You might also like

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Statement of Comprehensive IncomeDocument11 pagesStatement of Comprehensive IncomeKhiezna PakamNo ratings yet

- Accounting For MerchandisingDocument2 pagesAccounting For MerchandisingEvelyn MaligayaNo ratings yet

- Answers 5Document101 pagesAnswers 5api-308823932100% (1)

- Certified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasDocument63 pagesCertified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasAllen CarlNo ratings yet

- 1 How To Prepare An Income StatementDocument4 pages1 How To Prepare An Income Statementapi-299265916No ratings yet

- NC Bacctg1 Final Exam Part 1Document3 pagesNC Bacctg1 Final Exam Part 1Danica Onte0% (1)

- FABM1 Lesson8-1 Five Major Accounts-LIABILITIESDocument13 pagesFABM1 Lesson8-1 Five Major Accounts-LIABILITIESWalter MataNo ratings yet

- Statement of Comprehensive Income (SCI) Single StepDocument11 pagesStatement of Comprehensive Income (SCI) Single StepNikolai MarasiganNo ratings yet

- CHAPTER 6 - Adjusting EntriesDocument25 pagesCHAPTER 6 - Adjusting EntriesMuhammad AdibNo ratings yet

- Wright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueDocument6 pagesWright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueLen PenieroNo ratings yet

- Book of Accounts Part 1. JournalDocument12 pagesBook of Accounts Part 1. JournalJace AbeNo ratings yet

- Test Question For Exam Chapter 1 To 6Document4 pagesTest Question For Exam Chapter 1 To 6Cherryl ValmoresNo ratings yet

- Exercises Short ProblemsDocument6 pagesExercises Short ProblemsKlaire SwswswsNo ratings yet

- FABM Week 8 - Bank Accounts, Transactions and DocumentsDocument26 pagesFABM Week 8 - Bank Accounts, Transactions and Documentsvmin친구No ratings yet

- Accounting EquationDocument55 pagesAccounting EquationRahul VermaNo ratings yet

- Analysis of Common Business TransactionsDocument18 pagesAnalysis of Common Business TransactionsClarisse RosalNo ratings yet

- Perpetual Inventory SystemDocument5 pagesPerpetual Inventory SystemRey ArudNo ratings yet

- Exercise Cash ControlDocument6 pagesExercise Cash ControlYallyNo ratings yet

- Buying & Selling For TeachersDocument46 pagesBuying & Selling For Teachersnino sulit100% (1)

- Adjusting Entries Company A ExercisesDocument19 pagesAdjusting Entries Company A ExercisesRodolfo CorpuzNo ratings yet

- Module in Fundamentals of Accountancy, Business and Management (Grade 12) Statement of Comprehensive Income (SCI)Document7 pagesModule in Fundamentals of Accountancy, Business and Management (Grade 12) Statement of Comprehensive Income (SCI)Jocelyn Estrella Prendol SorianoNo ratings yet

- Week 6Document11 pagesWeek 6Kim Albero CubelNo ratings yet

- FOA Final OutputDocument18 pagesFOA Final OutputGwyneth MogolNo ratings yet

- Essential Accounting Concepts and ExamplesDocument17 pagesEssential Accounting Concepts and ExamplesMarryRose Dela Torre FerrancoNo ratings yet

- CFS ComponentsDocument11 pagesCFS ComponentsAlyssa Nikki VersozaNo ratings yet

- I. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1Document3 pagesI. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1HLeigh Nietes-GabutanNo ratings yet

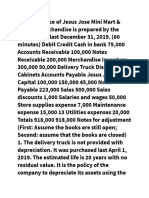

- E Trial Balance of Jesus Jose Mini MartDocument3 pagesE Trial Balance of Jesus Jose Mini Martshamsa ynnaNo ratings yet

- Lesson 4 - The Steps in The Accounting CycleDocument5 pagesLesson 4 - The Steps in The Accounting Cycleamora elyseNo ratings yet

- FabmDocument18 pagesFabmYangyang Leslie100% (1)

- Business Finance (Quarter 1 - Weeks 3 & 4)Document11 pagesBusiness Finance (Quarter 1 - Weeks 3 & 4)Francine Dominique CollantesNo ratings yet

