You might also like

- Lecture Time Value of MoneyDocument44 pagesLecture Time Value of MoneyAdina MaricaNo ratings yet

- Capstone SimulationDocument25 pagesCapstone SimulationShreshtha MalhotraNo ratings yet

- Workers Compensation and RehabilitationDocument13 pagesWorkers Compensation and RehabilitationTedd HaidarNo ratings yet

- JACULBE V Silliman UniversityDocument1 pageJACULBE V Silliman UniversityEllis LagascaNo ratings yet

- Vanguard Case Analysis - Group 2Document10 pagesVanguard Case Analysis - Group 2Rishabh GuptaNo ratings yet

- Mahindra Trucks & Bus Division: Building A Marketing PlanDocument1 pageMahindra Trucks & Bus Division: Building A Marketing PlanAyyappa ChakilamNo ratings yet

- A Plain English Guide To Financial TermsDocument42 pagesA Plain English Guide To Financial TermssyedmanNo ratings yet

- SAP Wage Types ExplainedDocument30 pagesSAP Wage Types Explainedananth-jNo ratings yet

- PK1 Plus enDocument9 pagesPK1 Plus enbskienhvqyNo ratings yet

- GSIS v. Montesclaros (434 SCRA 441)Document2 pagesGSIS v. Montesclaros (434 SCRA 441)Void Less50% (2)

- Rachit SubmissionDocument8 pagesRachit Submissionharshita ramrakhyaniNo ratings yet

- Marketing Strategy at Low-Cost Investment Leader Vanguard GroupDocument12 pagesMarketing Strategy at Low-Cost Investment Leader Vanguard GroupagarhemantNo ratings yet

- Spencers Retail Case StudyDocument10 pagesSpencers Retail Case StudyEina GuptaNo ratings yet

- Saffola's Journey of Repositioning from a Heart Medicinal Oil to a General Cooking OilDocument7 pagesSaffola's Journey of Repositioning from a Heart Medicinal Oil to a General Cooking OilshivrinderNo ratings yet

- How TITAN Watches Changed Consumers Perception About Wrist WatchesDocument16 pagesHow TITAN Watches Changed Consumers Perception About Wrist WatchessiddiquiajazNo ratings yet

- Sales and Distribution Management CourseDocument8 pagesSales and Distribution Management CourseSaurabh KadamNo ratings yet

- A-One Starch Gluco-One Case StudyDocument3 pagesA-One Starch Gluco-One Case StudyGopikrishnaNo ratings yet

- Dunkin Donuts CaseDocument12 pagesDunkin Donuts CaseKanhaiya PoddarNo ratings yet

- DaburDocument28 pagesDaburShreya GuptaNo ratings yet

- Case Analysis BigBAzaarDocument6 pagesCase Analysis BigBAzaarArka MitraNo ratings yet

- 5C Marketing Analysis of Mahindra First Choice ServicesDocument6 pages5C Marketing Analysis of Mahindra First Choice ServicesAbhinanda GhoshNo ratings yet

- Matrix Footwear Premium Segment AnalysisDocument10 pagesMatrix Footwear Premium Segment Analysisvarun_muraliNo ratings yet

- Analysis of Havells' Acquisition of Lloyd Electric's Consumer Durable BusinessDocument8 pagesAnalysis of Havells' Acquisition of Lloyd Electric's Consumer Durable BusinessRituparna BhattacharjeeNo ratings yet

- Guidelines SebiDocument19 pagesGuidelines SebiDylan WilcoxNo ratings yet

- CBBE Model Explains Dabur's Brand Equity BuildingDocument8 pagesCBBE Model Explains Dabur's Brand Equity BuildingShilpa SharmaNo ratings yet

- Manyavar ProfileDocument14 pagesManyavar ProfileAbhinav SrivastavaNo ratings yet

- IBM-Managing Brand EquityDocument78 pagesIBM-Managing Brand EquityTry Lestari Kusuma Putri0% (1)

- This Study Resource Was: Singapore Airlines: Customer Service InnovationDocument4 pagesThis Study Resource Was: Singapore Airlines: Customer Service InnovationImron MashuriNo ratings yet

- Group 8 - Managing The CompetitionDocument7 pagesGroup 8 - Managing The CompetitionAshish DrawkcabNo ratings yet

- Group 2Document23 pagesGroup 2Rahul GargNo ratings yet

- Optimize Customer Portfolio Management with Data-Driven InsightsDocument20 pagesOptimize Customer Portfolio Management with Data-Driven InsightsRedwanul IslamNo ratings yet

