You might also like

- ch04 PDFDocument4 pagesch04 PDFMosharraf HussainNo ratings yet

- Belinda 125150469 OY E7-14. On April 1, 2015, Prince Company Assigns $500,000 of Its Accounts Receivable To TheDocument1 pageBelinda 125150469 OY E7-14. On April 1, 2015, Prince Company Assigns $500,000 of Its Accounts Receivable To ThebelindaNo ratings yet

- Comprehensive Problems Solution Answer Key Mid TermDocument5 pagesComprehensive Problems Solution Answer Key Mid TermGabriel Aaron DionneNo ratings yet

- Newman Hardware Store Completed The Following Merchandising Tran PDFDocument1 pageNewman Hardware Store Completed The Following Merchandising Tran PDFAnbu jaromiaNo ratings yet

- Earn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFDocument1 pageEarn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFAnbu jaromiaNo ratings yet

- MIKROEKON.docx Pengantar Akuntansi II (Part 1Document38 pagesMIKROEKON.docx Pengantar Akuntansi II (Part 1Cok Angga PutraNo ratings yet

- 3, Fa1 Question Book 2021 (Gen 5) - G I Cho Sinh ViênDocument76 pages3, Fa1 Question Book 2021 (Gen 5) - G I Cho Sinh ViênHoàng Vũ HuyNo ratings yet

- Exercises Chapter1Document4 pagesExercises Chapter1Huyen Siu NhưnNo ratings yet

- ACCT550 Homework Week 1Document6 pagesACCT550 Homework Week 1Natasha DeclanNo ratings yet

- CH 08Document10 pagesCH 08Antonios FahedNo ratings yet

- Current liability problems and solutionsDocument5 pagesCurrent liability problems and solutionsNoSepasi FebriyaniNo ratings yet

- The Statement of Financial Position of Stancia Sa at DecemberDocument1 pageThe Statement of Financial Position of Stancia Sa at DecemberCharlotte100% (1)

- Kumpulan 2 - Kancil Group ProjectDocument58 pagesKumpulan 2 - Kancil Group ProjectYamunasri Mari100% (1)

- Latihan 3Document3 pagesLatihan 3Radit Ramdan NopriantoNo ratings yet

- Tutorial Laporan Arus KasDocument17 pagesTutorial Laporan Arus KasRatna DwiNo ratings yet

- CH 03Document4 pagesCH 03flrnciairnNo ratings yet

- CH 5Document2 pagesCH 5tigger5191No ratings yet

- Ch.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesDocument7 pagesCh.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesFaishal Alghi FariNo ratings yet

- Chapter 3 ExercisesDocument11 pagesChapter 3 ExercisesNguyen VyNo ratings yet

- SOAL LATIHAN MATERI FINAL TESTDocument24 pagesSOAL LATIHAN MATERI FINAL TESTCarissaNo ratings yet

- 6-GL and FR CycleDocument6 pages6-GL and FR Cyclehangbg2k3No ratings yet

- Consolidated Financial Statement Practice 3-2Document2 pagesConsolidated Financial Statement Practice 3-2Winnie TanNo ratings yet

- Review CH 08Document7 pagesReview CH 08Martin Putra100% (1)

- Income Statements For Xcel Energy From 2011 To 2013 AppearDocument1 pageIncome Statements For Xcel Energy From 2011 To 2013 AppearHassan JanNo ratings yet

- Problems: Set B: InstructionsDocument2 pagesProblems: Set B: InstructionsflrnciairnNo ratings yet

- ACCT 2062 Homework #2Document22 pagesACCT 2062 Homework #2downinpuertorico100% (1)

- Intermediate Accounting: Assignment 4: Exercise 4-6: Multiple-Step and Extraordinary ItemsDocument13 pagesIntermediate Accounting: Assignment 4: Exercise 4-6: Multiple-Step and Extraordinary ItemsMuhammad MalikNo ratings yet

- Lease Problems Hw1Document6 pagesLease Problems Hw1Vi NguyenNo ratings yet

- تابع فصل ادارة المخزونDocument1 pageتابع فصل ادارة المخزونAhmed El KhateebNo ratings yet

- Problem 1: Organizing Categorical Variables: SolutionDocument34 pagesProblem 1: Organizing Categorical Variables: SolutionArgieshi GCNo ratings yet