- How To Calculate Gross ProfitDocument3 pagesHow To Calculate Gross ProfitQais WaqasNo ratings yet

- Financial StatementDocument5 pagesFinancial StatementJubelle Tacusalme PunzalanNo ratings yet

- Introduction To AccountingDocument37 pagesIntroduction To AccountingRey ViloriaNo ratings yet

- Elements of Accounting LectureDocument43 pagesElements of Accounting LectureRaissa Mae100% (1)

- Quiz 5 Books of Accounts Without AnswerDocument5 pagesQuiz 5 Books of Accounts Without AnswerHello KittyNo ratings yet

- Case 2-4 - SceDocument3 pagesCase 2-4 - SceNica CabradillaNo ratings yet

- Adjusting Journal EntriesDocument11 pagesAdjusting Journal EntriesKatrina RomasantaNo ratings yet

- Teddy BearDocument3 pagesTeddy BearKrisha Joy MercadoNo ratings yet

- Handout 6 Accounting For Service Merchandising and Manufacturing BusinessesDocument8 pagesHandout 6 Accounting For Service Merchandising and Manufacturing BusinessesSevi MendezNo ratings yet

- Adjusting Entries for Uncollectible AccountsDocument6 pagesAdjusting Entries for Uncollectible AccountsKristine IvyNo ratings yet

- Analyzing Business TransactionsDocument13 pagesAnalyzing Business TransactionsEricJohnRoxasNo ratings yet

- Account TitlesDocument5 pagesAccount TitlesalyNo ratings yet

- Lesley Dela Cruz Clearners Financial StatementsDocument7 pagesLesley Dela Cruz Clearners Financial StatementsJasmine ActaNo ratings yet

- Accounting Cycle Journal Entries With Chart of AccountsDocument3 pagesAccounting Cycle Journal Entries With Chart of AccountsMay Rojas MortosNo ratings yet

- Chapter 7 Books of Accounts Journals and LedgersDocument28 pagesChapter 7 Books of Accounts Journals and Ledgersjcxes Del rosarioNo ratings yet

- Accounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloDocument41 pagesAccounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloRoxe XNo ratings yet

- Fabm 2Document170 pagesFabm 2Asti GumacaNo ratings yet

- Cash BudgetDocument3 pagesCash Budgetmanoj kumarNo ratings yet

- 2 Adjusting Journal EntriesDocument6 pages2 Adjusting Journal EntriesJerric CristobalNo ratings yet

- Saint Louis College-Cebu: (Servant Leaders For Mission)Document4 pagesSaint Louis College-Cebu: (Servant Leaders For Mission)Marc Graham NacuaNo ratings yet

- Adjusting Entries ProblemsDocument5 pagesAdjusting Entries ProblemsDirck VerraNo ratings yet

- BUS 142 - Slides Chap 3. The Adjusting ProcessDocument50 pagesBUS 142 - Slides Chap 3. The Adjusting ProcessJess Ica100% (1)

- Philippine high school student's accounting worksheetDocument7 pagesPhilippine high school student's accounting worksheetCha Eun WooNo ratings yet

- Fundamentals of Accountancy 1 Trial BalanceDocument12 pagesFundamentals of Accountancy 1 Trial BalanceRichard Rhamil Carganillo Garcia Jr.No ratings yet

- Practice Problem 11.0: Name Date Course/Year ScoreDocument5 pagesPractice Problem 11.0: Name Date Course/Year ScoreCatherine GonzalesNo ratings yet

- Financial Statement Analysis TechniquesDocument38 pagesFinancial Statement Analysis TechniquesmercyvienhoNo ratings yet

- What Is Bank Reconciliation.Document11 pagesWhat Is Bank Reconciliation.Sabrena FennaNo ratings yet

- Shs Abm Gr12 Fabm2 q1 m2 Statement-Of-comprehensive-IncomeDocument14 pagesShs Abm Gr12 Fabm2 q1 m2 Statement-Of-comprehensive-IncomeKye RauleNo ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- Chapter 5 - Acc. OperationsDocument42 pagesChapter 5 - Acc. OperationsSozia TanNo ratings yet

- Chapter 1 - Acc - in BusinessDocument54 pagesChapter 1 - Acc - in BusinessSozia TanNo ratings yet

