You might also like

- Chapter 8Document14 pagesChapter 8Patricia AyalaNo ratings yet

- 7 Competitive Firms and MarketsDocument36 pages7 Competitive Firms and MarketsGretel MinayaNo ratings yet

- PR8e GE ch08Document35 pagesPR8e GE ch08Khushi GuptaNo ratings yet

- Managerial Economics and Strategy: Third EditionDocument52 pagesManagerial Economics and Strategy: Third EditionRaeNo ratings yet

- Profit Maximization and Competitive Supply: Chapter OutlineDocument14 pagesProfit Maximization and Competitive Supply: Chapter Outlinevarun kumar VermaNo ratings yet

- Econ Microeconomics 4 4Th Edition Mceachern Solutions Manual Full Chapter PDFDocument35 pagesEcon Microeconomics 4 4Th Edition Mceachern Solutions Manual Full Chapter PDFeric.herrara805100% (11)

- ECON Microeconomics 4 4th Edition McEachern Solutions Manual 1Document14 pagesECON Microeconomics 4 4th Edition McEachern Solutions Manual 1debra100% (37)

- CH 8 Perfectly Competitive MarketsDocument14 pagesCH 8 Perfectly Competitive MarketsAbdullah AhmedNo ratings yet

- Chapt08 Krugman 46657 09 IE C08 FDocument63 pagesChapt08 Krugman 46657 09 IE C08 FMihai StoicaNo ratings yet

- 08 - Profit Maximization and Competitive Supply 2015 (Compatibility Mode)Document22 pages08 - Profit Maximization and Competitive Supply 2015 (Compatibility Mode)Jithu JoseNo ratings yet

- Perfect CompetitionDocument71 pagesPerfect CompetitionSumedha SunayaNo ratings yet

- 2.1. Perfect CompetitionDocument73 pages2.1. Perfect Competitionapi-3696178100% (5)

- Perfect Competition, Cost & Output DeterminationDocument70 pagesPerfect Competition, Cost & Output DeterminationVũ TrangNo ratings yet

- Microeconomics Exam 2 ReviewDocument3 pagesMicroeconomics Exam 2 ReviewSpartinNo ratings yet

- 1 56183 566 8 - 27Document26 pages1 56183 566 8 - 27sabza0590% (1)

- Microeconomics Theory and Applications With Calculus 4th Edition Perloff Solutions ManualDocument39 pagesMicroeconomics Theory and Applications With Calculus 4th Edition Perloff Solutions Manualjaydenur3jones100% (11)

- Microeconomics Theory and Applications With Calculus 4th Edition Perloff Solutions ManualDocument24 pagesMicroeconomics Theory and Applications With Calculus 4th Edition Perloff Solutions Manualphedrajoshuan28yjy100% (28)

- Firms in The Global Economy-Export Decisions, Outsourcing, and Multinational EnterprisesDocument68 pagesFirms in The Global Economy-Export Decisions, Outsourcing, and Multinational EnterprisesVicky KhanNo ratings yet

- Economics For Managers 2nd Edition Farnham Solutions ManualDocument9 pagesEconomics For Managers 2nd Edition Farnham Solutions Manualcassandracruzpkteqnymcf100% (33)

- Ebook Economics For Today 5Th Edition Layton Solutions Manual Full Chapter PDFDocument31 pagesEbook Economics For Today 5Th Edition Layton Solutions Manual Full Chapter PDFenstatequatrain1jahl100% (7)

- Economics For Managers Global Edition 3rd Edition Farnham Solutions ManualDocument12 pagesEconomics For Managers Global Edition 3rd Edition Farnham Solutions Manualtusseh.itemm0lh100% (27)

- Pure CompetitionDocument9 pagesPure Competitioncindycanlas_07No ratings yet

- Pricing and Output Decisions: Perfect Competition and MonopolyDocument27 pagesPricing and Output Decisions: Perfect Competition and Monopolypalak32No ratings yet

- Chapter 8 Powerpoint Slides-2Document33 pagesChapter 8 Powerpoint Slides-2Goitsemodimo SennaNo ratings yet

- Firms in Perfectly Competitive Markets: Lecture 3.2 Chapter 7Document39 pagesFirms in Perfectly Competitive Markets: Lecture 3.2 Chapter 7Hashma KhanNo ratings yet