- Porter's Five Force Analysis of Industry: Rivalry Among Competitors - Attractiveness: HighDocument5 pagesPorter's Five Force Analysis of Industry: Rivalry Among Competitors - Attractiveness: HighPrasanta MondalNo ratings yet

- Strategic Analysis of InfosysDocument12 pagesStrategic Analysis of InfosysnaveenspacNo ratings yet

- Devebhumi Organic Honey - Sandeep Rawat ArticleDocument4 pagesDevebhumi Organic Honey - Sandeep Rawat Articlerawatsandeep2No ratings yet

- SwotDocument5 pagesSwotRajput KuldeepNo ratings yet

- Tech Talk - Creating A Social Media StrategyDocument3 pagesTech Talk - Creating A Social Media StrategyAnwesha SahooNo ratings yet

- Coffee Wars in India: How CCD Can Retain Market Leadership Against StarbucksDocument3 pagesCoffee Wars in India: How CCD Can Retain Market Leadership Against StarbucksPulkit AggarwalNo ratings yet

- Rin Case StudyDocument4 pagesRin Case StudyReha Nayyar100% (1)

- Winzo OnboardingDocument5 pagesWinzo Onboardingsaheb167No ratings yet

- Heli Flex Cables - SDM AssignmentDocument3 pagesHeli Flex Cables - SDM AssignmentKajol NigamNo ratings yet

- Eureka Forbes LimitedDocument77 pagesEureka Forbes LimitedDipanjan DasNo ratings yet

- Group5 - B 3rd CaseDocument2 pagesGroup5 - B 3rd CaseRisheek SaiNo ratings yet

- Marketing Mix of Hero MotocorpDocument2 pagesMarketing Mix of Hero Motocorpbookworm222940% (2)

- A Market Analysis of BritanniaDocument10 pagesA Market Analysis of Britanniaurmi_patel22No ratings yet

- AakashBookStore ClassDocument16 pagesAakashBookStore Classharshit100% (1)

- Integrative Bargaining: Employee Buys Car to Solve Lateness IssueDocument4 pagesIntegrative Bargaining: Employee Buys Car to Solve Lateness IssueTanya MahajanNo ratings yet

- Benefice Limited - Team 5Document16 pagesBenefice Limited - Team 5DEMINo ratings yet

- Marico PresentationDocument36 pagesMarico Presentationsandeep0975No ratings yet

- Strategic Repositioning Through CRM - GREY Worldwide Case Analysis - Final-V1Document15 pagesStrategic Repositioning Through CRM - GREY Worldwide Case Analysis - Final-V1karthikshankar2000No ratings yet

- Insurance Made Simple TitleDocument13 pagesInsurance Made Simple TitleTushar RamNo ratings yet

- PayZone Consulting's High Bandwidth BrainstormingDocument16 pagesPayZone Consulting's High Bandwidth BrainstormingAD RNo ratings yet

- Peapod-Smart Shopping For Busy PeopleDocument20 pagesPeapod-Smart Shopping For Busy Peoplemrsbellos100% (1)

- Titan Case StudyDocument14 pagesTitan Case StudySaurabh SinghNo ratings yet

- WILLS LIFESTYLE: ITC'S PREMIUM RETAIL CHAINDocument25 pagesWILLS LIFESTYLE: ITC'S PREMIUM RETAIL CHAINsangram960% (1)

- An Empirical Study On Organic Products and Services at Organic Mandya - A Case Study With Special Reference To Mandya DistrictDocument8 pagesAn Empirical Study On Organic Products and Services at Organic Mandya - A Case Study With Special Reference To Mandya DistrictGowtham RaajNo ratings yet

- Storeking-Rural ConsumersDocument10 pagesStoreking-Rural Consumersprakhar guptaNo ratings yet

- Conflicts Management and Negotiation Skills: Individual Assignment - IiDocument3 pagesConflicts Management and Negotiation Skills: Individual Assignment - IiNishit GarwasisNo ratings yet

- SALES AND CHANNEL MANAGEMENT AT DESIGNS BY KATEDocument1 pageSALES AND CHANNEL MANAGEMENT AT DESIGNS BY KATEDaniel ValensiNo ratings yet

- Anshul - Singh - RM908 - MALL Manage.Document3 pagesAnshul - Singh - RM908 - MALL Manage.Anshul singh Rajawat-RM 20RM908No ratings yet