- Pertemuan 8 Chapter 17Document29 pagesPertemuan 8 Chapter 17Jordan Siahaan100% (1)

- Accounting 1Document11 pagesAccounting 1Audie yanthiNo ratings yet

- Chapter4 Cost AllocationDocument14 pagesChapter4 Cost AllocationNetsanet BelayNo ratings yet

- Data Coding SchemesDocument26 pagesData Coding SchemesJovanie CadungogNo ratings yet

- 1 Intermediate Accounting IFRS 3rd Edition-554-569Document16 pages1 Intermediate Accounting IFRS 3rd Edition-554-569Khofifah SalmahNo ratings yet

- Soal AkmDocument5 pagesSoal AkmCarvin HarisNo ratings yet

- HWK 2Document3 pagesHWK 2Ingrid Anaya MoralesNo ratings yet

- CH 04Document7 pagesCH 04Tien Thanh Dang50% (2)

- Income Statement CH 4Document6 pagesIncome Statement CH 4Omar Hosny100% (1)

- ACC 557 Week 4 Chapter 6 E6 1 E6 10 E6 14 P6 3ADocument7 pagesACC 557 Week 4 Chapter 6 E6 1 E6 10 E6 14 P6 3Atswag2014No ratings yet

- Black Knights Factory Location Analysis: Building C NPV LowestDocument6 pagesBlack Knights Factory Location Analysis: Building C NPV LowestVịt HoàngNo ratings yet

- Working 3Document6 pagesWorking 3Hà Lê DuyNo ratings yet

- 1-2 - Assignment - Current and Contingent LiabilitiesDocument6 pages1-2 - Assignment - Current and Contingent LiabilitiesOliviane Theodora Wenno0% (1)

- Homework1 E3 10Document4 pagesHomework1 E3 10Jade NguyenNo ratings yet

- Assume The FollowingDocument3 pagesAssume The FollowingElliot RichardNo ratings yet

- Problems Chapter 7Document9 pagesProblems Chapter 7Trang Le0% (1)

- Maria Martinez Organized Manhattan Transport Company in January 2008 TheDocument1 pageMaria Martinez Organized Manhattan Transport Company in January 2008 Thetrilocksp Singh0% (1)

- CH 17Document6 pagesCH 17Rabie HarounNo ratings yet

- Bab 9 AkmDocument44 pagesBab 9 Akmcaesara geniza ghildaNo ratings yet

- Be16 P16 2aDocument7 pagesBe16 P16 2aLisa Hammerle ClarkNo ratings yet

- Accounting Indvidual AssignmentDocument3 pagesAccounting Indvidual AssignmentEmbassy and NGO jobs100% (1)

- Chapter 19, Modern Advanced Accounting-Review Q & ExrDocument17 pagesChapter 19, Modern Advanced Accounting-Review Q & Exrrlg4814100% (2)

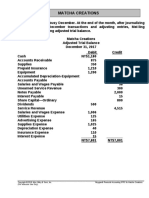

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Current Liabilities, Provisions, and Contingencies: Learning ObjectivesDocument91 pagesCurrent Liabilities, Provisions, and Contingencies: Learning ObjectivesElaine LingxNo ratings yet

- Soal Dan Jawaban Flexible BudgetDocument6 pagesSoal Dan Jawaban Flexible BudgetBayu SasongkoNo ratings yet

- Statement of Cash Flows Lecture Questions and AnswersDocument9 pagesStatement of Cash Flows Lecture Questions and AnswersSaaniya AbbasiNo ratings yet

- Accounting Errors and Dentist Business TransactionsDocument1 pageAccounting Errors and Dentist Business TransactionsJordy TangNo ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Unit 1 - Gear Manufacturing ProcessDocument54 pagesUnit 1 - Gear Manufacturing ProcessAkash DivateNo ratings yet

- Preventing and Mitigating COVID-19 at Work: Policy Brief 19 May 2021Document21 pagesPreventing and Mitigating COVID-19 at Work: Policy Brief 19 May 2021Desy Fitriani SarahNo ratings yet

- LM1011 Global ReverseLogDocument4 pagesLM1011 Global ReverseLogJustinus HerdianNo ratings yet

- 1.each of The Solids Shown in The Diagram Has The Same MassDocument12 pages1.each of The Solids Shown in The Diagram Has The Same MassrehanNo ratings yet

