You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Currency Notes For Visually ImpairedDocument5 pagesCurrency Notes For Visually ImpairedRohit Nain Srk GeorgianNo ratings yet

- Maruti - Case StudyDocument17 pagesMaruti - Case Studygautham994467% (3)

- Windchill FlexPLMDocument5 pagesWindchill FlexPLMRohit Nain Srk GeorgianNo ratings yet

- Shahi Export PVT - LTD.: (Unit Sarla Fabrics)Document27 pagesShahi Export PVT - LTD.: (Unit Sarla Fabrics)Rohit Nain Srk GeorgianNo ratings yet

- A Joint Venture in ThailandDocument18 pagesA Joint Venture in ThailandRohit Nain Srk GeorgianNo ratings yet

- Work Breakdown StructureDocument9 pagesWork Breakdown StructureArif ForhadNo ratings yet

- Project Planning WorkDocument29 pagesProject Planning WorkRohit Nain Srk GeorgianNo ratings yet

- Shahi Exports CSR Vision and Focus AreasDocument9 pagesShahi Exports CSR Vision and Focus AreasRohit Nain Srk GeorgianNo ratings yet

- Acht Er Grond ArtikelDocument18 pagesAcht Er Grond ArtikelRohit Nain Srk GeorgianNo ratings yet

- WBSDocument6 pagesWBSLuthfi HanafiNo ratings yet

- CSR Policy SummaryDocument4 pagesCSR Policy SummaryAmi RayNo ratings yet

- Character MerchandisingDocument27 pagesCharacter Merchandisingsaurav suman100% (1)

- Project Planning WorkDocument29 pagesProject Planning WorkRohit Nain Srk GeorgianNo ratings yet

- Work Breakdown StructureDocument11 pagesWork Breakdown StructureRohit Nain Srk GeorgianNo ratings yet

- Character MerchandisingDocument27 pagesCharacter Merchandisingsaurav suman100% (1)

- IP and Mergers BnhjuDocument59 pagesIP and Mergers BnhjuRohit Nain Srk GeorgianNo ratings yet

- RelativityDocument28 pagesRelativitygmleninNo ratings yet

- ERP II - Next Generation ERPDocument3 pagesERP II - Next Generation ERPShalini SharmaNo ratings yet

- 7 An Overview Enterprise Resource Planning ERPDocument20 pages7 An Overview Enterprise Resource Planning ERPReema DawraNo ratings yet

- A Legal Dispute Between Tire CompanyDocument4 pagesA Legal Dispute Between Tire CompanyRohit Nain Srk GeorgianNo ratings yet

- Joint Venture GuidanceDocument112 pagesJoint Venture GuidanceRohit Nain Srk Georgian100% (1)

- Theory of RelativityDocument27 pagesTheory of RelativityNageswar ReddyNo ratings yet

- Toyota's Kaizen Experience: HistoryDocument12 pagesToyota's Kaizen Experience: HistoryRohit Nain Srk GeorgianNo ratings yet

- New Microsoft PowerPoint PresentationDocument22 pagesNew Microsoft PowerPoint PresentationRohit Nain Srk GeorgianNo ratings yet

- Module 5 D Obligations With A Penal ClauseDocument3 pagesModule 5 D Obligations With A Penal Clauseairam cabadduNo ratings yet

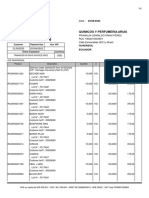

- Factura ComercialDocument6 pagesFactura ComercialKaren MezaNo ratings yet

- Caridad Ongsiako, Et. Al Vs Emilia Ongsiako, Et. Al (GR. No. 7510, 30 March 1957, 101 Phil 1196-1197)Document1 pageCaridad Ongsiako, Et. Al Vs Emilia Ongsiako, Et. Al (GR. No. 7510, 30 March 1957, 101 Phil 1196-1197)Archibald Jose Tiago ManansalaNo ratings yet

- KEY DEFINITIONS IN COMPANIES ORDINANCE 1984Document204 pagesKEY DEFINITIONS IN COMPANIES ORDINANCE 1984Muhammad KamranNo ratings yet

- Teoría Producción Por LotesDocument3 pagesTeoría Producción Por LotesGedeón PizarroNo ratings yet

- Red Tape Report: Behind The Scenes of The Section 8 Housing ProgramDocument7 pagesRed Tape Report: Behind The Scenes of The Section 8 Housing ProgramBill de BlasioNo ratings yet

