You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Chapter 3 ParcorDocument6 pagesChapter 3 Parcornikki sy40% (5)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Teuer FurnitureDocument35 pagesTeuer FurniturePawanDubeyNo ratings yet

- Analyze Financial StatementsDocument111 pagesAnalyze Financial StatementsOther Side100% (3)

- Session 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsDocument55 pagesSession 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsRheneir Mora100% (1)

- Adjusting Entries: Matching Revenues and ExpensesDocument68 pagesAdjusting Entries: Matching Revenues and ExpensesLợi MD FCNo ratings yet

- Fun Golf SolicitationDocument2 pagesFun Golf SolicitationRheneir MoraNo ratings yet

- PAREB AMLC Online Registration System GuideDocument72 pagesPAREB AMLC Online Registration System GuideRheneir MoraNo ratings yet

- Peach.confirmation.QQ5775Document3 pagesPeach.confirmation.QQ5775Rheneir MoraNo ratings yet

- Peach.confirmation.EU88X5Document3 pagesPeach.confirmation.EU88X5Rheneir MoraNo ratings yet

- Talisay Central Eagles ClubDocument5 pagesTalisay Central Eagles ClubRheneir MoraNo ratings yet

- Certificate SphinxDocument1 pageCertificate SphinxRheneir MoraNo ratings yet

- Electronic Ticket Receipt 26MAR For RHENEIR PARAN MORADocument3 pagesElectronic Ticket Receipt 26MAR For RHENEIR PARAN MORARheneir MoraNo ratings yet

- Or Wiib511710389303Document1 pageOr Wiib511710389303Marjorie Unabia HernandoNo ratings yet

- Cebu Pacific Air MoraDocument4 pagesCebu Pacific Air MoraRheneir MoraNo ratings yet

- SourceTech Consultancy LLCDocument11 pagesSourceTech Consultancy LLCRheneir MoraNo ratings yet

- Annual Business BudgetDocument22 pagesAnnual Business BudgetGeisson Martinez GenaoNo ratings yet

- 2019notice New Forms and Pre EvaluationDocument29 pages2019notice New Forms and Pre EvaluationRheneir MoraNo ratings yet

- Differences PFRSDocument11 pagesDifferences PFRSRheneir MoraNo ratings yet

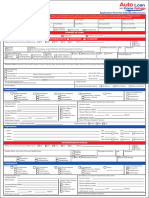

- New Auto-Loan-Application-Form - IndividualDocument2 pagesNew Auto-Loan-Application-Form - IndividualRheneir MoraNo ratings yet

- MS Call CardsDocument3 pagesMS Call CardsRheneir MoraNo ratings yet

- 1MSADocument1 page1MSARheneir MoraNo ratings yet

- Session 6 - QAR Audit Methodology Manual Presentation - Review and FinalizationDocument23 pagesSession 6 - QAR Audit Methodology Manual Presentation - Review and FinalizationRheneir MoraNo ratings yet

- GMM ProgramDocument1 pageGMM ProgramRheneir MoraNo ratings yet

- Session 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureDocument18 pagesSession 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureRheneir MoraNo ratings yet

- 77th ANC CebuDocument7 pages77th ANC CebuRheneir MoraNo ratings yet

- 49 Insights July 2022Document41 pages49 Insights July 2022Rheneir MoraNo ratings yet

- Amcham Phil. Membership SurveyDocument2 pagesAmcham Phil. Membership SurveyRheneir Mora100% (1)

- Session 3 - QAR Audit Methodology Manual Presentation - Intro To The ManualDocument12 pagesSession 3 - QAR Audit Methodology Manual Presentation - Intro To The ManualRheneir MoraNo ratings yet

- Session 2 - QAR Audit Methodology Manual - IsQMDocument49 pagesSession 2 - QAR Audit Methodology Manual - IsQMRheneir MoraNo ratings yet

- Session 1 - QAR Audit Methodology Manual Presentation - Fundamentals of PSA AuditDocument34 pagesSession 1 - QAR Audit Methodology Manual Presentation - Fundamentals of PSA AuditRheneir MoraNo ratings yet