- Bharhut Stupa Toraa Architectural SplenDocument65 pagesBharhut Stupa Toraa Architectural Splenအသွ်င္ ေကသရNo ratings yet

- Resume of Deliagonzalez34 - 1Document2 pagesResume of Deliagonzalez34 - 1api-24443855No ratings yet

- Last Clean ExceptionDocument24 pagesLast Clean Exceptionbeom choiNo ratings yet

- Catalogoclevite PDFDocument6 pagesCatalogoclevite PDFDomingo YañezNo ratings yet

- KSEB Liable to Pay Compensation for Son's Electrocution: Kerala HC CaseDocument18 pagesKSEB Liable to Pay Compensation for Son's Electrocution: Kerala HC CaseAkhila.ENo ratings yet

- GIS Multi-Criteria Analysis by Ordered Weighted Averaging (OWA) : Toward An Integrated Citrus Management StrategyDocument17 pagesGIS Multi-Criteria Analysis by Ordered Weighted Averaging (OWA) : Toward An Integrated Citrus Management StrategyJames DeanNo ratings yet

- Acne Treatment Strategies and TherapiesDocument32 pagesAcne Treatment Strategies and TherapiesdokterasadNo ratings yet

- Hindustan Motors Case StudyDocument50 pagesHindustan Motors Case Studyashitshekhar100% (4)

- Ujian Madrasah Kelas VIDocument6 pagesUjian Madrasah Kelas VIrahniez faurizkaNo ratings yet

- FSRH Ukmec Summary September 2019Document11 pagesFSRH Ukmec Summary September 2019Kiran JayaprakashNo ratings yet

- Reader's Digest (November 2021)Document172 pagesReader's Digest (November 2021)Sha MohebNo ratings yet

- ISO 9001:2015 Explained, Fourth Edition GuideDocument3 pagesISO 9001:2015 Explained, Fourth Edition GuideiresendizNo ratings yet

- 4 Wheel ThunderDocument9 pages4 Wheel ThunderOlga Lucia Zapata SavaresseNo ratings yet

- Break Even AnalysisDocument4 pagesBreak Even Analysiscyper zoonNo ratings yet

- S5-42 DatasheetDocument2 pagesS5-42 Datasheetchillin_in_bots100% (1)

- Google Dorks For PentestingDocument11 pagesGoogle Dorks For PentestingClara Elizabeth Ochoa VicenteNo ratings yet

- Kami Export - BuildingtheTranscontinentalRailroadWEBQUESTUsesQRCodes-1Document3 pagesKami Export - BuildingtheTranscontinentalRailroadWEBQUESTUsesQRCodes-1Anna HattenNo ratings yet

- Quantification of Dell S Competitive AdvantageDocument3 pagesQuantification of Dell S Competitive AdvantageSandeep Yadav50% (2)

- SEG Newsletter 65 2006 AprilDocument48 pagesSEG Newsletter 65 2006 AprilMilton Agustin GonzagaNo ratings yet

- Riddles For KidsDocument15 pagesRiddles For KidsAmin Reza100% (8)

- India Today 11-02-2019 PDFDocument85 pagesIndia Today 11-02-2019 PDFGNo ratings yet

- Resume Template & Cover Letter Bu YoDocument4 pagesResume Template & Cover Letter Bu YoRifqi MuttaqinNo ratings yet

- Phys101 CS Mid Sem 16 - 17Document1 pagePhys101 CS Mid Sem 16 - 17Nicole EchezonaNo ratings yet

- Guidelines On Occupational Safety and Health in Construction, Operation and Maintenance of Biogas Plant 2016Document76 pagesGuidelines On Occupational Safety and Health in Construction, Operation and Maintenance of Biogas Plant 2016kofafa100% (1)

- Moor, The - Nature - Importance - and - Difficulty - of - Machine - EthicsDocument4 pagesMoor, The - Nature - Importance - and - Difficulty - of - Machine - EthicsIrene IturraldeNo ratings yet

- DC Motor Dynamics Data Acquisition, Parameters Estimation and Implementation of Cascade ControlDocument5 pagesDC Motor Dynamics Data Acquisition, Parameters Estimation and Implementation of Cascade ControlAlisson Magalhães Silva MagalhãesNo ratings yet