- Economics For Today 5th Edition Layton Solutions ManualDocument10 pagesEconomics For Today 5th Edition Layton Solutions Manualcassandracruzpkteqnymcf100% (31)

- CH08 PPTDocument57 pagesCH08 PPTkesavarthiniyponnambalamNo ratings yet

- Economics For Managers - Session 11Document16 pagesEconomics For Managers - Session 11Abimanyu NNNo ratings yet

- Module 5 - Chapter 7 Q&ADocument6 pagesModule 5 - Chapter 7 Q&ABusn DNo ratings yet

- Perfect CompetitionDocument27 pagesPerfect CompetitionFlorie May SaynoNo ratings yet

- Market Structure and Perfect CompetitionDocument3 pagesMarket Structure and Perfect Competitionafrocircus09No ratings yet

- Chap011 MKT Structure Perfect CompetitionDocument75 pagesChap011 MKT Structure Perfect CompetitionM Yaseen ButtNo ratings yet

- Eaton Micro 6e Ch10Document22 pagesEaton Micro 6e Ch10sailormoon8998No ratings yet

- Chapter 8 - Perfect Competition and MonopolyDocument31 pagesChapter 8 - Perfect Competition and Monopolysalehsara556No ratings yet

- Managerial Economics - Short Answer CHDocument4 pagesManagerial Economics - Short Answer CHAnkita T. MooreNo ratings yet

- Parkin 13ge Econ IMDocument12 pagesParkin 13ge Econ IMDina SamirNo ratings yet

- Perfect CompetitionDocument37 pagesPerfect CompetitionAastha JainNo ratings yet

- Workbook Answers: AQA A2 Economics Unit 3Document25 pagesWorkbook Answers: AQA A2 Economics Unit 3New IdNo ratings yet

- FinalDocument20 pagesFinalMaryamNo ratings yet

- Perfect Competition MC Practice With AnswersDocument8 pagesPerfect Competition MC Practice With AnswersMaría José AmezquitaNo ratings yet

- 10e 12 Chap Student WorkbookDocument23 pages10e 12 Chap Student WorkbookkartikartikaaNo ratings yet

- Firms in Perfectly Competitive Markets: Chapter Summary and Learning ObjectivesDocument33 pagesFirms in Perfectly Competitive Markets: Chapter Summary and Learning ObjectivesseriosulyawksomNo ratings yet

- Microeconomics Principles and Applications 6th Edition Hall Solutions ManualDocument17 pagesMicroeconomics Principles and Applications 6th Edition Hall Solutions ManualGeorgePalmerkqgd100% (38)

- Managerial Decisions For Firms With Market Power: Essential ConceptsDocument8 pagesManagerial Decisions For Firms With Market Power: Essential ConceptsRohit SinhaNo ratings yet

- LaytonIM Ch07Document7 pagesLaytonIM Ch07astin brownNo ratings yet

- Long-Run Costs and Output Decisions: The Market SystemDocument22 pagesLong-Run Costs and Output Decisions: The Market SystemKevin PirabuNo ratings yet

- Econ2011-Chapter 8: Competitive Markets (Perfect Competition)Document10 pagesEcon2011-Chapter 8: Competitive Markets (Perfect Competition)RosemaryTanNo ratings yet

- Economics Quiz Review KeyDocument7 pagesEconomics Quiz Review Keynitin_mjl100% (1)

- ACFrOgD8mx1aj1NlKb5479so 1JW7zuyY rDfTA-F1b4xL-ijXcw9dz lrQ45xO6Z9867rqhFFkFtiBxdv9rd PnG4aFz7wpQ6TjpRyMGjnRDuIxt-gI avIe41pTKXKe-AYLrs Kx4fnBvLKc2SDocument41 pagesACFrOgD8mx1aj1NlKb5479so 1JW7zuyY rDfTA-F1b4xL-ijXcw9dz lrQ45xO6Z9867rqhFFkFtiBxdv9rd PnG4aFz7wpQ6TjpRyMGjnRDuIxt-gI avIe41pTKXKe-AYLrs Kx4fnBvLKc2SErsin TukenmezNo ratings yet

- Maximize Profits Perfect CompetitionDocument28 pagesMaximize Profits Perfect CompetitionMike Cheshire0% (1)

