You might also like

- Prince George Alexander Louis of Cambridge and The Precession of EquinoxesDocument33 pagesPrince George Alexander Louis of Cambridge and The Precession of EquinoxesVJLaxmananNo ratings yet

- Firearms-Suicides: The Second Amendment and The Law of Unintended ConsequencesDocument21 pagesFirearms-Suicides: The Second Amendment and The Law of Unintended ConsequencesVJLaxmananNo ratings yet

- Three Types of Gun Violence and The Need For National Gun Safety ActDocument59 pagesThree Types of Gun Violence and The Need For National Gun Safety ActVJLaxmananNo ratings yet

- Trust Me, The Financial World Will Change Forever If Wall Street Starts Analyzing Financial Data Like We Do Baseball Stats: Miguel CabreraDocument38 pagesTrust Me, The Financial World Will Change Forever If Wall Street Starts Analyzing Financial Data Like We Do Baseball Stats: Miguel CabreraVj LaxmananNo ratings yet

- Highway Fatalities Trend Shows Its First Uptick in Six Years: Predicting Crossover With Firearms DeathsDocument39 pagesHighway Fatalities Trend Shows Its First Uptick in Six Years: Predicting Crossover With Firearms DeathsVJLaxmananNo ratings yet

- Can Staten Island Be Murder Free? Yes. That's What The Generalized Idea of Einstein's Work Function Teaches Us.Document33 pagesCan Staten Island Be Murder Free? Yes. That's What The Generalized Idea of Einstein's Work Function Teaches Us.VJLaxmananNo ratings yet

- Mayor Bloomberg's Comparison of NYC Homicide Rates and Wall Street's Ratio AnalysisDocument15 pagesMayor Bloomberg's Comparison of NYC Homicide Rates and Wall Street's Ratio AnalysisVJLaxmananNo ratings yet

- Fundamental Concepts in Data AnalysisDocument29 pagesFundamental Concepts in Data AnalysisVJLaxmananNo ratings yet

- Mayor Bloomberg's Comparison of The Homicide Rates in Chicago, Detroit, and New York Is Re-ExaminedDocument47 pagesMayor Bloomberg's Comparison of The Homicide Rates in Chicago, Detroit, and New York Is Re-ExaminedVJLaxmananNo ratings yet

- The Batting Average (BA) and Wins Above Replacement (WAR) Relation For The Batting Leaders in The 2013 SeasonDocument16 pagesThe Batting Average (BA) and Wins Above Replacement (WAR) Relation For The Batting Leaders in The 2013 SeasonVJLaxmananNo ratings yet

- Is Miguel Cabrera On Pace To Break Hack Wilson's Single-Season RBI Record? YES Can! I Changed My Mind On This. Read On Now.Document37 pagesIs Miguel Cabrera On Pace To Break Hack Wilson's Single-Season RBI Record? YES Can! I Changed My Mind On This. Read On Now.Vj LaxmananNo ratings yet

- Is Vehicle Miles Traveled (VMT) Even The Proper Metric To Determine Traffic Fatality Rates?Document26 pagesIs Vehicle Miles Traveled (VMT) Even The Proper Metric To Determine Traffic Fatality Rates?VJLaxmananNo ratings yet

- Gun Death Statistics and The Method of Least Squares and The Forgotten Property of A Straight LineDocument22 pagesGun Death Statistics and The Method of Least Squares and The Forgotten Property of A Straight LineVJLaxmananNo ratings yet

- Gun Violence in America: Americans Are Killing Themselves NOT Each Other Across StatesDocument22 pagesGun Violence in America: Americans Are Killing Themselves NOT Each Other Across StatesVJLaxmananNo ratings yet

- The Correlation Between Highway Deaths and The US EconomyDocument21 pagesThe Correlation Between Highway Deaths and The US EconomyVJLaxmananNo ratings yet

- Airline Quality Report 2013: Analysis of The On-Time PercentagesDocument46 pagesAirline Quality Report 2013: Analysis of The On-Time PercentagesVJLaxmananNo ratings yet

- Firearms-Suicides Stats Are The Only Relevant Stats in The Gun Violence DebateDocument29 pagesFirearms-Suicides Stats Are The Only Relevant Stats in The Gun Violence DebateVJLaxmananNo ratings yet