- GR 158896 Siayngco Vs Siayngco PIDocument1 pageGR 158896 Siayngco Vs Siayngco PIMichael JonesNo ratings yet

- Vasai Housing Federation AppendicesDocument6 pagesVasai Housing Federation AppendicesPrasadNo ratings yet

- A Multiple Type Questions BA Political Science CBCSS Private Sem IDocument35 pagesA Multiple Type Questions BA Political Science CBCSS Private Sem IHaji Ghaz100% (1)

- Contract Formation Issues in Betty and Albert's Car Sale NegotiationsDocument2 pagesContract Formation Issues in Betty and Albert's Car Sale NegotiationsRajesh NagarajanNo ratings yet

- 2016 Ballb (B)Document36 pages2016 Ballb (B)Vicky D0% (1)

- Guaranteed Tobacco Arrival Condition DisputeDocument12 pagesGuaranteed Tobacco Arrival Condition DisputeFaye Cience BoholNo ratings yet

- Plaint: in The Court of Civil Judge Senior Division Nasik Summary Suit No. 1987Document10 pagesPlaint: in The Court of Civil Judge Senior Division Nasik Summary Suit No. 1987Kumar RameshNo ratings yet

- An Essay On The Foreign Policy of IndiaDocument2 pagesAn Essay On The Foreign Policy of IndiatintucrajuNo ratings yet

- Armco - Simplified One-Page Hauling Agreement Template 2019Document3 pagesArmco - Simplified One-Page Hauling Agreement Template 2019Sulpi Casil100% (1)

- Customs Seizure of Ships UpheldDocument2 pagesCustoms Seizure of Ships UpheldFgmtNo ratings yet

- Vakalatnama Supreme CourtDocument2 pagesVakalatnama Supreme CourtSiddharth Chitturi80% (5)

- Imbong v. Ochoa 4. The Question of Constitutionality Must Be Raised at The Earliest OpportunityDocument3 pagesImbong v. Ochoa 4. The Question of Constitutionality Must Be Raised at The Earliest OpportunitychristineNo ratings yet

- Case Update - Ayache vs. Pjcmi - 6.22.22Document2 pagesCase Update - Ayache vs. Pjcmi - 6.22.22Lemwil SaclayNo ratings yet

- Q. Write A Short Note On FIR. Discuss The Guidelines Laid Down by The Supreme Court For Mandatory Registration of FIR in Lalita Kumari's CaseDocument3 pagesQ. Write A Short Note On FIR. Discuss The Guidelines Laid Down by The Supreme Court For Mandatory Registration of FIR in Lalita Kumari's CaseshareenNo ratings yet

- Certified List of Candidates For Congressional and Local Positions For The May 13, 2013 2013 National, Local and Armm ElectionsDocument2 pagesCertified List of Candidates For Congressional and Local Positions For The May 13, 2013 2013 National, Local and Armm ElectionsSunStar Philippine NewsNo ratings yet

- Article On Insurable InterestDocument9 pagesArticle On Insurable InterestPrashanth VaradarajanNo ratings yet

- Presentation On GST: (Goods and Services Tax)Document11 pagesPresentation On GST: (Goods and Services Tax)tpplantNo ratings yet

- Geriatric Nursing: Saint Louis UniversityDocument5 pagesGeriatric Nursing: Saint Louis UniversityDannielle Kathrine JoyceNo ratings yet

- Barber: Affordable Housing in MassachusettsDocument29 pagesBarber: Affordable Housing in MassachusettsNew England Law ReviewNo ratings yet

- Rule 44 Ordinary Appealed CasesDocument21 pagesRule 44 Ordinary Appealed CasesJenely Joy Areola-TelanNo ratings yet

- Forms of Business OwnershipDocument26 pagesForms of Business OwnershipKCD MULTITRACKSNo ratings yet

- P L D 2016 Lahore 587 - Releif Not Prayed For Cannot Be GrantedDocument14 pagesP L D 2016 Lahore 587 - Releif Not Prayed For Cannot Be GrantedAhmad RazaNo ratings yet

- Philippine Government Structure ExplainedDocument5 pagesPhilippine Government Structure ExplainedLiezel NibresNo ratings yet

- High Court Appeal Seeks Reversal of Dismissed Debt Recovery SuitDocument2 pagesHigh Court Appeal Seeks Reversal of Dismissed Debt Recovery SuitBhumikaNo ratings yet