- Budgeting Tools for Merchandising BusinessesDocument55 pagesBudgeting Tools for Merchandising BusinessesSozia TanNo ratings yet

- PP For Chapter 10 - Variance Analysis - FinalDocument52 pagesPP For Chapter 10 - Variance Analysis - FinalSozia TanNo ratings yet

- UUM Business Accounting Course OverviewDocument5 pagesUUM Business Accounting Course OverviewSozia TanNo ratings yet

- Chapter 3 - Adj - Ncial StateDocument34 pagesChapter 3 - Adj - Ncial StateSozia TanNo ratings yet

- PP For Chapter 7 - Introduction To Managerial Accounting - FinalDocument40 pagesPP For Chapter 7 - Introduction To Managerial Accounting - FinalSozia TanNo ratings yet

- Chapter 3 - Adj - Ncial StateDocument34 pagesChapter 3 - Adj - Ncial StateSozia TanNo ratings yet

- Chapter 4 - Com - Nting CycleDocument44 pagesChapter 4 - Com - Nting CycleSozia TanNo ratings yet

- Chapter 2 - Ana - RansactionsDocument35 pagesChapter 2 - Ana - RansactionsSozia TanNo ratings yet

- Chapter 3 - Adj - Ncial StateDocument34 pagesChapter 3 - Adj - Ncial StateSozia TanNo ratings yet

- PP For Chapter 8 - Cost Volume Profit - FinalDocument91 pagesPP For Chapter 8 - Cost Volume Profit - FinalSozia TanNo ratings yet

- Chapter 14 - Co - It AnalysisDocument68 pagesChapter 14 - Co - It AnalysisSozia TanNo ratings yet

- Budgeting As A Tool For Planning and Controlling: Budget????Document73 pagesBudgeting As A Tool For Planning and Controlling: Budget????Sozia TanNo ratings yet

- PP For Chapter 6 - Financial Statement Analysis - FinalDocument67 pagesPP For Chapter 6 - Financial Statement Analysis - FinalSozia TanNo ratings yet

- Chapter 6Document63 pagesChapter 6Sozia TanNo ratings yet

- Click To Edit Master Title Style: Completing The Accounting CycleDocument54 pagesClick To Edit Master Title Style: Completing The Accounting CycleSozia TanNo ratings yet

- Chapter 6 - Acc. OperationsDocument44 pagesChapter 6 - Acc. OperationsSozia TanNo ratings yet

- Chapter 8Document30 pagesChapter 8Sozia TanNo ratings yet

- Chapter 13 - Fi - NT AnalysisDocument64 pagesChapter 13 - Fi - NT AnalysisSozia TanNo ratings yet

- PP For Chapter 1 - Introduction To Accounting - FinalDocument97 pagesPP For Chapter 1 - Introduction To Accounting - FinalSozia TanNo ratings yet

- PP For Chapter 2 - Analyzing Transactions - FinalDocument49 pagesPP For Chapter 2 - Analyzing Transactions - FinalSozia TanNo ratings yet

- Power Notes: Company Annual ReportDocument14 pagesPower Notes: Company Annual ReportSozia TanNo ratings yet

- Chapter 6Document24 pagesChapter 6Sozia TanNo ratings yet

- Chapter 7Document24 pagesChapter 7Sozia TanNo ratings yet

- Chapter 4Document26 pagesChapter 4Sozia TanNo ratings yet

- Topic 12Document19 pagesTopic 12Sozia TanNo ratings yet

- Chapter 5 ContDocument55 pagesChapter 5 ContSozia TanNo ratings yet

- Financial Markets and Institutions: Required Reading: Mishkin, Chapter 1 andDocument43 pagesFinancial Markets and Institutions: Required Reading: Mishkin, Chapter 1 andVivek Roy100% (1)

- Chapter 6Document63 pagesChapter 6Sozia TanNo ratings yet

- ms3 Seq 01 Expressing Interests With Adverbs of FrequencyDocument3 pagesms3 Seq 01 Expressing Interests With Adverbs of Frequencyg27rimaNo ratings yet

- 1120 Assessment 1A - Self-Assessment and Life GoalDocument3 pages1120 Assessment 1A - Self-Assessment and Life GoalLia LeNo ratings yet