- Michigan Firearms Related Suicides The Suicides-County Population LawDocument18 pagesMichigan Firearms Related Suicides The Suicides-County Population LawVJLaxmananNo ratings yet

- Iceland Votes Against Austerity: Analysis of Iceland's Debt-GDP Data (2002-2012)Document19 pagesIceland Votes Against Austerity: Analysis of Iceland's Debt-GDP Data (2002-2012)VJLaxmananNo ratings yet

- Comparison of The Strong and Weak Gun Law States and The Ten States With Highest Levels of Gun Violence: Least Squares Analysis of The DataDocument30 pagesComparison of The Strong and Weak Gun Law States and The Ten States With Highest Levels of Gun Violence: Least Squares Analysis of The DataVJLaxmananNo ratings yet

- The Method of Least Squares: Predicting The Batting Average of A Baseball Player (Hamilton in 2013)Document19 pagesThe Method of Least Squares: Predicting The Batting Average of A Baseball Player (Hamilton in 2013)VJLaxmananNo ratings yet

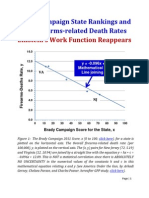

- The Brady Campaign State Ranking and The Firearms Death Rates: Einstein's Work Function ReappearsDocument42 pagesThe Brady Campaign State Ranking and The Firearms Death Rates: Einstein's Work Function ReappearsVJLaxmananNo ratings yet

- The Method of Least Squares: The GDP-Debt Relation For The Trillionaires Club of NationsDocument39 pagesThe Method of Least Squares: The GDP-Debt Relation For The Trillionaires Club of NationsVJLaxmananNo ratings yet

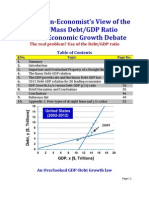

- An MIT Non-Economist's View of The Harvard-UMass Debt/GDP Ratio and The Economic Growth DebateDocument74 pagesAn MIT Non-Economist's View of The Harvard-UMass Debt/GDP Ratio and The Economic Growth DebateVJLaxmananNo ratings yet

- Is US National Debt Out of Control? The Trillionaires Club of NationsDocument36 pagesIs US National Debt Out of Control? The Trillionaires Club of NationsVJLaxmananNo ratings yet

- Bibliography-I: Articles On The Extension of Planck's Ideas and Einstein's Ideas On Energy Quantum To Topics Outside Physics, by V. LaxmananDocument19 pagesBibliography-I: Articles On The Extension of Planck's Ideas and Einstein's Ideas On Energy Quantum To Topics Outside Physics, by V. LaxmananVJLaxmananNo ratings yet

- A Brief Survey of The Debt-GDP Relationship For Some Modern 21st Century EconomiesDocument38 pagesA Brief Survey of The Debt-GDP Relationship For Some Modern 21st Century EconomiesVJLaxmananNo ratings yet

- Babe Ruth's 1923 Batting Statistics and Einstein's Work FunctionDocument18 pagesBabe Ruth's 1923 Batting Statistics and Einstein's Work FunctionVJLaxmananNo ratings yet

- Babe Ruth Batting Statistics and Einstein's Work FunctionDocument31 pagesBabe Ruth Batting Statistics and Einstein's Work FunctionVJLaxmananNo ratings yet

- Entropy and India's Billionaires (Part 1)Document11 pagesEntropy and India's Billionaires (Part 1)VJLaxmananNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Daily Practice Problems Chapter Provides Accurate Physics PracticeDocument4 pagesDaily Practice Problems Chapter Provides Accurate Physics PracticePritam kumar100% (1)

- ORS SystemDocument4 pagesORS SystemlaxmanNo ratings yet

- Computational StructuralENGG PDFDocument1,244 pagesComputational StructuralENGG PDFFAIZ100% (2)

- EE305 Lecture 2 Instrument TypesDocument22 pagesEE305 Lecture 2 Instrument TypesFrank WhiteNo ratings yet

- Bharathidasan University, Tiruchirappalli - 620 024. B.Sc. Physics Course Structure Under CBCSDocument27 pagesBharathidasan University, Tiruchirappalli - 620 024. B.Sc. Physics Course Structure Under CBCSSarjithNo ratings yet

- Chapter 5 Answers To Examination Style QuestionsDocument6 pagesChapter 5 Answers To Examination Style QuestionsRosa Wells0% (1)