- Accreditation of APO and AIPODocument24 pagesAccreditation of APO and AIPOteguhsunyotoNo ratings yet

- Updated Japan Visa RequirementsDocument2 pagesUpdated Japan Visa RequirementsRheneir MoraNo ratings yet

- 04 Property PicturesDocument1 page04 Property PicturesRheneir MoraNo ratings yet

- 03 - List of PropertiesDocument4 pages03 - List of PropertiesRheneir MoraNo ratings yet

- 67 1 1 Accountancy Compart PaperDocument23 pages67 1 1 Accountancy Compart PaperManuj AroraNo ratings yet

- BSA2A Financial ManagementDocument10 pagesBSA2A Financial ManagementFlorenz AmbasNo ratings yet

- Template 2 Task 3 Calculation Worksheet - BSBFIM601Document17 pagesTemplate 2 Task 3 Calculation Worksheet - BSBFIM601Writing Experts0% (1)

- Operating Statements and Balance Sheets for Cartwright Company 2001-2004Document7 pagesOperating Statements and Balance Sheets for Cartwright Company 2001-2004UMMUSNUR OZCANNo ratings yet

- Segment and Interim ReportingDocument8 pagesSegment and Interim ReportingKECEBONG ALBINO50% (2)

- Translation To The Presentation Currency/translation of A Foreign OperationDocument1 pageTranslation To The Presentation Currency/translation of A Foreign OperationdskrishnaNo ratings yet

- Ipsas ManualDocument180 pagesIpsas ManualJohanna Catahan100% (1)

- Cashflow (MK)Document2 pagesCashflow (MK)Karisma DeviNo ratings yet

- Scanner 2 PDFDocument137 pagesScanner 2 PDFyuvraj khatriNo ratings yet

- Consolidated Balance Sheet of H Ltd and S LtdDocument11 pagesConsolidated Balance Sheet of H Ltd and S LtdJesse SandersNo ratings yet

- Teodoro M. Luansing College of Rosario: Senior High School DepartmentDocument9 pagesTeodoro M. Luansing College of Rosario: Senior High School DepartmentSamantha Alice LysanderNo ratings yet

- Interloop Financials 2023Document31 pagesInterloop Financials 2023Ghulam MustafaNo ratings yet

- CPA Review School Philippines Financial Accounting PreboardDocument18 pagesCPA Review School Philippines Financial Accounting PreboardAllyson VillalobosNo ratings yet

- Perpetual - Financial StatementsDocument4 pagesPerpetual - Financial StatementsJeon Cyrone CuachonNo ratings yet

- Introduction to Financial Management ConceptsDocument14 pagesIntroduction to Financial Management ConceptsAiron BendañaNo ratings yet

- Introduction To Corporate Finance 4th Edition Booth Test Bank 1Document49 pagesIntroduction To Corporate Finance 4th Edition Booth Test Bank 1glen100% (47)

- Chapter 08 Entrepreneurship by Zubair A Khan - Copy (2) of Im - 08Document21 pagesChapter 08 Entrepreneurship by Zubair A Khan - Copy (2) of Im - 08Zubair A KhanNo ratings yet

- Alphabet 2014 Financial ReportDocument6 pagesAlphabet 2014 Financial ReportsharatjuturNo ratings yet

- Balance SheetDocument18 pagesBalance SheetAndriaNo ratings yet

- Workshop Lecture 4 QsDocument8 pagesWorkshop Lecture 4 QsabhirejanilNo ratings yet

- FAR1Document736 pagesFAR1Muhammad AwanNo ratings yet

- P 2Document4 pagesP 2Julious CaalimNo ratings yet

- Kunci Jawaban ElisaDocument52 pagesKunci Jawaban ElisaElisa EndrianiiNo ratings yet

- Tran Hoai Anh Bai Tap Chap 4Document16 pagesTran Hoai Anh Bai Tap Chap 4Vũ Nhi AnNo ratings yet

- Foundation Acc AssignmentDocument4 pagesFoundation Acc AssignmentJOEY LEONG KAH JIENo ratings yet

- FABM 1.module 4 PDFDocument21 pagesFABM 1.module 4 PDFSHIERY MAE FALCONITINNo ratings yet