You might also like

- Chap 021Document16 pagesChap 021Bob RobNo ratings yet

- Chapter 4 BF TextDocument28 pagesChapter 4 BF TextBob RobNo ratings yet

- Chap 007Document19 pagesChap 007Bob RobNo ratings yet

- Wills, Trusts, and Estates: Week 3 Spring 2015Document38 pagesWills, Trusts, and Estates: Week 3 Spring 2015Bob RobNo ratings yet

- Chap 012Document17 pagesChap 012Bob RobNo ratings yet

- Spring 2015 - WTE - Week 5-6 - TrustsDocument52 pagesSpring 2015 - WTE - Week 5-6 - TrustsBob RobNo ratings yet

- Chap 011Document28 pagesChap 011Bob RobNo ratings yet

- Chap 016Document20 pagesChap 016Bob RobNo ratings yet

- Chap 013Document19 pagesChap 013Bob RobNo ratings yet

- Chap 009Document23 pagesChap 009Bob RobNo ratings yet

- Spring+2015+-+WTE+-+Week+1+ IntroDocument4 pagesSpring+2015+-+WTE+-+Week+1+ IntroBob RobNo ratings yet

- Chap 005Document29 pagesChap 005Bob RobNo ratings yet

- Spring+2015+-+WTE+-+Week+2+ Estate+Planning+Process+and+PropertyDocument51 pagesSpring+2015+-+WTE+-+Week+2+ Estate+Planning+Process+and+PropertyBob RobNo ratings yet

- Spring 2015 - WTE - Review Exam 1Document8 pagesSpring 2015 - WTE - Review Exam 1Bob RobNo ratings yet

- Spring+2015+-+WTE+-+Week+2+ Estate+Planning+Process+and+PropertyDocument51 pagesSpring+2015+-+WTE+-+Week+2+ Estate+Planning+Process+and+PropertyBob RobNo ratings yet

- Week 8Document1 pageWeek 8Bob RobNo ratings yet

- Spring+2015+-+WTE+-+Week+11+ GSTTDocument19 pagesSpring+2015+-+WTE+-+Week+11+ GSTTBob RobNo ratings yet

- Week 8Document1 pageWeek 8Bob RobNo ratings yet

- Wills, Trusts, and Estates: Week 3 Spring 2015Document38 pagesWills, Trusts, and Estates: Week 3 Spring 2015Bob RobNo ratings yet

- Nonforfeiture TableDocument1 pageNonforfeiture TableBob RobNo ratings yet

- Linear Programming: Model Formulation and Graphical SolutionDocument39 pagesLinear Programming: Model Formulation and Graphical SolutionBob RobNo ratings yet

- Insurance Ch.9cDocument31 pagesInsurance Ch.9cBob RobNo ratings yet

- Linear Programming: Model Formulation and Graphical SolutionDocument39 pagesLinear Programming: Model Formulation and Graphical SolutionBob RobNo ratings yet

- Insurance+Needs+-+Ch +9Document7 pagesInsurance+Needs+-+Ch +9Bob RobNo ratings yet

- Computer Solution and Sensitivity Analysis of Linear Programming ProblemsDocument38 pagesComputer Solution and Sensitivity Analysis of Linear Programming ProblemsBob RobNo ratings yet

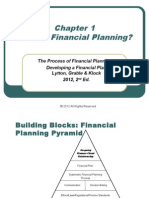

- What Is Financial Planning?Document41 pagesWhat Is Financial Planning?Bob RobNo ratings yet

- Life Insurance 2. Annuities 3. Health Insurance & Hsas 4. Long-Term Care 5. DisabilityDocument44 pagesLife Insurance 2. Annuities 3. Health Insurance & Hsas 4. Long-Term Care 5. DisabilityBob RobNo ratings yet

- Management Science Models for Problem SolvingDocument17 pagesManagement Science Models for Problem SolvingBob RobNo ratings yet

- Computer Solution and Sensitivity Analysis of Linear Programming ProblemsDocument38 pagesComputer Solution and Sensitivity Analysis of Linear Programming ProblemsBob RobNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

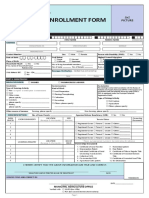

- 1.) Enrollment Form v.3 04.06.18Document2 pages1.) Enrollment Form v.3 04.06.18Psbc RosarioNo ratings yet

- Proclamation No. 172Document13 pagesProclamation No. 172Mang SimoNo ratings yet