- DYNROT: A Matlab Toolbox For Rotordynamics Analysis: January 1994Document27 pagesDYNROT: A Matlab Toolbox For Rotordynamics Analysis: January 1994saurabhchandrakerNo ratings yet

- Heat Transfer of Non-Newtonian Fluids in Circular Micro-TubeDocument14 pagesHeat Transfer of Non-Newtonian Fluids in Circular Micro-TubeGaurav KhamesraNo ratings yet

- Module 2 Simple Mechanisms EditedDocument58 pagesModule 2 Simple Mechanisms EditedNirshadNo ratings yet

- Decrease in Level of Sound Pressure and Sound IntensityDocument1 pageDecrease in Level of Sound Pressure and Sound IntensitySreeNo ratings yet

- X-Rays: 14 An X-Ray Beam of Initial Intensity 50 W MDocument5 pagesX-Rays: 14 An X-Ray Beam of Initial Intensity 50 W MCarlos KasambiraNo ratings yet

- A2 Physics Monthly Test January 2017Document3 pagesA2 Physics Monthly Test January 2017AbhiKhanNo ratings yet

- Acoustic Levitation Using Arduino: Experiment FindingsDocument7 pagesAcoustic Levitation Using Arduino: Experiment FindingsMichelangelo VetrugnoNo ratings yet

- 0600 C0050 0E Medium Voltage EbookDocument114 pages0600 C0050 0E Medium Voltage EbookasssasasNo ratings yet

- Examiners Report Breadth in Physics PDFDocument32 pagesExaminers Report Breadth in Physics PDFNeural Spark PhysicsNo ratings yet

- CLIL LESSON PLANpatrizia+annaDocument6 pagesCLIL LESSON PLANpatrizia+annaLuca Angelo LauriNo ratings yet

- Reading2D Spectrum PDFDocument6 pagesReading2D Spectrum PDFRaihan Uchiha100% (1)

- Chapter 11-SolutionDocument9 pagesChapter 11-Solutionmp6w9qw7t2No ratings yet

- FM Assignment 5Document4 pagesFM Assignment 5JadeJadeTrevibulNo ratings yet

- Circuit Concepts and Network Simplification Techniques 15EC34 PDFDocument535 pagesCircuit Concepts and Network Simplification Techniques 15EC34 PDFShreekar Halvi100% (2)

- Types of EMWaves & Their UsesDocument3 pagesTypes of EMWaves & Their UsesPallika DhingraNo ratings yet

- The Normalized Fundamental Matrix for ODE SystemsDocument4 pagesThe Normalized Fundamental Matrix for ODE SystemsPCTudorNo ratings yet

- Lab 6 - Transient Analysis (Transient Response) of Series RL Circuit Using OscilloscopeDocument3 pagesLab 6 - Transient Analysis (Transient Response) of Series RL Circuit Using OscilloscopehamzaNo ratings yet

- Light Metals 2012Document5 pagesLight Metals 2012Sinan YıldızNo ratings yet

- 1802 04173 PDFDocument87 pages1802 04173 PDFÇhura CristianNo ratings yet

- Power Grid Earthing CertificatesDocument40 pagesPower Grid Earthing Certificatesshanmugam.sNo ratings yet

- NCERT Solutions For Class 11 Physics 12 May Chapter 6 Work Energy and PowerDocument26 pagesNCERT Solutions For Class 11 Physics 12 May Chapter 6 Work Energy and Powerdaksh tyagiNo ratings yet

- Konsep Base Isolation dalam Perencanaan Bangunan Tahan GempaDocument56 pagesKonsep Base Isolation dalam Perencanaan Bangunan Tahan GempaNobi SetiawanNo ratings yet

- Spreadsheet - Gas Blanketed Tanks - Outbreathing Process Calculations & Control Valve Sizing - Rev2Document33 pagesSpreadsheet - Gas Blanketed Tanks - Outbreathing Process Calculations & Control Valve Sizing - Rev2MaheshNo ratings yet

- ESAC25 (C, N, D) : Fast Recovery Diodes PRV: 200 - 400 Volts Io: 10 AmperesDocument2 pagesESAC25 (C, N, D) : Fast Recovery Diodes PRV: 200 - 400 Volts Io: 10 AmperesCarlos David MarquezNo ratings yet