- Icici Bank FileDocument7 pagesIcici Bank Fileharman singhNo ratings yet

- Science 10-2nd Periodical Test 2018-19Document2 pagesScience 10-2nd Periodical Test 2018-19Emiliano Dela Cruz100% (3)

- The Neteru Gods Goddesses of The Grand EnneadDocument16 pagesThe Neteru Gods Goddesses of The Grand EnneadKirk Teasley100% (1)

- DINDIGULDocument10 pagesDINDIGULAnonymous BqLSSexONo ratings yet

- Examination of InvitationDocument3 pagesExamination of InvitationChoi Rinna62% (13)

- 05 Gregor and The Code of ClawDocument621 pages05 Gregor and The Code of ClawFaye Alonzo100% (7)

- Compound SentenceDocument31 pagesCompound Sentencerosemarie ricoNo ratings yet

- Supply Chain AssignmentDocument29 pagesSupply Chain AssignmentHisham JackNo ratings yet

- Chapter 12 The Incredible Story of How The Great Controversy Was Copied by White From Others, and Then She Claimed It To Be Inspired.Document6 pagesChapter 12 The Incredible Story of How The Great Controversy Was Copied by White From Others, and Then She Claimed It To Be Inspired.Barry Lutz Sr.No ratings yet

- Tata Hexa (2017-2019) Mileage (14 KML) - Hexa (2017-2019) Diesel Mileage - CarWaleDocument1 pageTata Hexa (2017-2019) Mileage (14 KML) - Hexa (2017-2019) Diesel Mileage - CarWaleMahajan VickyNo ratings yet

- Neligence: Allows Standards of Acceptable Behavior To Be Set For SocietyDocument3 pagesNeligence: Allows Standards of Acceptable Behavior To Be Set For SocietyransomNo ratings yet

- GASB 34 Governmental Funds vs Government-Wide StatementsDocument22 pagesGASB 34 Governmental Funds vs Government-Wide StatementsLisa Cooley100% (1)

- Addendum Dokpil Patimban 2Document19 pagesAddendum Dokpil Patimban 2HeriYantoNo ratings yet

- Mundane AstrologyDocument93 pagesMundane Astrologynikhil mehra100% (5)

- Communication Tourism PDFDocument2 pagesCommunication Tourism PDFShane0% (1)

- RumpelstiltskinDocument7 pagesRumpelstiltskinAndreia PintoNo ratings yet

- Amway Health CareDocument7 pagesAmway Health CareChowduru Venkat Sasidhar SharmaNo ratings yet

- BCIC General Holiday List 2011Document4 pagesBCIC General Holiday List 2011Srikanth DLNo ratings yet

- DLL - Science 6 - Q3 - W3Document6 pagesDLL - Science 6 - Q3 - W3AnatasukiNo ratings yet

- TITLE 28 United States Code Sec. 3002Document77 pagesTITLE 28 United States Code Sec. 3002Vincent J. Cataldi91% (11)

- Explaining ADHD To TeachersDocument1 pageExplaining ADHD To TeachersChris100% (2)

- Wonder at The Edge of The WorldDocument3 pagesWonder at The Edge of The WorldLittle, Brown Books for Young Readers0% (1)

- 110 TOP Survey Interview QuestionsDocument18 pages110 TOP Survey Interview QuestionsImmu100% (1)

- Introduction To Computing (COMP-01102) Telecom 1 Semester: Lab Experiment No.05Document7 pagesIntroduction To Computing (COMP-01102) Telecom 1 Semester: Lab Experiment No.05ASISNo ratings yet

- FOCGB4 Utest VG 5ADocument1 pageFOCGB4 Utest VG 5Asimple footballNo ratings yet

- List of Parts For Diy Dremel CNC by Nikodem Bartnik: Part Name Quantity BanggoodDocument6 pagesList of Parts For Diy Dremel CNC by Nikodem Bartnik: Part Name Quantity Banggoodyogesh parmarNo ratings yet

- Setting MemcacheDocument2 pagesSetting MemcacheHendra CahyanaNo ratings yet

- Pale Case Digest Batch 2 2019 2020Document26 pagesPale Case Digest Batch 2 2019 2020Carmii HoNo ratings yet