- Squatters Rights Oklahoma - Difference Between Trespasser and SquatterDocument12 pagesSquatters Rights Oklahoma - Difference Between Trespasser and Squatterscott nachatiloNo ratings yet

- Land Title and Deeds ReviewerDocument2 pagesLand Title and Deeds ReviewerPauline Vistan Garcia100% (1)

- Analysis On The Proposed Property Tax AssessmentDocument32 pagesAnalysis On The Proposed Property Tax AssessmentAB AgostoNo ratings yet

- Securitization: Day 1 ActivitiesDocument4 pagesSecuritization: Day 1 ActivitiesNye LavalleNo ratings yet

- Bir Ruling 423 16Document2 pagesBir Ruling 423 16APRIL ANN BIGAYNo ratings yet

- Joy Wills NotesDocument76 pagesJoy Wills NotesMichael Vincent BautistaNo ratings yet

- Difference Between License and EasementDocument14 pagesDifference Between License and EasementNakul Raj Jagarwal100% (1)

- DPWH Guide to Infrastructure Right-of-Way Acquisition and RelocationDocument125 pagesDPWH Guide to Infrastructure Right-of-Way Acquisition and RelocationERNIL L BAWA83% (6)

- Commercial Real Estate Interview PrepDocument8 pagesCommercial Real Estate Interview PrepciccioNo ratings yet

- Lagon vs. Lapuz Digest-RubyDocument1 pageLagon vs. Lapuz Digest-RubyDawn BarondaNo ratings yet

- Conditional Deed of Sale 1Document3 pagesConditional Deed of Sale 1John Paul Pagala AbatNo ratings yet

- Washtenaw County Parcel SummaryDocument47 pagesWashtenaw County Parcel SummaryHelpin HandNo ratings yet

- Landman Survival GuideDocument36 pagesLandman Survival GuideqqqasgaNo ratings yet

- IMPRESSIVE CONVEYANCING NOTES - by Onguto and KokiDocument89 pagesIMPRESSIVE CONVEYANCING NOTES - by Onguto and Kokikate80% (5)

- FHA Minimum Property StandardsDocument73 pagesFHA Minimum Property StandardsilroyNo ratings yet

- Rewpdf18 20110504Document29 pagesRewpdf18 20110504rscottcoNo ratings yet

- Property Law Notes Lecture Notes Lectures 1 10Document39 pagesProperty Law Notes Lecture Notes Lectures 1 10RjRajora100% (1)

- Dynamic Business Law The Essentials 4th Edition Kubasek Test BankDocument50 pagesDynamic Business Law The Essentials 4th Edition Kubasek Test Bankmichelleortizpxnzkycmbw100% (30)

- Is226 Tutorial 6 Problems For Week 7: Modeling Systems Requirements - Dfds SolutionsDocument7 pagesIs226 Tutorial 6 Problems For Week 7: Modeling Systems Requirements - Dfds Solutionsshaniya maharaj100% (1)

- Republic v. Vda de Castellvi Land Expropriation CaseDocument7 pagesRepublic v. Vda de Castellvi Land Expropriation CaseJonas PeridaNo ratings yet

- Macondray v. SellnerDocument10 pagesMacondray v. SellnerApa MendozaNo ratings yet

- GSAA Home Equity Trust 2005-15 - Purchased Property 3 Years After Closing Date From US BankDocument7 pagesGSAA Home Equity Trust 2005-15 - Purchased Property 3 Years After Closing Date From US BankTim BryantNo ratings yet

- Affidavit of Waiver Rights Real EstateDocument2 pagesAffidavit of Waiver Rights Real EstateRyu UyNo ratings yet

- Condominio Orion em Construção - Sommerschield 2Document15 pagesCondominio Orion em Construção - Sommerschield 2Wendy Cinthia Nobela InácioNo ratings yet

- 201744-2016-Bradford United Church of Christ Inc. V.Document7 pages201744-2016-Bradford United Church of Christ Inc. V.Vee Jay DeeNo ratings yet

- Iowa Admin. Code R. 193E-14.1 (543B) (6) : ARELLO Archive Iowa-Delivery of Property Condition DisclosureDocument3 pagesIowa Admin. Code R. 193E-14.1 (543B) (6) : ARELLO Archive Iowa-Delivery of Property Condition DisclosureNational Association of REALTORS®No ratings yet

- Property de Leon Notes PDFDocument3 pagesProperty de Leon Notes PDFClarisseOsteria50% (4)

- BSAD 295 Solution 2Document52 pagesBSAD 295 Solution 2Erin Liu100% (1)