- 101 HWK 5 KeyDocument2 pages101 HWK 5 KeyEldana BukumbayevaNo ratings yet

- Supply in A Competitive Market: Chapter OutlineDocument52 pagesSupply in A Competitive Market: Chapter OutlineAbdullahiNo ratings yet

- Chapter 8 Profit Maximisation and Competitive SupplyDocument26 pagesChapter 8 Profit Maximisation and Competitive SupplyRitesh RajNo ratings yet

- Eco Assignment 2Document7 pagesEco Assignment 2prabhat kumarNo ratings yet

- Perfect Competition: Short Run and Long RunDocument29 pagesPerfect Competition: Short Run and Long Runr3l3kiNo ratings yet

- Economics Project ReportDocument8 pagesEconomics Project ReportKumar SanuNo ratings yet

- Econ This IsDocument11 pagesEcon This Isbeasteast80No ratings yet

- Perfect Competition Revision NotesDocument10 pagesPerfect Competition Revision NotesJyot NarangNo ratings yet

- Economics 3rd Edition Hubbard Solutions Manual DownloadDocument26 pagesEconomics 3rd Edition Hubbard Solutions Manual DownloadFrederic Harper100% (17)

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- TimeDocument3 pagesTimesailormoon8998No ratings yet

- Summa Theologica: St. Thomas Aquinas - Summa Theologicae First Part, A, Question 2, Article 3Document4 pagesSumma Theologica: St. Thomas Aquinas - Summa Theologicae First Part, A, Question 2, Article 3sailormoon8998No ratings yet

- DeathDocument3 pagesDeathsailormoon8998No ratings yet

- Eaton Micro 6e Ch17Document32 pagesEaton Micro 6e Ch17sailormoon8998No ratings yet

- Eaton Micro 6e Ch19Document29 pagesEaton Micro 6e Ch19sailormoon8998No ratings yet

- Long JumpDocument7 pagesLong Jumpsailormoon8998100% (1)

- Eaton Micro 6e Ch20Document21 pagesEaton Micro 6e Ch20sailormoon8998No ratings yet

- Eaton Micro 6e Ch18Document22 pagesEaton Micro 6e Ch18sailormoon8998No ratings yet

- Eaton Micro 6e Ch12Document27 pagesEaton Micro 6e Ch12sailormoon8998No ratings yet

- Eaton Micro 6e Ch14Document21 pagesEaton Micro 6e Ch14sailormoon8998No ratings yet

- Eaton Micro 6e Ch15Document36 pagesEaton Micro 6e Ch15sailormoon8998No ratings yet

- Eaton Micro 6e Ch11Document38 pagesEaton Micro 6e Ch11sailormoon8998No ratings yet

- Eaton Micro 6e Ch13Document32 pagesEaton Micro 6e Ch13sailormoon8998No ratings yet

- Eaton Micro 6e Ch16Document38 pagesEaton Micro 6e Ch16sailormoon8998No ratings yet

- Eaton Micro 6e Ch03Document31 pagesEaton Micro 6e Ch03sailormoon8998No ratings yet

- Eaton Micro 6e Ch10Document22 pagesEaton Micro 6e Ch10sailormoon8998No ratings yet

- Eaton Micro 6e Ch01Document21 pagesEaton Micro 6e Ch01sailormoon8998No ratings yet

- Department of Health and Human Services: Age Average Amount of Sleep Per DayDocument4 pagesDepartment of Health and Human Services: Age Average Amount of Sleep Per Daysailormoon8998No ratings yet

- Eaton Micro 6e Ch07Document33 pagesEaton Micro 6e Ch07sailormoon8998No ratings yet

- Eaton Micro 6e Ch06Document27 pagesEaton Micro 6e Ch06sailormoon8998No ratings yet

- Lore LolDocument2 pagesLore Lolsailormoon8998No ratings yet

- Eaton Micro 6e Ch05Document30 pagesEaton Micro 6e Ch05sailormoon8998No ratings yet

- Eaton Micro 6e Ch04Document29 pagesEaton Micro 6e Ch04sailormoon8998No ratings yet

- Eaton Micro 6e Ch09Document19 pagesEaton Micro 6e Ch09sailormoon8998No ratings yet

- Eaton Micro 6e Ch02Document22 pagesEaton Micro 6e Ch02sailormoon8998No ratings yet

