CharactersDocument31 pagesFinancial Reporting & Analysis in 40 CharactersAbinash MishraNo ratings yet

- Financial Statement AnalysisDocument33 pagesFinancial Statement Analysisfirst name100% (3)

- Lecture No.2 Financial Statements AnalysisDocument17 pagesLecture No.2 Financial Statements AnalysisSokoine Hamad Denis100% (1)

- FINANCIAL RATIO ANALYSISDocument25 pagesFINANCIAL RATIO ANALYSISWong Siu CheongNo ratings yet

- MS_3609_Financial_Statements_AnalysisDocument6 pagesMS_3609_Financial_Statements_Analysisrichshielanghag627No ratings yet

- Statement of Financial Position: Fundamentals of Accountancy, Business and Management 2Document55 pagesStatement of Financial Position: Fundamentals of Accountancy, Business and Management 2Arminda Villamin75% (4)

- Balance SheetDocument24 pagesBalance SheetGnanasekar ThirugnanamNo ratings yet

- Dr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, IncDocument7 pagesDr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, IncWarriorNo ratings yet

- Fin 12 Notes Chapter 3 UpdatedDocument4 pagesFin 12 Notes Chapter 3 UpdatedKaycee StylesNo ratings yet

- Dr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, IncDocument7 pagesDr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, IncWarriorNo ratings yet

- Financial MeasuresDocument7 pagesFinancial MeasuresAndra SomodungNo ratings yet

- Acknowledgments: 80 Sme Mining Engineering HandbookDocument1 pageAcknowledgments: 80 Sme Mining Engineering HandbookYeimsNo ratings yet

- FS Analysis GuideDocument4 pagesFS Analysis GuideHaks MashtiNo ratings yet

- Matrimonial Resume CVDocument3 pagesMatrimonial Resume CVpunitatvsnNo ratings yet

- Marriage Biodata Doc Word Formate ResumeDocument2 pagesMarriage Biodata Doc Word Formate ResumeJoy Friend55% (306)

- ONGC Recruitment 70812Document7 pagesONGC Recruitment 70812admin2772No ratings yet

- Glossary of Finance Terms1Document5 pagesGlossary of Finance Terms1punitatvsnNo ratings yet

- Ongc ChallanDocument1 pageOngc ChallanArchika Kaushik100% (1)

- Economic Planning of India-ReportDocument90 pagesEconomic Planning of India-Reportpunitatvsn100% (2)

- Pet CokeDocument2 pagesPet CokepunitatvsnNo ratings yet

- How Inflation Affect The Consumer in IndiaDocument240 pagesHow Inflation Affect The Consumer in IndiapunitatvsnNo ratings yet

- Chapter Two: A Market That Has No One Specific Location Is Termed A (N) - MarketDocument9 pagesChapter Two: A Market That Has No One Specific Location Is Termed A (N) - MarketAsif HossainNo ratings yet

- Mupila V Yu Wei (COMPIRCLK 222 of 2021) (2022) ZMIC 3 (02 March 2022)Document31 pagesMupila V Yu Wei (COMPIRCLK 222 of 2021) (2022) ZMIC 3 (02 March 2022)Angelina mwakamuiNo ratings yet

- The Three Principles of The CovenantsDocument3 pagesThe Three Principles of The CovenantsMarcos C. Thaler100% (1)

- Khilafat Movement 1919 1924Document4 pagesKhilafat Movement 1919 1924obaidNo ratings yet

- Module 2 - Part III - UpdatedDocument38 pagesModule 2 - Part III - UpdatedDhriti NayyarNo ratings yet

- Memorandum of AgreementDocument4 pagesMemorandum of AgreementCavite PrintingNo ratings yet

- Postgraduate Application Form UPDATEDDocument4 pagesPostgraduate Application Form UPDATEDNYANGWESO KEVINNo ratings yet

- Tax 3 Mid Term 2016-2017 - RawDocument16 pagesTax 3 Mid Term 2016-2017 - RawPandaNo ratings yet

- Digos Central Adventist Academy, IncDocument3 pagesDigos Central Adventist Academy, IncPeter John IntapayaNo ratings yet

- Release Vehicle Motion Philippines Theft CaseDocument3 pagesRelease Vehicle Motion Philippines Theft Caseczabina fatima delicaNo ratings yet

- As 2252.4-2010 Controlled Environments Biological Safety Cabinets Classes I and II - Installation and Use (BSDocument7 pagesAs 2252.4-2010 Controlled Environments Biological Safety Cabinets Classes I and II - Installation and Use (BSSAI Global - APACNo ratings yet

- DocsssDocument4 pagesDocsssAnne DesalNo ratings yet

- Law of Evidence I Standard of Proof Part 2: Prima Facie A.IntroductionDocument10 pagesLaw of Evidence I Standard of Proof Part 2: Prima Facie A.IntroductionKelvine DemetriusNo ratings yet

- CUCAS Scam in China - Study Abroad Fraud Part 1Document8 pagesCUCAS Scam in China - Study Abroad Fraud Part 1Anonymous 597ejrQAmNo ratings yet

- Extra Reading Comprehension Exercises (Unit 7, Page 80) Comprehension QuestionsDocument2 pagesExtra Reading Comprehension Exercises (Unit 7, Page 80) Comprehension Questionsroberto perezNo ratings yet

- Chair BillDocument1 pageChair BillRakesh S RNo ratings yet

- PS (T) 010Document201 pagesPS (T) 010selva rajaNo ratings yet

- Manifesto: Manifesto of The Awami National PartyDocument13 pagesManifesto: Manifesto of The Awami National PartyonepakistancomNo ratings yet

- Both Sides NowDocument3 pagesBoth Sides Nowd-railNo ratings yet

- Pop Art: Summer Flip FlopsDocument12 pagesPop Art: Summer Flip FlopssgsoniasgNo ratings yet

- 2-Doctrine of Arbitrariness and Legislative Action-A Misconceived ApplicationDocument14 pages2-Doctrine of Arbitrariness and Legislative Action-A Misconceived ApplicationShivendu PandeyNo ratings yet

- BL TestbankDocument47 pagesBL TestbankTrixie de LeonNo ratings yet

- Drug Free Workplace Act PolicyDocument8 pagesDrug Free Workplace Act PolicyglitchygachapandaNo ratings yet

- Assignment 2 SolutionDocument4 pagesAssignment 2 SolutionSobhia Kamal100% (1)

- Factorytalk Batch View Quick Start GuideDocument22 pagesFactorytalk Batch View Quick Start GuideNelsonNo ratings yet

- Rahul IAS Notes on Code of Criminal ProcedureDocument310 pagesRahul IAS Notes on Code of Criminal Proceduresam king100% (1)

- Forex For Dummies PDFDocument91 pagesForex For Dummies PDFBashir Yusuf100% (3)

- Clem Amended ComplaintDocument26 pagesClem Amended ComplaintstprepsNo ratings yet

- Succession 092418Document37 pagesSuccession 092418Hyuga NejiNo ratings yet

- Annual ReportDocument110 pagesAnnual ReportSarwan AliNo ratings yet