You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Credit Card Processing GlossaryDocument14 pagesCredit Card Processing Glossarykintirgum100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Bill of Exchange DiscountingDocument14 pagesBill of Exchange Discountingrida_fatima1067% (3)

- Practice Question - Absorption & Variable Costing - May 2015Document8 pagesPractice Question - Absorption & Variable Costing - May 2015Muhammad Ali MeerNo ratings yet

- Rebate Processing PDFDocument42 pagesRebate Processing PDFrajesh1978.nair238186% (7)

- Competitor Analysis - Arla FoodsDocument94 pagesCompetitor Analysis - Arla FoodsRamsha Sheikh100% (1)

- Pampers - Integrated Marketing Communication PlanDocument40 pagesPampers - Integrated Marketing Communication PlanAli Usman100% (1)

- Consumer Attitude Towards Asian Paints EXECUTIVE SUMMARYDocument2 pagesConsumer Attitude Towards Asian Paints EXECUTIVE SUMMARYDARSHANFRANK0% (1)

- Chapter 4 Procurement Supply MGMTDocument79 pagesChapter 4 Procurement Supply MGMTisang100% (1)

- Delta Fuels Company ProfileDocument12 pagesDelta Fuels Company ProfileAnonymous 5z7ZOpNo ratings yet

- Cost and Management Accounting TechniquesDocument20 pagesCost and Management Accounting TechniquesAsem ShabanNo ratings yet

- Chapter 09Document47 pagesChapter 09موسى البلوي100% (13)

- MPCPressReleaseJuly2014 FINALAR PDFDocument2 pagesMPCPressReleaseJuly2014 FINALAR PDFAsem ShabanNo ratings yet

- Chapter 09Document47 pagesChapter 09موسى البلوي100% (13)

- Arens14e ch20 PPTDocument30 pagesArens14e ch20 PPTAsem ShabanNo ratings yet

- Varmora's Project ReportDocument93 pagesVarmora's Project ReportpRiNcE DuDhAtRa100% (1)

- KotlerDocument5 pagesKotlerVineeth GopalNo ratings yet

- E.digital v. Dexxon Groupe Holding Et. Al.Document7 pagesE.digital v. Dexxon Groupe Holding Et. Al.Patent LitigationNo ratings yet

- Marketing Strategy For NokiaDocument44 pagesMarketing Strategy For NokiaGurvinder SinghNo ratings yet

- Accounting Income Vs Economic Income DefinitionDocument11 pagesAccounting Income Vs Economic Income DefinitionZahid UsmanNo ratings yet

- Economics consumption concepts demand functions utility maximizationDocument2 pagesEconomics consumption concepts demand functions utility maximizationShahzad AhmadNo ratings yet

- 06 Supplier Approval Conversation Guide Outside The US Google DocsDocument6 pages06 Supplier Approval Conversation Guide Outside The US Google DocsPipit IkeNo ratings yet

- Communication Process With Reference To AdvertisingDocument11 pagesCommunication Process With Reference To Advertisingapi-291598576No ratings yet

- How persuaders manipulate our shopping and spendingDocument4 pagesHow persuaders manipulate our shopping and spendingJoshua JethrohNo ratings yet

- Alita (BD.) Limited: Industrial Tour Report OnDocument54 pagesAlita (BD.) Limited: Industrial Tour Report Onsalman KomorNo ratings yet

- Kellogg's Potential in Czech Cereal MarketDocument23 pagesKellogg's Potential in Czech Cereal MarketAmal HameedNo ratings yet

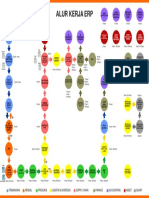

- Alur Kerja Erp: Pemasaran Rendal Produksi Logistik & Ekspedisi Supply Chain Finance Accounting Asset QuaryDocument1 pageAlur Kerja Erp: Pemasaran Rendal Produksi Logistik & Ekspedisi Supply Chain Finance Accounting Asset QuaryMuhammad FairusNo ratings yet

- Marketing Plan Development-2Document21 pagesMarketing Plan Development-2Yesica Yuliana Lopez CardenasNo ratings yet

- Internship Report On Marketing Activities of Expo GroupDocument14 pagesInternship Report On Marketing Activities of Expo GroupsaajancuNo ratings yet

- GE Energy Parts Inc VsDocument7 pagesGE Energy Parts Inc VsAnant ShrivastavaNo ratings yet

- Showpreview - Day1Document24 pagesShowpreview - Day1rudypatilNo ratings yet

- Rural Marketing The Changing ScenarioDocument9 pagesRural Marketing The Changing ScenariobitbknNo ratings yet

- Finals StratCostDocument7 pagesFinals StratCostMarie AzaresNo ratings yet

- Recalibrate To Win: Oc&C FMCG India Index Fy 08Document12 pagesRecalibrate To Win: Oc&C FMCG India Index Fy 08nareshsbcNo ratings yet

- Promotion StrategiesDocument2 pagesPromotion StrategiesAmirul NorisNo ratings yet

- Deed of Absolute Sale - WCGDocument3 pagesDeed of Absolute Sale - WCGMargeon Caminade100% (1)