- Optimization in Mine DesignDocument26 pagesOptimization in Mine DesignDiana Catalina Munera0% (1)

- Multiple Choice Quiz ResultsDocument4 pagesMultiple Choice Quiz ResultsAdarsh PoojaryNo ratings yet

- Financial ReportingDocument7 pagesFinancial ReportingInnocent MollaNo ratings yet

- Small Account Futures - Class SlidesDocument154 pagesSmall Account Futures - Class Slideshotdog10No ratings yet

- Linear Programming Problems ExplainedDocument12 pagesLinear Programming Problems ExplainedThea BacsaNo ratings yet

- Sample Midterm Exam 1Document14 pagesSample Midterm Exam 1keo k usttadNo ratings yet

- Article 2 Roe Breakd Dec 12 5pDocument5 pagesArticle 2 Roe Breakd Dec 12 5pRicardo Jáquez CortésNo ratings yet

- Onapal V CADocument10 pagesOnapal V CAMp CasNo ratings yet

- Export CostingDocument6 pagesExport CostingVasant KothariNo ratings yet

- Economics 0455 Learner Guide 2015Document21 pagesEconomics 0455 Learner Guide 2015Deshna RathodNo ratings yet

- Cao Thu 1Document12 pagesCao Thu 1Lê Hữu NamNo ratings yet

- Maximising Profits in Competitive MarketsDocument6 pagesMaximising Profits in Competitive MarketsGag PafNo ratings yet

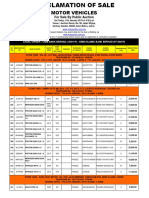

- Motor Vehicles: For Sale by Public AuctionDocument7 pagesMotor Vehicles: For Sale by Public AuctionmanNo ratings yet

- International Business Strategy NotesDocument68 pagesInternational Business Strategy NotesAlexandra LífNo ratings yet

- Evans Ba1 Tif Ch01Document17 pagesEvans Ba1 Tif Ch01lulucrossNo ratings yet

- Notes Receivables: 1. Present Value IsDocument4 pagesNotes Receivables: 1. Present Value IsZyrene Kei ReyesNo ratings yet

- Answers To Assignment 1 (Chs1-3)Document7 pagesAnswers To Assignment 1 (Chs1-3)Subashini Maniam100% (1)

- Developing Pricing Strategies and ProgramsDocument42 pagesDeveloping Pricing Strategies and ProgramsstudentNo ratings yet

- SPDRDocument268 pagesSPDRRoberto PerezNo ratings yet

- BIDDING DOCUMENTS - Security Services 1Document108 pagesBIDDING DOCUMENTS - Security Services 1ValerieAnnVilleroAlvarezValienteNo ratings yet

- Price Tag Laws in The PhilippinesDocument2 pagesPrice Tag Laws in The PhilippinesCjhay MarcosNo ratings yet

- Case Study On Operational ManagementDocument3 pagesCase Study On Operational ManagementCindy Faye CrusanteNo ratings yet

- Annex Z Dole Kabuhayan Program Group Business Plan: I. Project BriefDocument6 pagesAnnex Z Dole Kabuhayan Program Group Business Plan: I. Project BriefFamily Liggayu Diaries100% (4)

- Who Decides What's On Your PlateDocument2 pagesWho Decides What's On Your PlateLeonardo LópezNo ratings yet

- Pile cp16Document13 pagesPile cp16casarokarNo ratings yet

- Midterm Exam of Managerial Economics 2022Document4 pagesMidterm Exam of Managerial Economics 2022dayeyoutai779No ratings yet

- Assessment B - Knowledge Test (Weng Yan CHU)Document5 pagesAssessment B - Knowledge Test (Weng Yan CHU)Natasha Tasha100% (1)

- Gafta 49Document4 pagesGafta 49tinhcoonlineNo ratings yet

- STAR AIR'S PRICING STRATEGY IN THE AIRPLANE INDUSTRYDocument8 pagesSTAR AIR'S PRICING STRATEGY IN THE AIRPLANE INDUSTRYhabiburachman_tsNo ratings yet

- DAN - 7 Aug 2016 - Progress TestDocument9 pagesDAN - 7 Aug 2016 - Progress TestHuy BảoNo ratings yet