- Visual MerchandisingDocument10 pagesVisual MerchandisingAvishkarzNo ratings yet

- COL 2016 - Marketinasfdgfg Management I - Prof. Venkatesh UmashankarDocument7 pagesCOL 2016 - Marketinasfdgfg Management I - Prof. Venkatesh UmashankarGiri DharanNo ratings yet

- Shiva Tourist DhabaDocument7 pagesShiva Tourist DhabaChaitanya JethaniNo ratings yet

- Brand Equity of IDBI Federal Life InsuranceDocument37 pagesBrand Equity of IDBI Federal Life InsuranceSandarbh Goswami100% (1)

- B2B Marketing - Jyoti - Sagar - P19052Document5 pagesB2B Marketing - Jyoti - Sagar - P19052JYOTI TALUKDARNo ratings yet

- Life Insurance Products in India: Market Strategies and Customer PerceptionsDocument19 pagesLife Insurance Products in India: Market Strategies and Customer Perceptionsumesh122No ratings yet

- AP Govt Sanctions Consolidated Pension for Polytechnic RetireesDocument2 pagesAP Govt Sanctions Consolidated Pension for Polytechnic Retireesfinance departmentNo ratings yet

- DPWH Rationalization PlanDocument12 pagesDPWH Rationalization PlanDexter G. Batalao50% (2)

- Pranav Bansal ProjectDocument66 pagesPranav Bansal Projectpranav_bansal2678No ratings yet

- Minnesota Property Tax Refund: Forms and InstructionsDocument28 pagesMinnesota Property Tax Refund: Forms and InstructionsJeffery MeyerNo ratings yet

- Awais DaoDocument68 pagesAwais DaoFaisal AwanNo ratings yet

- Htaimrb Form16 54079Document6 pagesHtaimrb Form16 54079Akhil AggarwalNo ratings yet

- Dabur Balance SheetDocument30 pagesDabur Balance SheetKrishan TiwariNo ratings yet

- Frequently Asked Questions (Faqs) : Office of The Accountant General (A&E) - Ii, Maharashtra, NagpurDocument7 pagesFrequently Asked Questions (Faqs) : Office of The Accountant General (A&E) - Ii, Maharashtra, NagpurPranil NandeshwarNo ratings yet

- AIIMS Nursing RecruitmentDocument5 pagesAIIMS Nursing RecruitmentArjun SinghNo ratings yet

- Module 7 - Ia2 Final CBLDocument22 pagesModule 7 - Ia2 Final CBLErika EsguerraNo ratings yet

- ReportDocument1 pageReportPriyanka DodkeNo ratings yet

- XX/XX/XXXX: Re: EmploymentDocument6 pagesXX/XX/XXXX: Re: EmploymentAdil KhanNo ratings yet

- 2nd National Judicial Pay Commission Volume IV (Summary) 64 PagesDocument65 pages2nd National Judicial Pay Commission Volume IV (Summary) 64 PagesPrl.District Court SrikakulamNo ratings yet

- Frienge BenefitsDocument9 pagesFrienge BenefitsKrany DollarNo ratings yet

- General Mathematics Summative Assessment 11.2.2 Name: - Section: - Date: - ScoreDocument2 pagesGeneral Mathematics Summative Assessment 11.2.2 Name: - Section: - Date: - ScoreMarc NillasNo ratings yet

- National Pension Scheme Authority: Performance Review Summary 2004Document7 pagesNational Pension Scheme Authority: Performance Review Summary 2004peter mulilaNo ratings yet

- Form 1: Death or InsanityDocument3 pagesForm 1: Death or Insanitychinna rajaNo ratings yet

- 10Document24 pages10JDNo ratings yet

- Incometaxstatement2009 2010Document2 pagesIncometaxstatement2009 2010api-3725541No ratings yet

- About The Charts: CA Pooja Kamdar DateDocument8 pagesAbout The Charts: CA Pooja Kamdar DatekbalakarthikaNo ratings yet

- Performance and Reward Management Kmbnhr04Document20 pagesPerformance and Reward Management Kmbnhr04Haris AnsariNo ratings yet

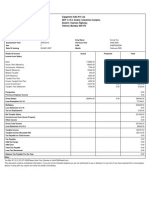

- Payroll and PayslipDocument2 pagesPayroll and PayslipKrisha TubogNo ratings yet